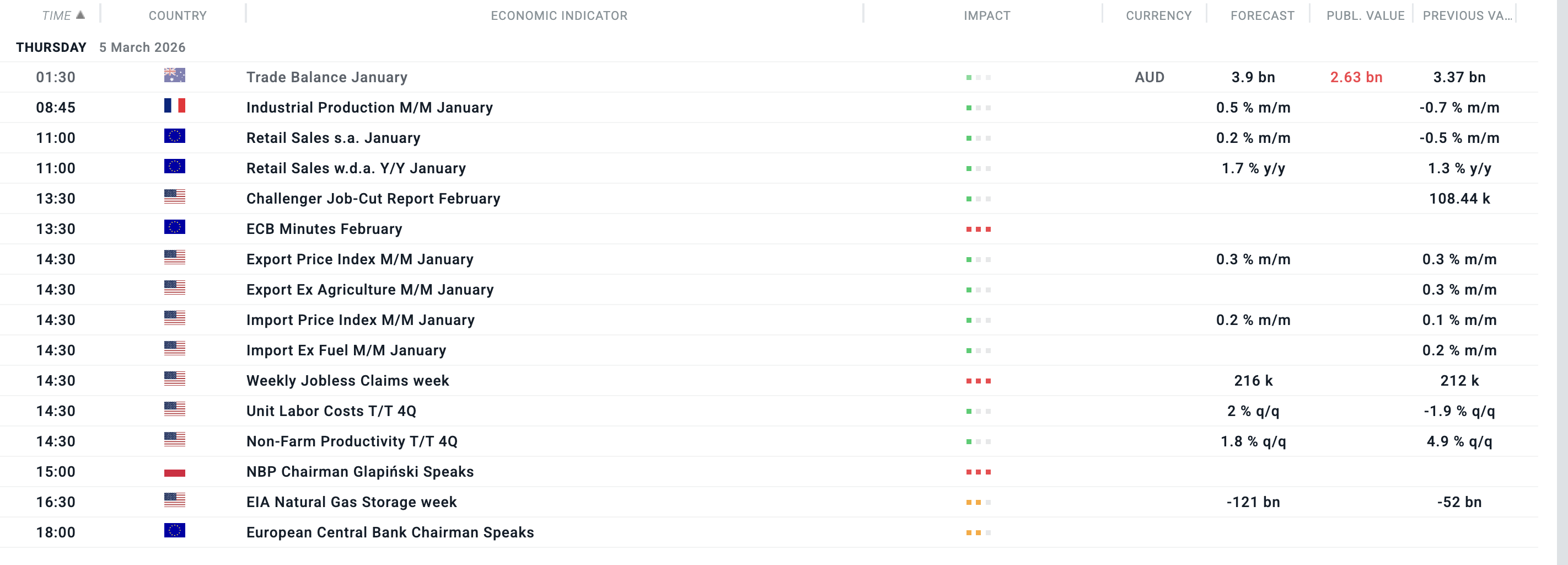

Even if all eyes remain turned toward the Middle East, Thursday will bring several publications that may break through the market noise due to the pressing issue of central banks and the new risk of energy price inflation.

In Europe, minutes from the last ECB meeting will be published, where the greatest attention will be drawn to the discussion on the euro exchange rate. The balance of risks from before the war in the Middle East de facto no longer exists, so the Governing Council's attitude toward a potentially too-strong euro—which, admittedly, has already returned from near 1.20 to 1.16—may turn out to be the only real hint for the future. Before the minutes, we also expect the retail sales reading for the Eurozone, while ECB President Christine Lagarde will speak in the evening.

For the Polish zloty, the most important role will be played by the conference of the NBP Governor, Prof. Adam Glapiński. The Monetary Policy Council lowered interest rates yesterday as expected by 25 bps to 3.75%, despite the geopolitical shock and concerns about a global return of inflationary pressure.

Across the Atlantic, the most important from the Fed's policy perspective will be jobless claims, and data regarding gas inventories may attract additional attention due to the conflict in the Middle East.

Financial results will be published by, among others: Costco, JD.com.

Filtered by: UK, US, Poland, France, Germany, Eurozone, Japan, Australia, New Zealand. Source: xStation5

When will the rise in oil prices reach us?

Daily Summary: Equities Diverge as Tech Lags, Europe Rallies on Earnings & PMIs (24.07.2026)

Three markets to watch next week (24.07.2026)

Oil Slides Ahead of the Weekend!