12:30 GMT, United States - inflation data for February:

-

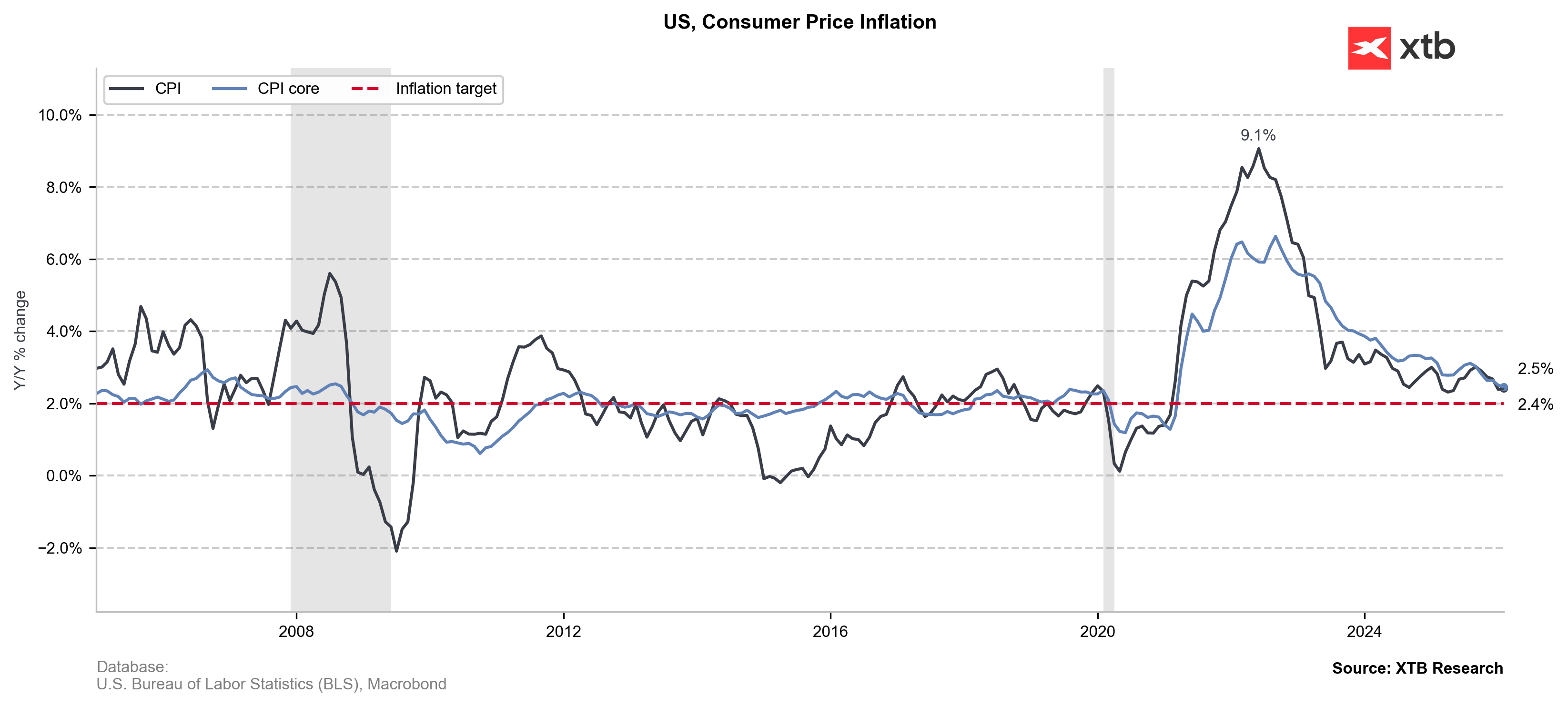

CPI YoY Actual 2.4% (Forecast 2.4%, Previous 2.4%)

-

CPI MoM Actual 0.3% (Forecast 0.3%, Previous 0.2%)

-

Core CPI YoY Actual 2.5% (Forecast 2.5%, Previous 2.5%)

-

Core CPI MoM Actual 0.2% (Forecast 0.2%, Previous 0.3%)

Despite a soft January print providing a favorable base for February, U.S. consumer prices remained subdued. However, the data is currently skewed downward by the government shutdown and does not yet reflect the recent surge in oil prices now hitting consumers' wallets.

Source: XTB Research

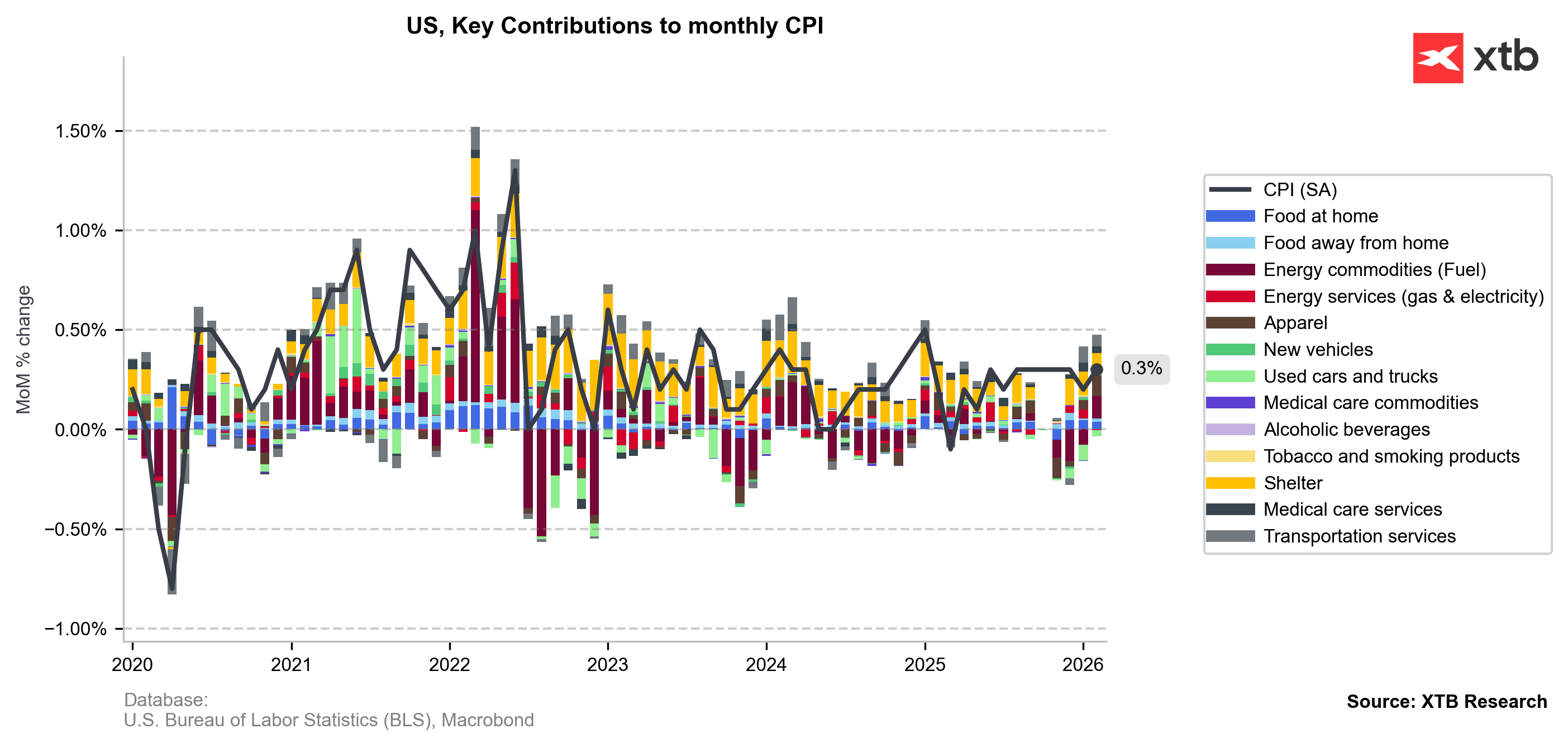

The composition of the CPI remains largely stable, with Core Services—specifically Shelter and Airfares—acting as the primary drivers of inflation, albeit the overall slowdown in Core CPI dynamics (from 0,3% to 0,2% m/m) should relieve Fed during the next FOMC. In terms of short-term monthly dynamics:

-

Used Cars continue to offer the most significant disinflationary relief.

-

Apparel and Energy Commodities saw a sharp acceleration in price pressure, largely due to the low base effect.

-

Software prices jumped 6.5%, notably defying the "SaaS-apocalypse" narrative that dominated February.

Source: XTB Research

EURUSD (M30)

Initially, the most traded currency pair had a muted reaction to the newest CPI print, suggesting no clear direction for the US monetary policy in the face of future data uncertainty. Thrity minutes in, EURUSD resumed losses, diving below key 1,1600 level, trying to find support at 1,1580.

Source: xStation5

Daily summary: Dollar rout after NFP, Gold back on the rise

Three markets to watch next week (07.08.2026)

The dollar sinks after labor market data💲📉

US OPEN: Shallow rebound in the shadow of a weak labor market