Due to Juneteenth, commemorating the abolition of slavery in the United States, there is no trading session on the US stock market today. Futures contracts indicate minor declines for key indices, with both the S&P 500 and Nasdaq 100 edging down by 0.1%.

Geopolitics

Global stock markets were initially weighed down by reports of the postponement of the next round of peace talks between the US and Iran, which were scheduled to take place today in Switzerland. Sentiment improved slightly following news of a ceasefire between Israel and Hezbollah. Previous shelling by Israel had cast doubt on the durability of the memorandum signed on Wednesday between the US and Iran. It is worth recalling that this memorandum grants both parties 60 days to formulate a precise peace agreement. In the interim, however, the Strait of Hormuz is expected to be opened.

Commodities

Prices for key energy commodities remain volatile.

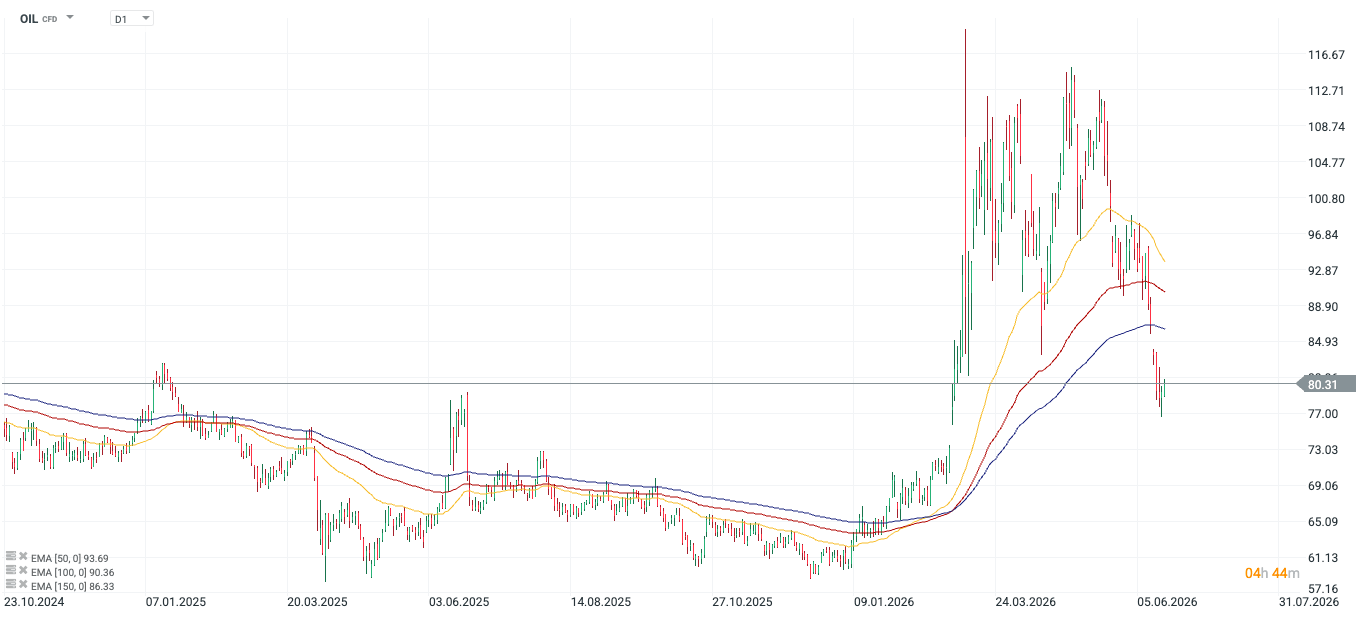

Taking crude oil as an example:

- Initially, we observed rising prices today, a reaction to the delay of the next round of peace talks.

- Subsequently, a correction followed, which can be partially attributed to the ceasefire between Israel and Hezbollah.

- Ultimately, however, Brent ends the day with a 1% gain, closing near $81 per barrel. We will pay just under $78 for WTI.

Figure 1: OIL [D1] (23.10.2024 - 19.06.2026)

Source: xStation, 19.06.2026

Source: xStation, 19.06.2026

Natural gas:

- NATGAS finishes the week at $3.2.

- TTF hovers around $42.1.

Precious metals continue to decline:

- We will currently pay approximately $4,156 per troy ounce of gold, and $64.9 for silver.

- The >1% move downward is largely a consequence of the continued rise in government bond yields in the largest economies, which serve as a direct alternative to precious metals as a low-risk asset.

Stock Market

With the exception of the Italian FTSE MIB (+0.3%) and the Polish WIG20 (+0.2%), European markets closed in the red today. The pan-European Stoxx 50 (-0.1%), German DAX (-0.2%), and British FTSE 100 (-0.4%) all posted losses.

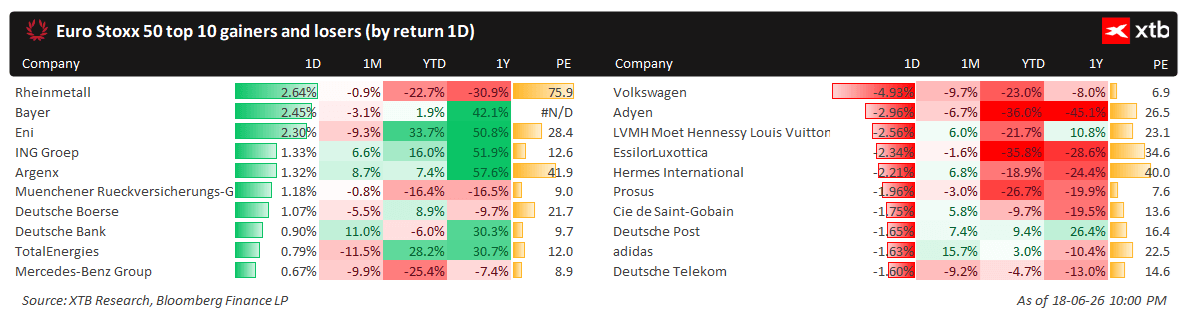

The largest decline, however, was recorded by the French CAC 40 (-0.6%), despite a substantial gain by Renault (+3.9%), which can be attributed primarily to the acquisition of a 65% stake in the company Flexis, which specialises in "last-mile logistics".

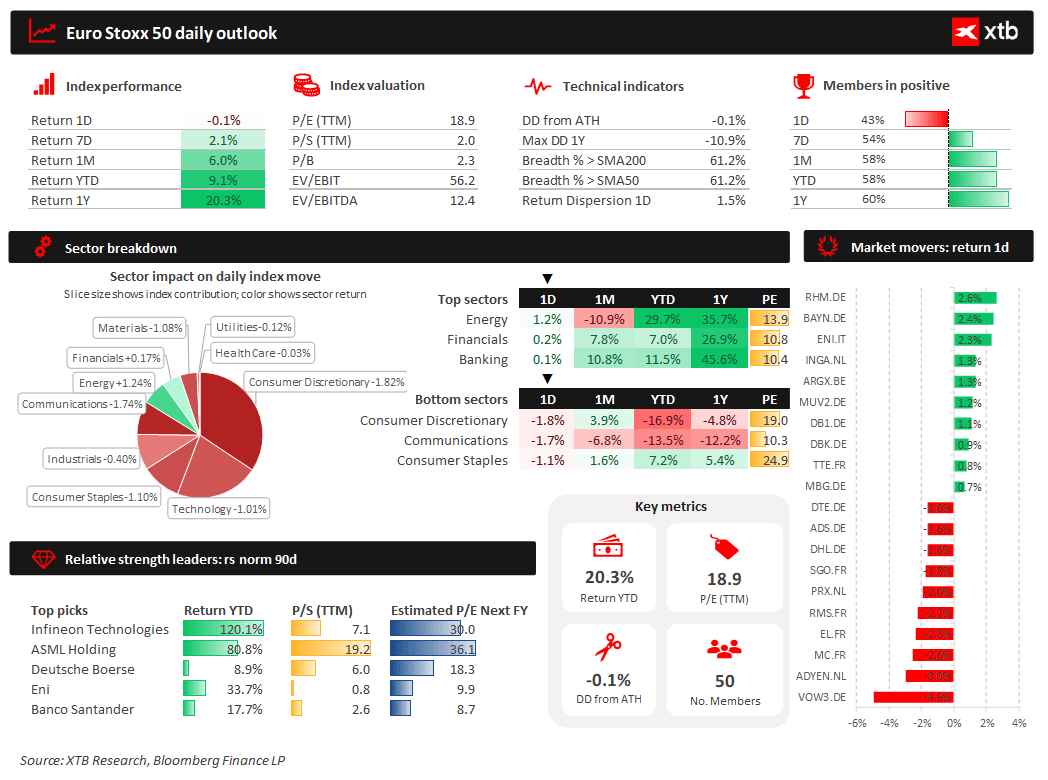

Figure 2: Dashboard for Euro Stoxx 50 (19.06.2026)

Source: XTB Research, 19.06.2026

Source: XTB Research, 19.06.2026

Figure 3: Winners and Losers on Euro Stoxx 50 (19.06.2026)

Source: XTB Research, 19.06.2026

Source: XTB Research, 19.06.2026

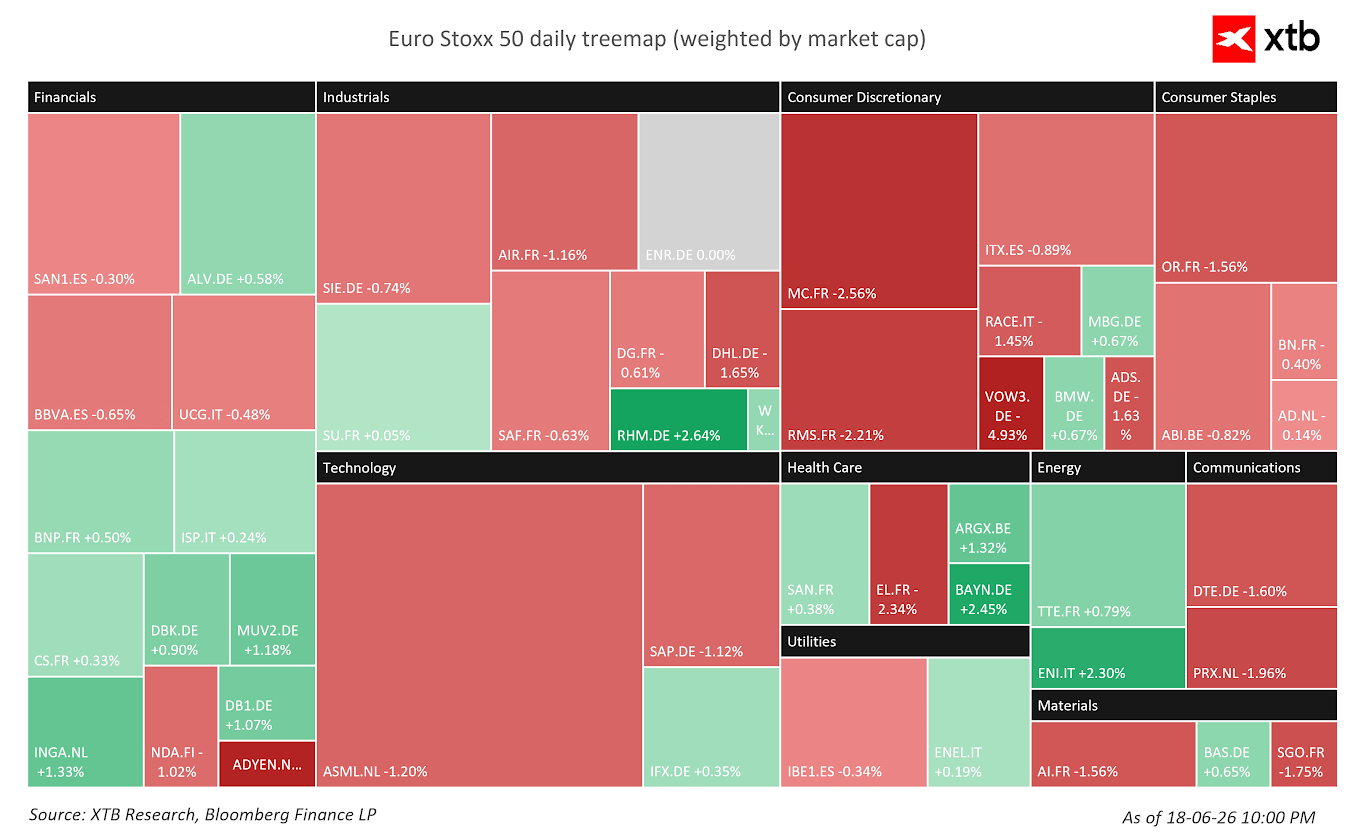

Figure 4: Heatmap for Euro Stoxx 50 (19.06.2026)

Source: XTB Research, 19.06.2026

Source: XTB Research, 19.06.2026

Macroeconomic Data + Currencies

We began the day with the Japanese CPI inflation reading.

- It held no surprises – the headline figure was 1.5%, with core inflation at 1.4%.

- Valuations for interest rate hikes remained largely unchanged – the market assigns approximately a 95% probability to such a move before the end of the year.

- The USD/JPY pair ends the day almost unchanged, hovering around 161.3.

- On a weekly basis, the yen’s depreciation against the dollar reaches 0.7%, which is relatively modest compared to other G10 currencies.

Later, it was time for data from the United Kingdom.

- Retail sales grew significantly stronger than the market anticipated (by 1.2% monthly, 3.2% year-on-year).

- This allowed for a modest appreciation of the pound (+0.2%).

- However, the British currency has not enjoyed a successful few days. Relative to the Monday open, GBPUSD has fallen by 1.3%.

—

Michał Jóźwiak, Financial Markets Analyst at XTB

Daily Summary: Equities rally on not-so-hawkish Fed and AI trade revival, Yen dominates FX, oil retreats (30.07.2026)

Unexpected FX intervention? USDJPY plummets more than 2%! 🇯🇵

Nasdaq futures rally more than 3% 🚀

US OPEN: Nasdaq rebounds! Microsoft and Lam Research earnings revive AI trade!