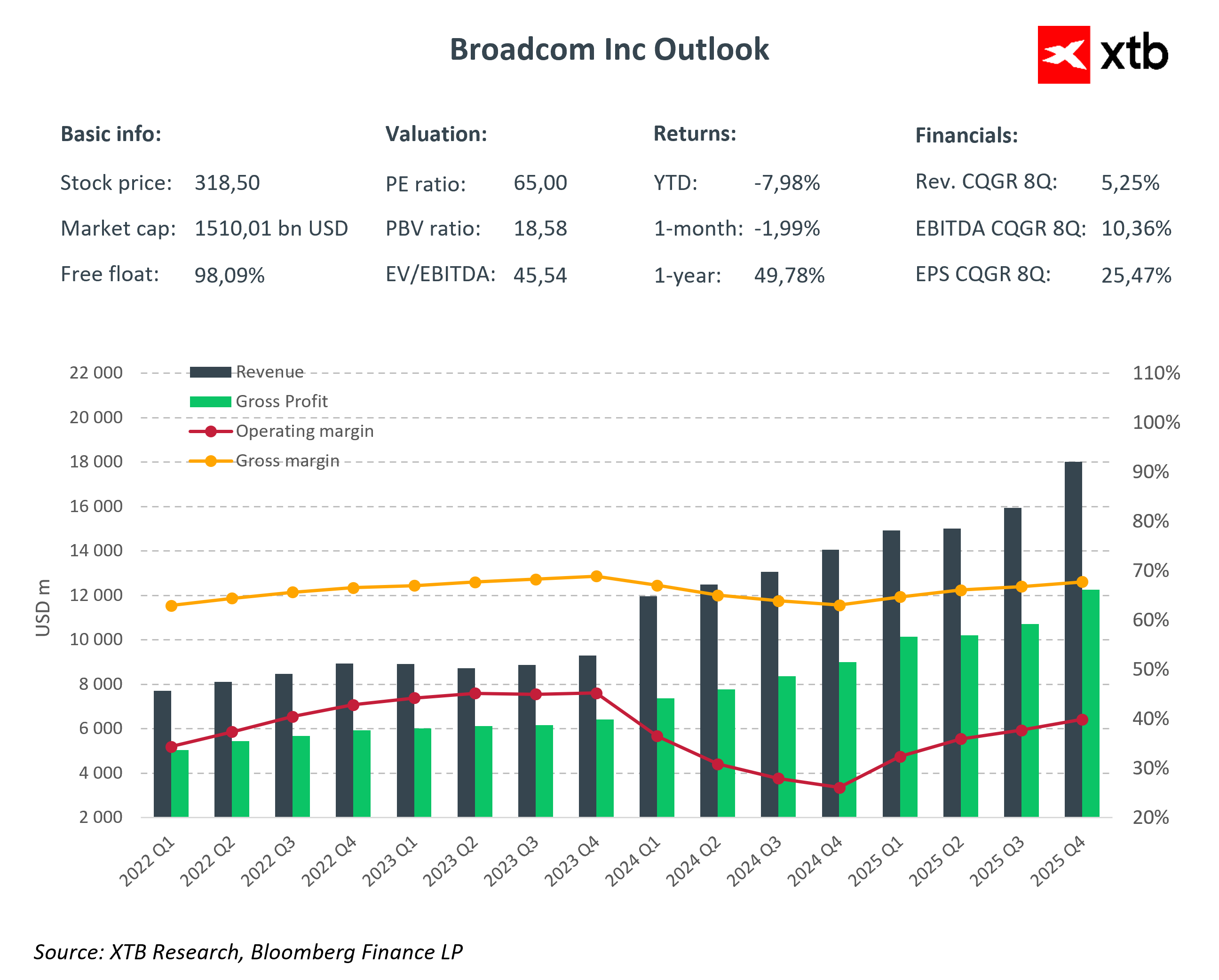

Broadcom Inc. enters the quarterly earnings season as one of the most important semiconductor companies shaping the development of infrastructure for artificial intelligence and cloud solutions. The company will release its results after the market closes tomorrow, and market expectations are high. Observers are looking not only at revenue growth but, more importantly, at the structure of that growth and Broadcom’s ability to maintain strong margins in advanced ASICs and infrastructure software. Following recent quarters with record AI and networking chip sales, markets anticipate another strong quarter, while simultaneously assessing risks related to cost pressures, product mix, and potential fluctuations in data center demand. Q1 FY2026 results will test whether Broadcom can convert growing AI demand into sustainable revenue growth and maintain its competitive position in the semiconductor industry.

Q1 FY2026 Financial Outlook

Markets expect Broadcom to deliver solid results in Q1 FY2026, with the following key projections:

-

Total revenue is expected to reach approximately 19.2–19.3 billion USD, representing year-on-year growth of around 28 percent.

-

Earnings per share (EPS) are projected at 2.02–2.03 USD, an increase of about 26 percent compared to the same period last year.

-

Revenue from AI and ASICs is expected to reach approximately 8.2 billion USD, representing more than 100 percent year-on-year growth, making it the primary driver of growth.

-

The infrastructure software segment is expected to show moderate year-on-year growth.

-

Other semiconductor and networking products are expected to grow steadily, though at a slower pace than AI.

Markets will pay particular attention to the revenue structure, as the share of AI and ASIC revenue relative to other segments will be a key indicator of the sustainability of growth. It is also important to assess whether a higher proportion of lower-margin products could weigh on overall profitability, especially in the context of rising production costs and capital expenditures.

AI and ASIC as the Main Growth Driver

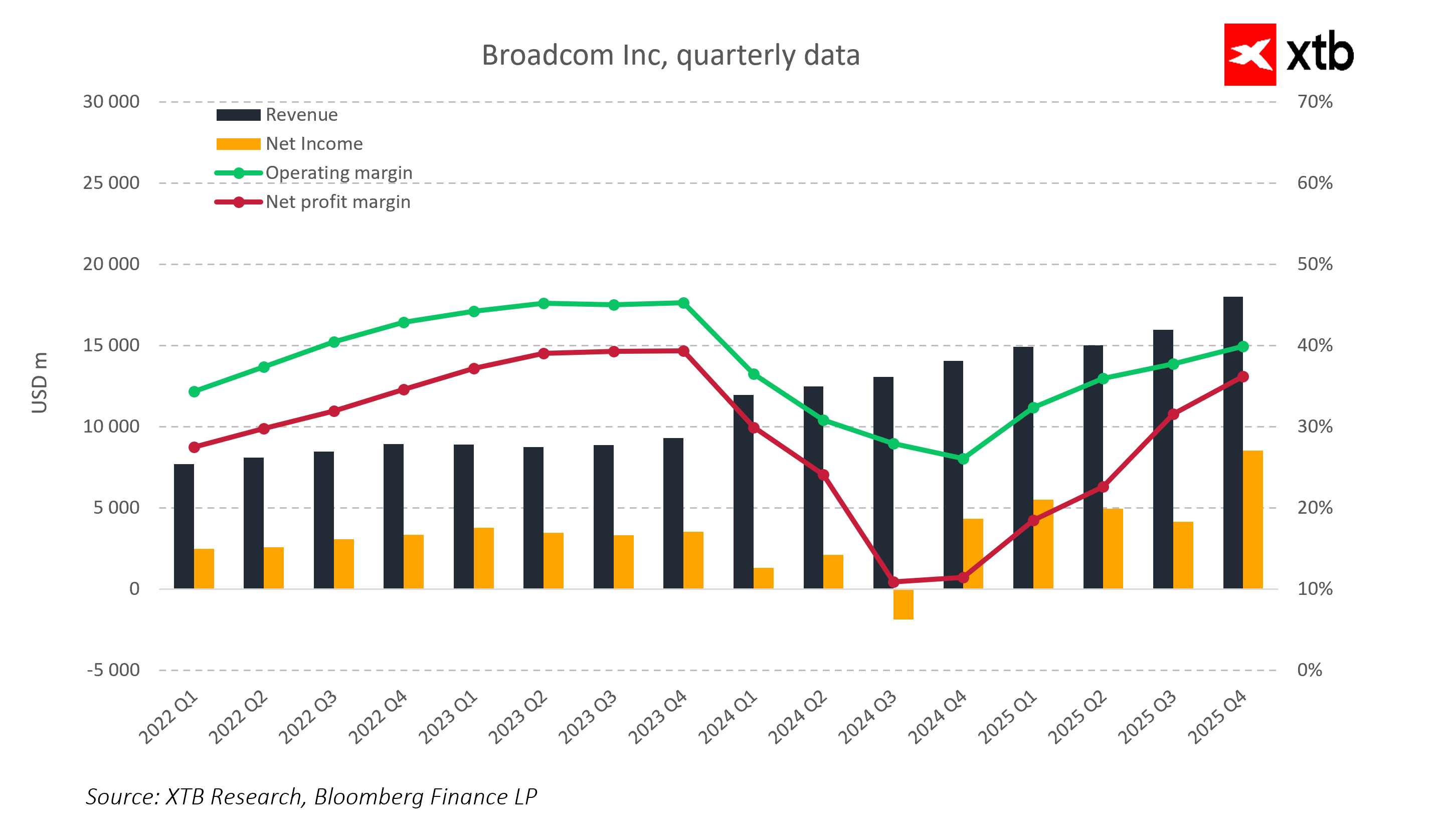

Revenue from ASICs and AI solutions is currently the key growth driver for Broadcom. Demand from hyperscalers and large technology partners remains high, resulting in dynamic growth in the AI segment. Broadcom provides both specialized chips that accelerate AI computations and networking infrastructure that supports data centers, making the company a strategic supplier of AI solutions. The integration of these products into customer data centers allows Broadcom to generate stable revenue and increase its market share in machine learning and large-scale data processing solutions. Markets will closely monitor the pace of AI revenue growth and its impact on overall profitability, as this segment becomes a critical growth lever beyond Broadcom’s traditional semiconductor products and infrastructure software.

Margins and Cost Pressure in Q1 FY2026

Despite strong revenue growth, markets will pay close attention to Broadcom’s margin levels in the upcoming quarter. A higher share of lower-margin products, including certain networking chips and parts of infrastructure software, could compress gross and operating margins compared to previous quarters. Markets will focus on management commentary regarding the sales mix, cost management, and allocation of capital expenditures in the AI and ASIC segments. Effectively balancing investment in new chip development while maintaining strong profitability will be a key indicator of the quality of Broadcom’s strategy and a signal to markets about whether the company can scale AI products profitably amid rising demand and production costs.

Market Sentiment and Short-Term Risks

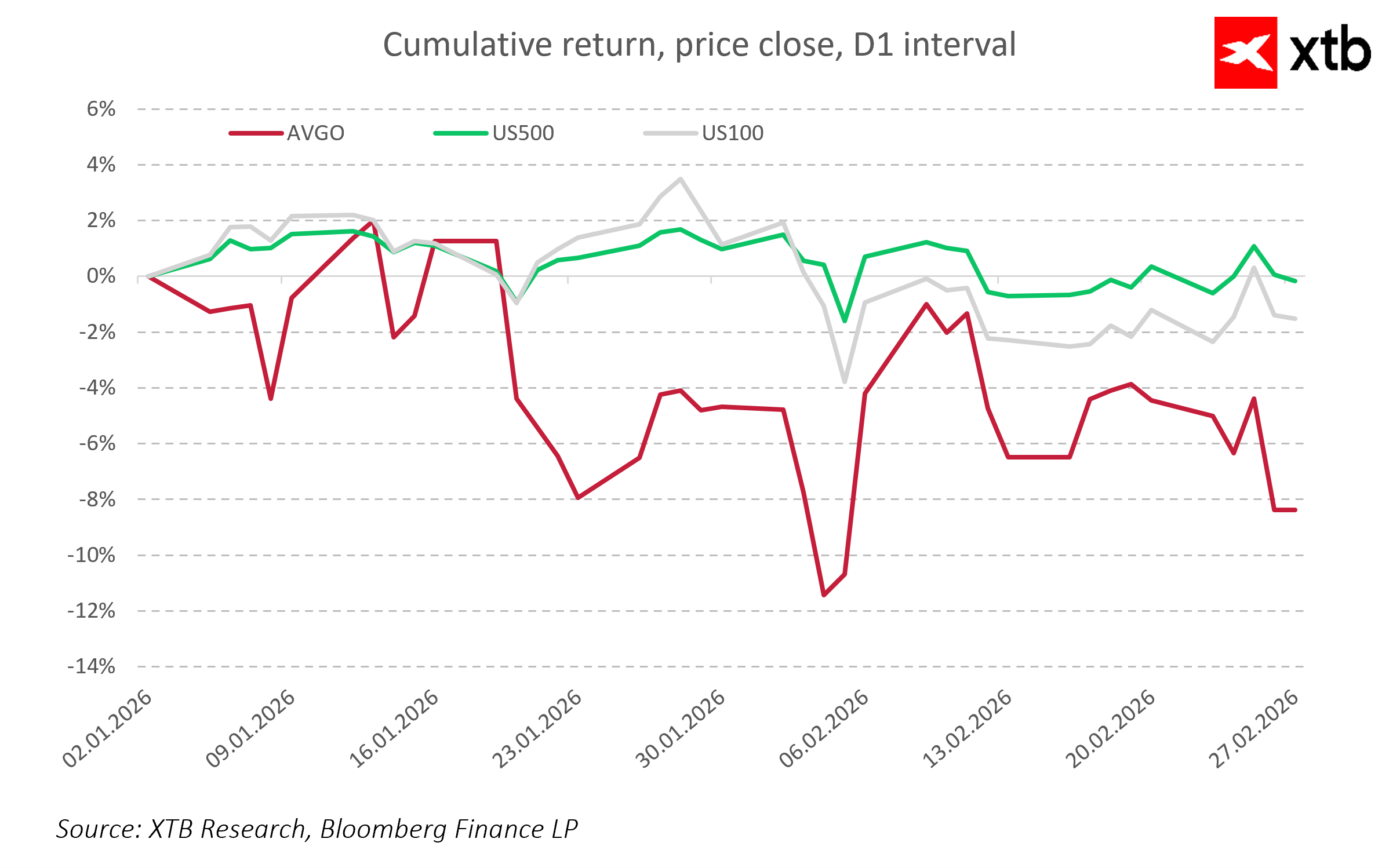

Markets are approaching Broadcom’s results with a mixed sentiment. Despite solid growth forecasts, the company may be vulnerable to short-term volatility caused by capital rotation away from the semiconductor sector following results from stronger competitors such as NVIDIA Corporation. High expectations for AI revenue and repeated quarters of beating estimates mean that even minor disappointments could trigger a nervous market reaction. Another risk factor is the potential normalization of demand following an intense investment cycle in data centers. Markets will also monitor analyst commentary and potential adjustments to price targets, which could affect the stock’s short-term valuation independently of fundamentals and long-term growth potential.

Key Takeaways and Metrics for Markets

Markets will primarily focus on revenue and earnings per share, looking to see if Broadcom achieves projected revenue of around 19.2–19.3 billion USD and EPS of 2.02–2.03 USD.

- The revenue structure will also be crucial. Observers want to see the share of revenue coming from AI and ASIC products, as this indicates whether growth is sustainable and whether Broadcom is effectively developing its future-oriented business segment.

- Margins will be another key focus. It is important to determine whether a higher proportion of lower-margin products, such as some networking chips and infrastructure software, could reduce overall profitability.

- Investments will remain under scrutiny. Management commentary on capital expenditures for data centers and AI infrastructure will show whether Broadcom can grow its business profitably and at scale.

- Finally, markets will monitor overall sentiment. Capital rotation within the semiconductor sector, possible normalization of demand, and expectations for upcoming quarters could influence market reactions independently of financial results.

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Morning Wrap: AI Fuels the Rebound. Technology Makes a Strong Comeback

Apple is still impressive, but the market is no longer impressed

Amazon’s massive AI bet is starting to pay off