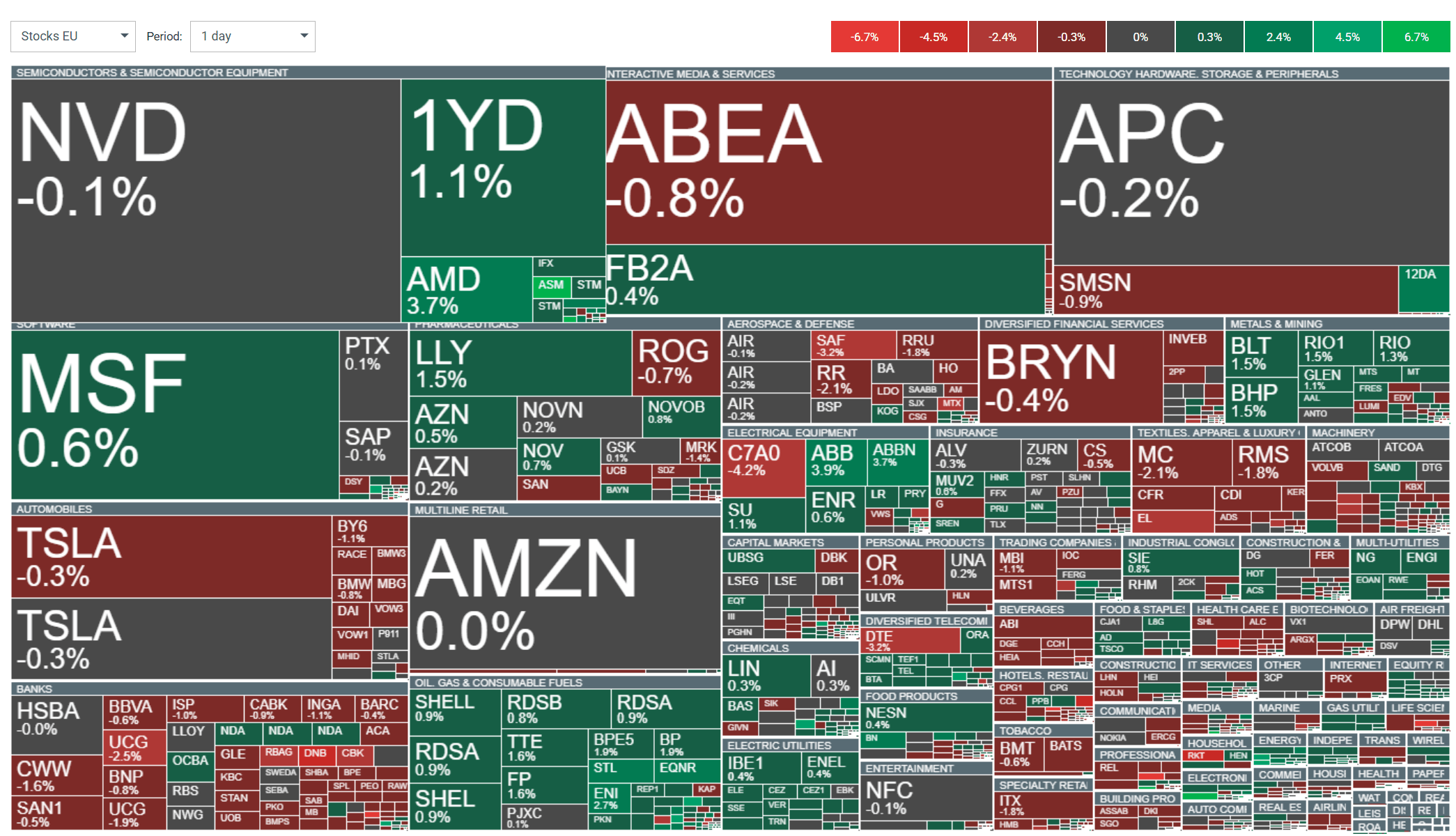

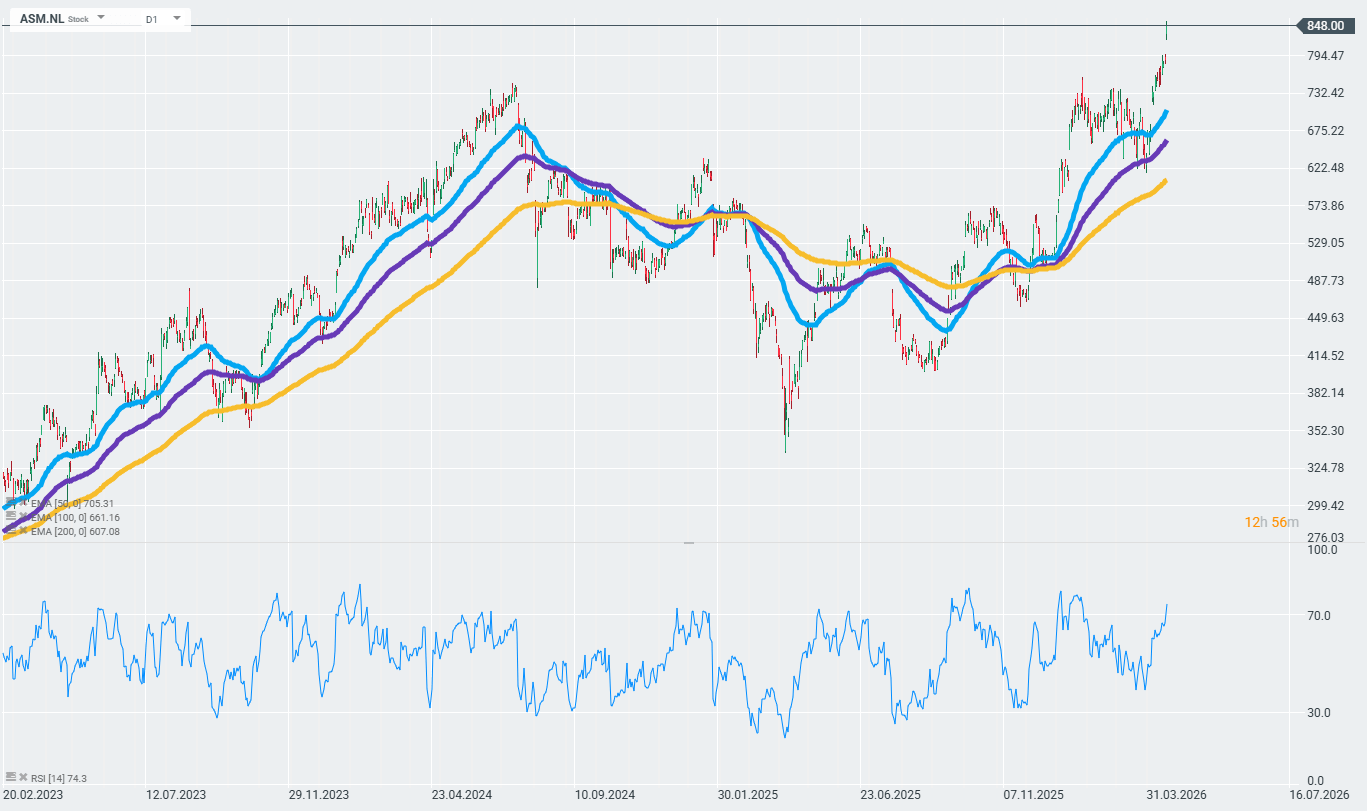

Last night, Dutch semiconductor equipment giant ASM International released its Q1 2026 results, which beat expectations and set new margin records. This morning, the company’s shares are jumping by +8.4% to all-time highs, pulling the entire European tech sector along with them and propelling ASMI to the top of the pan-European index.

The technology sector is driving today's gains in Europe. Source: xStation

Citi commented: “ASM significantly exceeded expectations and raised its forecasts, even by semiconductor industry standards.”

📊 Key figures — bet & raise:

-

Q1 2026 revenue: €862.5 million vs. consensus of €828.5 million (LSEG) — at the upper end of the company’s guidance of €830 million ±4%

-

Year-over-year revenue growth: +3% reported / +16% at constant exchange rates

-

Gross margin: 53.3% — supported by a favorable product mix (a year ago: 53.4%)

-

Adjusted operating margin: 33.1% — a quarterly record (a year ago: 32.3%)

-

Adjusted net profit: €246 million — an increase of €54 million year-over-year

🔭 Q2 2026 Guidance — another beat:

-

Q2 2026 revenue forecast: ~€980 million ±5% in constant currency

-

The analyst consensus (LSEG) was €883.9 million — the company is well above that figure

-

H2 2026 is expected to be stronger than H1 — management maintains its optimistic outlook for the full year

🀏 What is driving this growth?

The three main drivers evident in the results:

-

Logic/Foundry demand — strong performance on leading-edge nodes + a clear rebound in China (the company reported that China revenue is projected to grow year-over-year)

-

AI-led investment — customers are accelerating investments in production capacity for AI infrastructure; production of pilot lines for the 1.4 nm node is set to begin in H2 2026

-

Favorable product mix & cost control — record operating margin while increasing R&D spending

CEO Hichem M'Saad: “Customers are increasing their spending on state-of-the-art technological processes and investing in pilot production lines for the 1.4-nm process—these could be used in products from Nvidia and Apple.”

📈 Market and Valuation:

-

Shares up +63.8% YTD (including today's session) — top performer on the STOXX 600

-

The company has stopped publishing data on new orders (bookings) — analysts such as Degroof Petercam are taking it in stride: "With a beat in guidance like this, we couldn't care less."

-

Forward P/E ratio ~38x — a premium relative to the sector justified by record margins and exposure to AI

Source: xstation

Market wrap (05.08.2026)

AMD Did Everything Right… But Only Right

SpaceX Shares Drop 6% After Earnings 🚩 Is Space No Longer Enough for Wall Street?

Daily Summary: Nasdaq 100 Up 3.2% – Is the Bull Market Back? (04.08.2026)