-

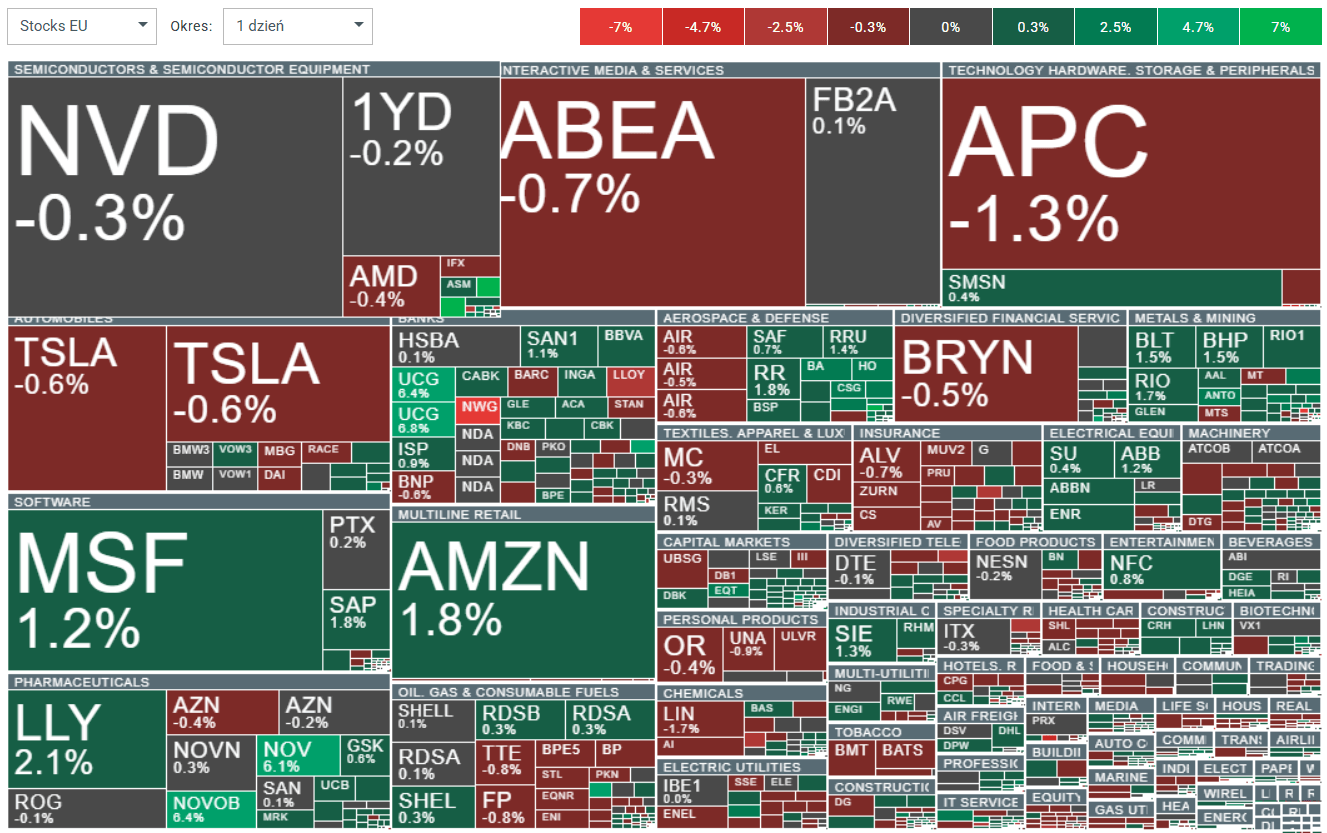

European equities held on to modest gains, but market tone remained selective and highly differentiated. Quarterly earnings are generally solid, yet investors are reacting critically even to small deviations from guidance, highlighting a still demanding market environment compared with US equities.

-

At the time of writing, the Stoxx 600 is up 0.25%, remaining near record-high levels. Germany’s DAX gains 0.23%, Italy’s ITA40 rises 0.98%, Spain’s SPA 35 adds 0.35%, while the UK’s UK100 declines 0.60%.

-

Companies in the Stoxx 600 are on track for roughly 8% EPS growth in 4Q; 61% have beaten EPS expectations and 58% have exceeded revenue forecasts. Despite this, upside potential for the index remains limited, as market reactions are often negative and 2026 guidance has failed to meet elevated expectations.

-

Tariff-sensitive companies delivered the strongest earnings beats in a year, while China-exposed names and purely EU-focused companies underperformed. Value, growth, and quality stocks beat expectations more consistently than momentum and small caps.

-

AI-risk niches under pressure: software, data services, publishers, financial information providers, alternative asset managers, and gaming stocks declined as markets priced in medium-term margin risks from AI-related disruption.

Key single-stock moves (Europe)

-

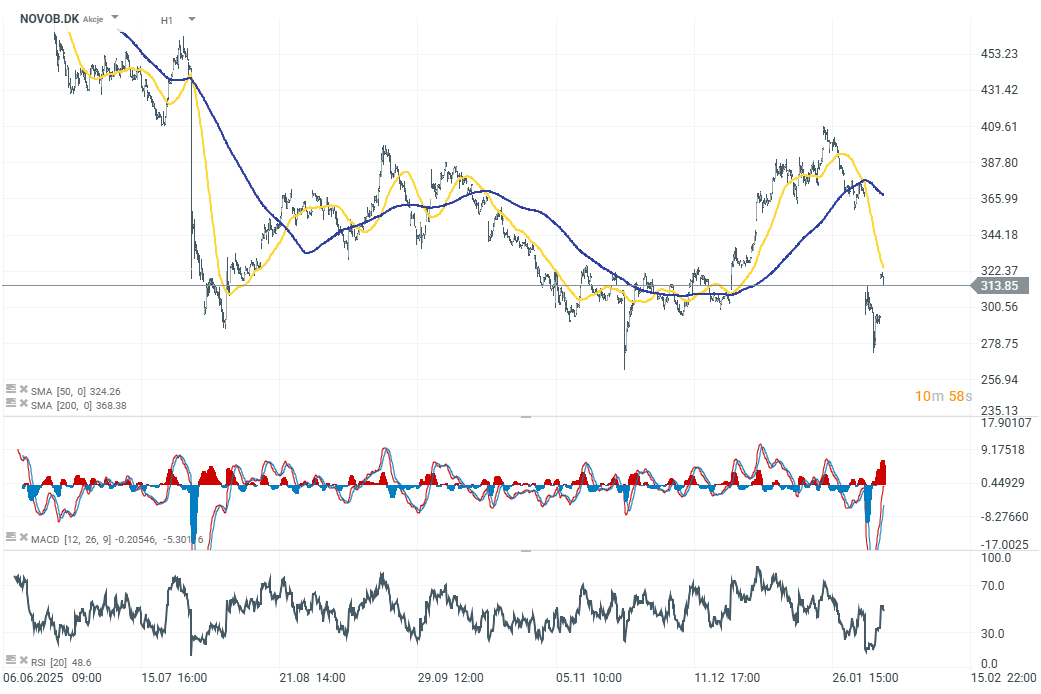

Novo Nordisk rebounds +7% after last week’s nearly 25% correction, following Hims & Hers’ announcement that it will stop selling Wegovy copies after the FDA tightened enforcement.

-

UniCredit rises +4% after presenting strong outlooks through 2030 and plans to return around €50bn to shareholders by 2030.

-

InPost surges +13% on takeover interest valuing the company at €7.8bn.

Global macro

-

Japan’s ruling LDP secured a supermajority, keeping the Takaichi trade in focus and reinforcing expectations of fiscal expansion.

-

The proposed two-year suspension of the food sales tax is seen as highly likely and is estimated to create a ~¥5trn annual fiscal gap, with key implications for bonds and FX.

-

The yen strengthened following verbal intervention by Japanese authorities. USDJPY is down 0.50%, and the yen is among the stronger G10 currencies despite Takaichi’s decisive victory.

-

Precious metals remain strong: gold is testing the $5,000 level, up 1.0% on the day, while silver gains 2.40% to $97.

Daily Summary: Equities Diverge as Tech Lags, Europe Rallies on Earnings & PMIs (24.07.2026)

Three markets to watch next week (24.07.2026)

US OPEN: Nasdaq hits 1-month low! Geopolitics bring AI trade down!

Market Wrap: European Stocks Are Trying to Rebound as the Week Comes to an End💡