Markets & Indices

-

Today's market sentiment is defined by diverging sector performance and growing caution ahead of the latest US jobs report (NFP). This data release is highly anticipated, as it will set the tone for the first Federal Reserve rate meeting under the new chair, Kevin Warsh.

-

The current macroeconomic environment complicates upcoming monetary policy decisions, driven by rising inflation, weakening consumer base and growing gap between the manufacturing and services sectors. Given these challenging headwinds, even an as-expected, positive NFP reading could drive the US dollar higher.

-

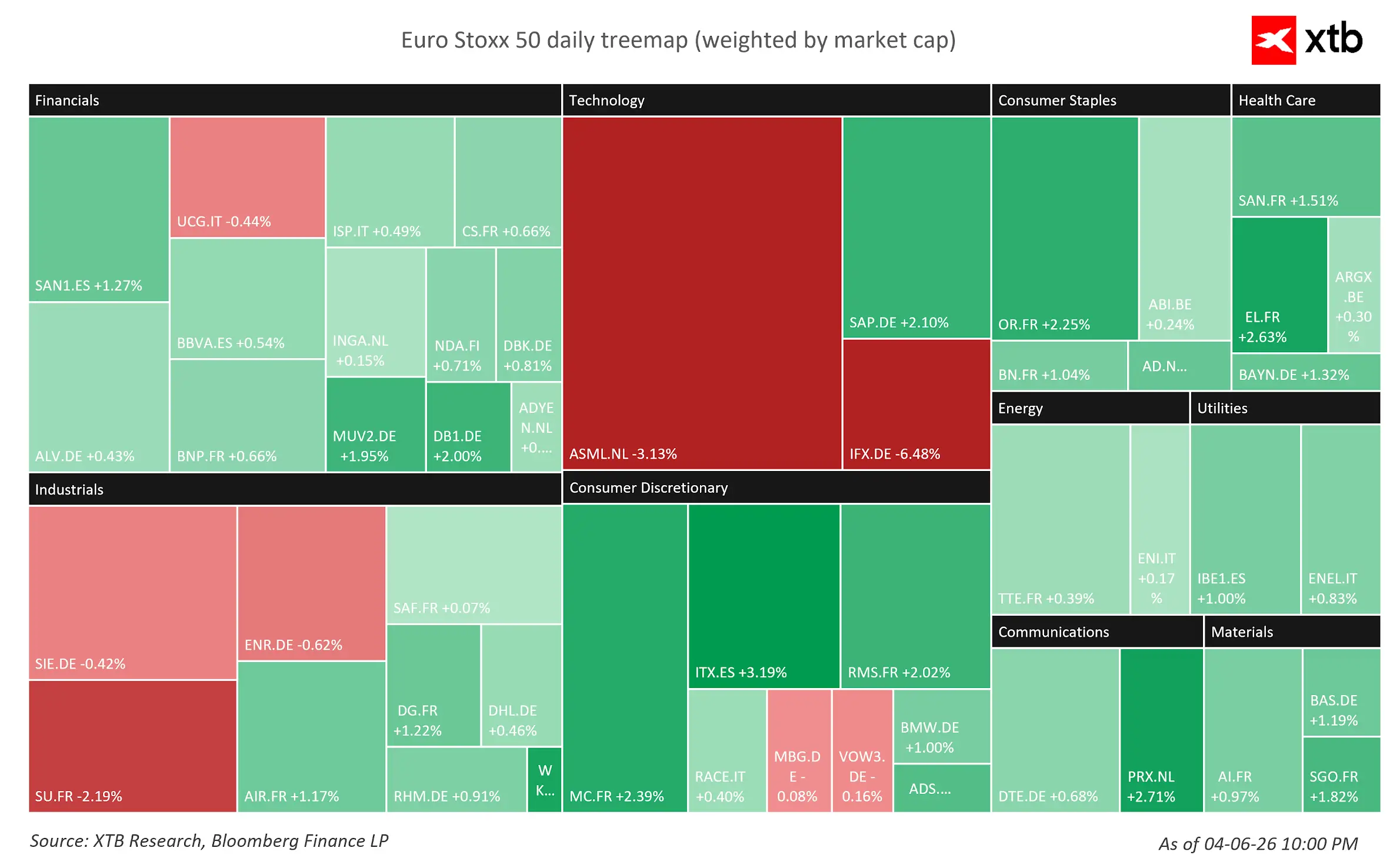

The sector rotation continues, with Tech taking a step back after the most recent rally (ASML: -3.1%) and leaving the room for other names that did not benefit from the last wave of AI optimism.

-

Futures for Spanish IBEX 35 (SPA35: +1%) lead gains today, thanks to the index’ heavy concentration of Financial (Banco Santander: +1.2%), Consumer Goods (Inditex: +3.5%) and even Energy stock (Repsol: +0.4%, Enagas: +1.3%), which are up despite a mild pressure in the crude oil futures.

-

French CAC40 (FRA40: +0.4%) futures follow the case with the strong representation of the Consumer Discretionary / Luxury sector (LVMH: +2.39%; Hermès: +2.02%).

-

German DAX (DE40: +0.3%) futures close the top three, with once again Consumer Goods stocks like Zalando (+5.4%) and Adidas (+2%) offsetting the sell-off in the star of the recent sessions, Infineon (-6.48%). Surprisingly, SAP sharply contrasts with a Tech sell-off, extending yesterday’s gains by another +2.10%.

-

S&P Global has refused to change its index entry requirements, effectively blocking SpaceX’s massive $75 billion IPO from a swift entry into the S&P 500. Despite targeting a $1.75 trillion valuation, SpaceX fails to meet S&P's strict profitability rules, having posted a $4.94 billion loss in 2025. While S&P maintains its standard by refusing exceptions based solely on market cap, competitors like Nasdaq and FTSE Russell have already relaxed their rules to accommodate such mega-cap listings.

-

FOREX: The US Dollar (USDIDX) dips before NFP, dropping about 0.35% from 1-month high, reached during Wednesday’s session. The British Pound is the strongest major currency today, advancing 0.4% against the dollar (GBPUSD) and the Japanese yen (GBPJPY). EURUSD is up 0.2% at 1.163.

-

COMMODITIES: oil futures recovered mild losses from earlier trading, currently trying to turn green (OIL: -0.05%, OIL.WTI: +0.3%). NATGAS extended yesterday’s losses by another 1.2%. Precious metals are also under pressure, with GOLD dropping 0.3% to 4460 USD/oz and SILVER losing 1.6% to 72.70 USD/oz.

-

CRYPTO: The liquidity is leaving the digital assets with the majority of major and minor tokens trading deep in the red. Bitcoin is down 1.1% to 62 600 USD, Ethereum losses 4.6% to 1680 USD. Solana (-1.7%), Dogecoin (-3.1%) and Chainlink (-4%) are also recording losses.

Today's performance of Stoxx 50 index members. Source: XTB Research using data from Bloomberg

Economics & Geopolitics

-

Despite a US-mediated truce, Israeli strikes in Lebanon killed four people, contrasting with President Trump’s claims of progress in talks with Hezbollah and Netanyahu. Meanwhile, mixed signals emerged regarding US-Iran negotiations; Trump suggested a potential deal and meeting with Iran’s supreme leader, while Iran denied significant progress. Additionally, tensions persist over the Strait of Hormuz, with Iran planning to charge shipping "service fees" for security, a move strongly opposed by the US demanding toll-free transit.

-

The media also reported on an alleged acceptance of Iran, passed to Pakistan, to transfer a part of its uranium to a third country agreed upon by both sides of the conflict.

-

Revised Eurostat figures indicate euro area GDP contracted by 0.2% compared to the prior quarter, while EU GDP fell by 0.1%. Concurrently, euro area employment slightly grew by 0.1%, whereas EU employment remained flat at 0.0%. These updated estimates utilise broader datasets than initial flash reports and incorporate Bulgaria's 2026 entry into the euro area.

-

Russian President Vladimir Putin firmly rejected European leaders as mediators in the Ukraine conflict, accusing them of lacking neutrality. Instead, he demanded adherence to a peace compromise allegedly arranged with Donald Trump in Alaska. Meanwhile, Ukrainian President Zelenskyy proposed direct negotiations, while Putin threatened further hypersonic missile strikes against Ukraine.

The SPA35 daily chart exhibits a strong bullish structure. The price trades at 18479, well above its 10, 30, and 100-period EMAs, indicating solid upward momentum. Having cleared the 100.0% Fibonacci level at 18391, bulls are testing the multi-month resistance near 18569. The rising RSI confirms buying pressure while leaving room before overbought territory. Source: xStation5

Economic Calendar: Could Smaller Job Reports Pressure Fed to Hike?

Morning Wrap: Equities under pressure after Wall Street took profits, FX frozen (06.08.2026)

Daily Summary: Dow Jones hits record highs, while gold and silver rally on hopes for a US–Iran deal

Hormuz Deal Moves Closer

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.