The GDPNow model last quarter went to great lengths to suggest the possibility of entering a technical recession. This has become a reality, although no one is talking about a "real" recession at this point. Now, the model indicates that we may be able to emerge from a technical recession as early as this quarter.

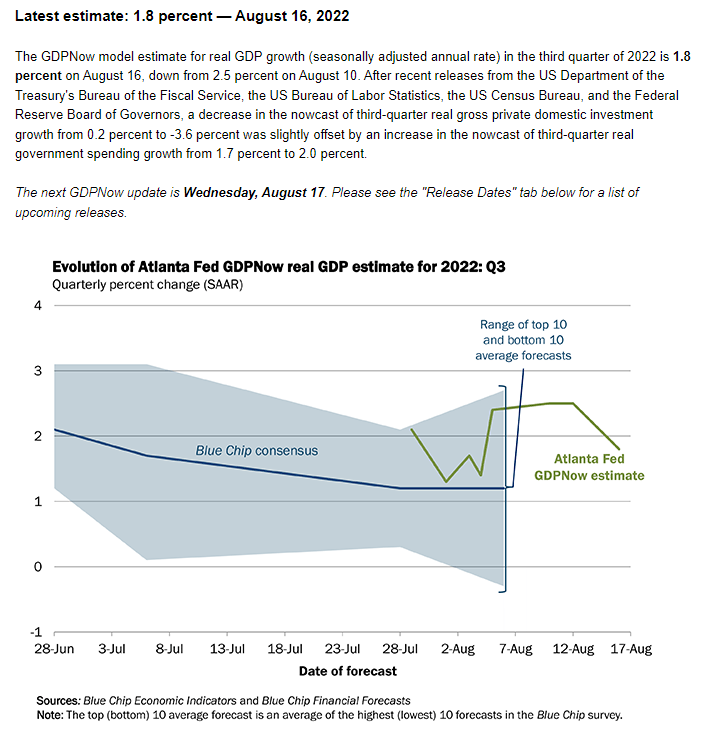

The model indicates real growth at 1.8%, which is, however, down from the previous 2.5%. This is due to a significant drop in the impact of private investment. On the other hand, there was an assessment of a higher impact of government spending.

It is worth mentioning that Q3 is a potential new wave of coronavirus, so growth in this period can be assessed very positively. On the other hand, there were very negative assessments as to Q3 in China.

Source: Fed Atlanta

Economic calendar - Europe's Inflation and US Housing Market in Spotlight

Economic Calendar: Earnings, US Retail Sales and Fed to Fight for Investors' Attention (16.07.2026)

BREAKING: GBPUSD up 0.1% after better-than-expected UK GDP data 🇬🇧 📈

Daily Summary: Wall Street Gains, Dow Jones Near All-Time Highs After Softer PPI Data