-

Crude oil remains stable ahead of the upcoming US–China summit. Brent oil is holding at a high level of around $107 per barrel after strong gains during the first two sessions of this week.

-

US equity index futures are recovering losses following the release of higher US inflation data. The US500 is currently up 0.3%, while the US100 is gaining as much as 0.8%. After yesterday’s declines, media narratives around so-called “buying the dip” have re-emerged. A similar rebound was also observed on the South Korean market.

-

Nvidia is rising by up to 2.5% in pre-market trading, supported by reports that Jensen Huang may accompany Donald Trump on his visit to China, potentially opening the door to new chip-related deals.

-

Global attention remains firmly focused on Beijing. As a reminder, a two-day visit by US President Donald Trump to China begins tomorrow. Key topics are expected to include Iran and the Persian Gulf, although observers do not anticipate any major breakthroughs.

-

France: Today’s April data showed mixed signals. CPI inflation came in at 2.2% y/y and HICP at 2.5%, both in line with expectations. However, the unemployment rate rose to 8.1%, indicating some weakening in the labour market.

-

Eurozone: The latest data confirm a slowdown in economic activity. Q1 GDP stood at 0.8% y/y, while industrial production fell by 2.1%, coming in well below expectations and highlighting continued weakness in the manufacturing sector.

-

GBPUSD is down nearly 0.2%, testing the 1.35 area amid political uncertainty in the United Kingdom.

-

Gold remains stable above $4,700, silver continues its upward trend, while copper has broken above $14,000.

Equities and corporate news:

Deutsche Telekom (DTE.DE) delivered a strong start to the year, reporting a 6.5% increase in adjusted net profit and stable cash flows. The results were strong enough for management to raise its full-year 2026 guidance for operating profit and free cash flow.

Allianz (ALV.DE) generated €53 billion in revenue, while PIMCO and AllianzGI attracted €21 billion in new capital inflows.

Siemens (SIE.DE) reported a mixed set of results: revenue and net income slightly disappointed, but new orders came in strongly at €24.1 billion, significantly beating expectations. Despite some pressure on industrial margins, the company maintained its growth outlook and announced a large share buyback programme of up to €6 billion.

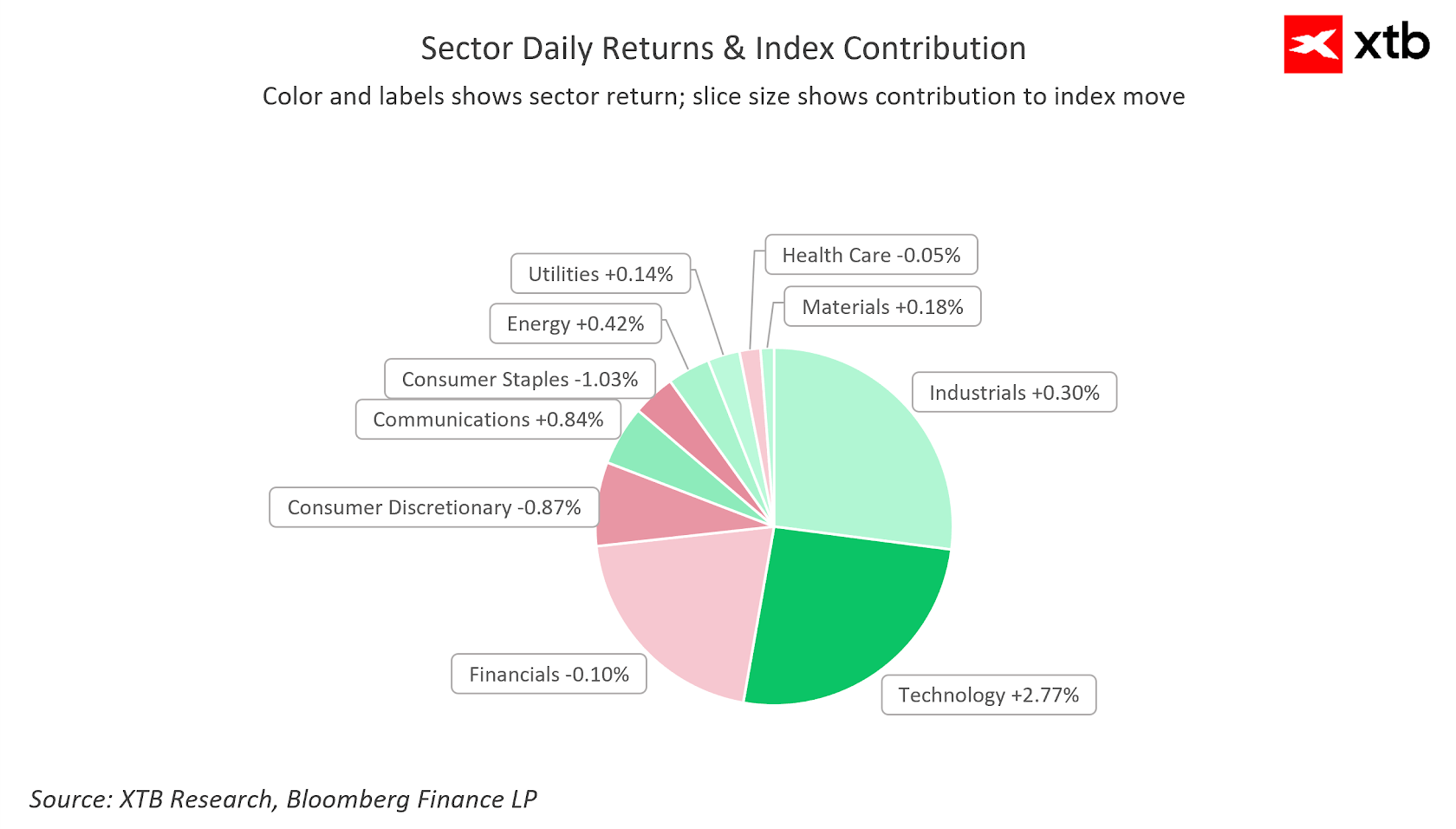

Volatility is visible today across major sectors of the economy. Notably, there is a renewed strong rebound in the technology sector. Source: XTB

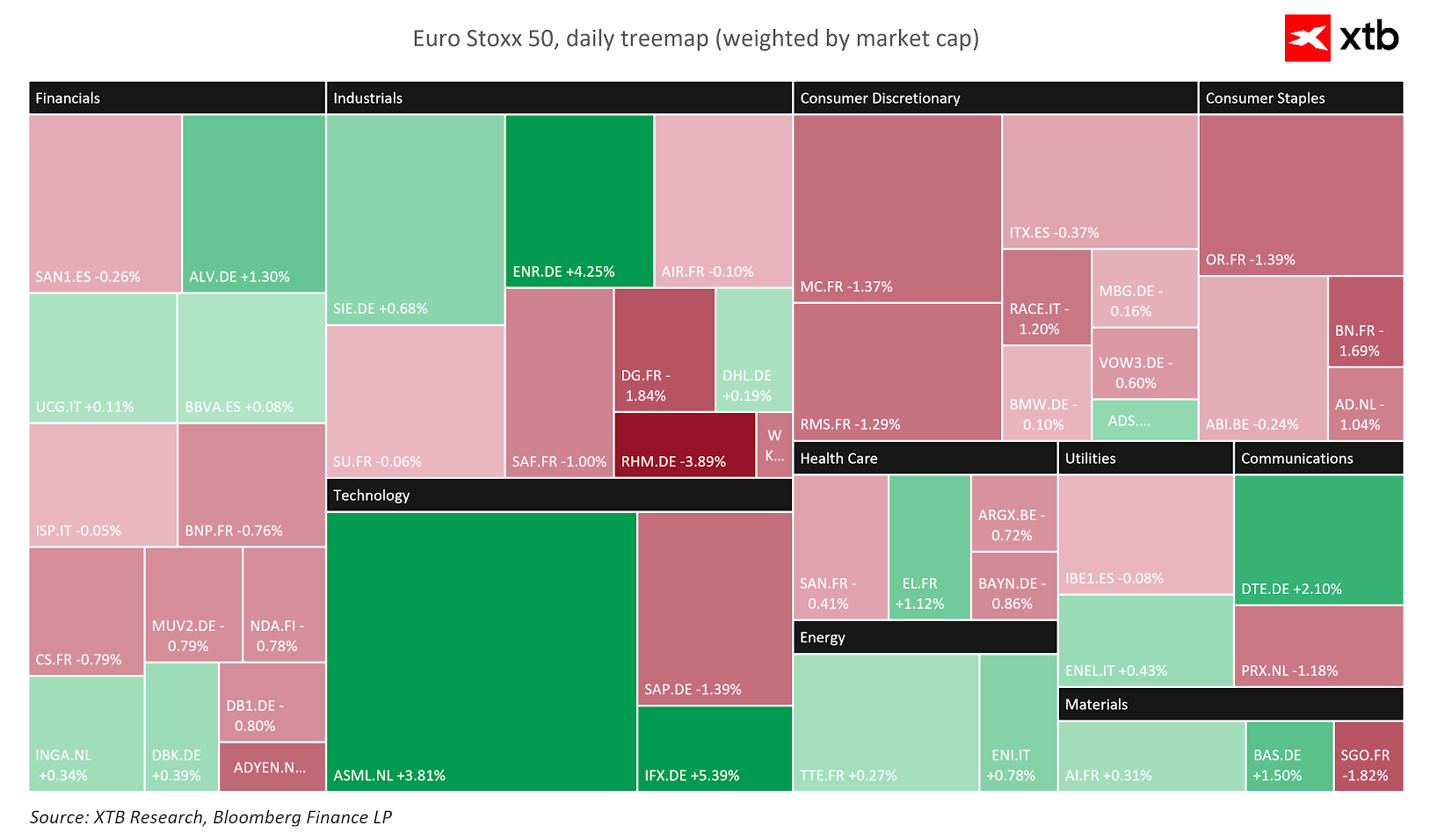

Sector dispersion highlights strong gains in ASML and Infineon, while consumer sector stocks are underperforming. Source: XTB

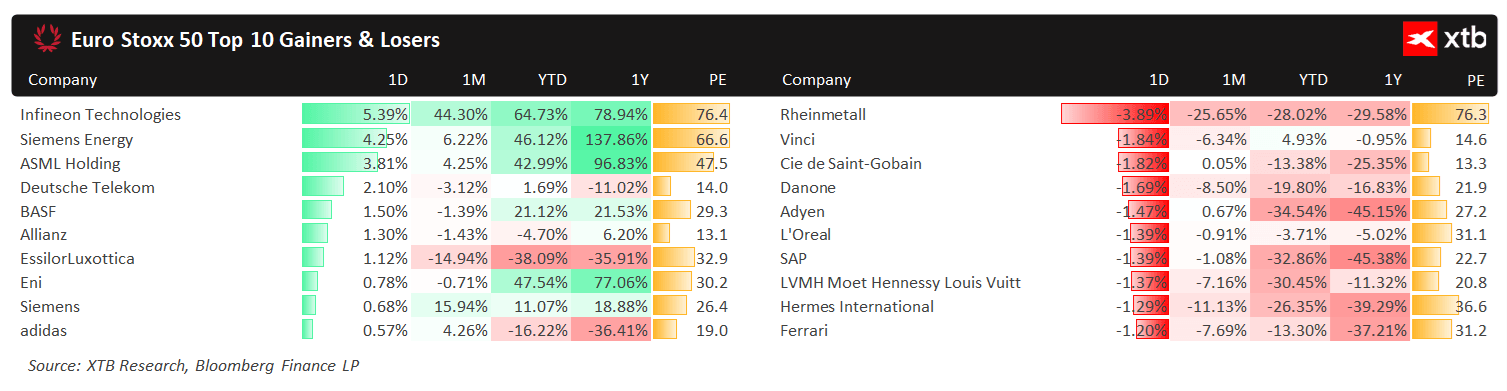

Among the most closely watched companies today are Siemens and Deutsche Telekom, both gaining on strong earnings. Meanwhile, Rheinmetall is extending its recent decline. Source: XTB

SpaceX Preview: It's Time to See How Much of Its Valuation Is Based on Business and How Much on Promise

BREAKING: US ISM Manufacturing - Strong Beat Across the Board

Eurozone PMIs: German Factory Revival Masks Underlying Stagnation 🇪🇺

Chart of the Day: Yen Falls From 40-Year Highs – What’s Next? (03.08.2026)