European stock indices are trading without a clear direction on Friday — the Euro Stoxx 50 is down 0.13% and the DAX (DE40) is down 0.16%, whilst S&P 500 futures (US500) remain slightly in positive territory (+0.12%) . The main factor driving market caution is the ongoing war with Iran and its pressure on energy commodity prices, which is translating into rising inflation and revisions to interest rate expectations in the eurozone. Strategists are increasingly warning that if the Strait of Hormuz remains closed for an extended period, a bearish scenario for European equities could become a reality.

It is worth noting that although analysts’ average year-end target for the Stoxx Europe 600 stands at just 624 points—suggesting less than 1% upside potential—the picture regarding earnings per share (EPS) revisions remains positive. Blended forward EPS for the Stoxx 600 has been rising consistently for years, and the consensus expects double-digit EPS growth in 2026 — supported by the energy sector and a rebound in consumption. If this trajectory continues, analysts will be under pressure to revise their price targets upwards, which could narrow the gap between current prices and forecasts. Source: Bloomberg Financial Lp

WTI crude oil remains above the $98 per barrel mark (+0.20%), fuelling concerns about corporate margins and consumer purchasing power. The US dollar (USDIDX) remains stable with a minimal rise of 0.08%, whilst the EURUSD pair is down 0.13% to 1.1604. In this trading environment, gold is down slightly (-0.21%), suggesting that the market is not yet aggressively seeking safe havens.

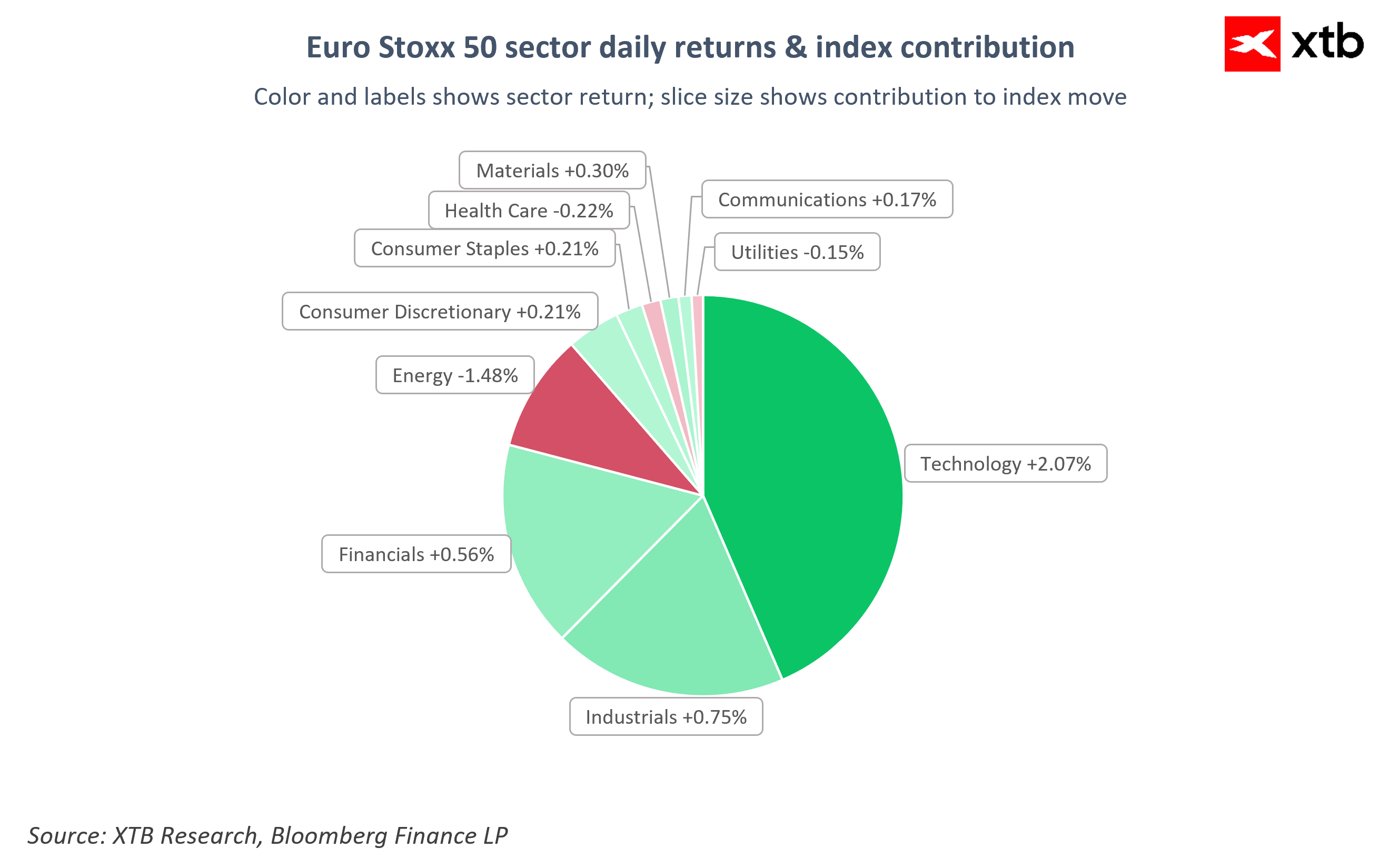

The technology sector is performing best in the Euro Stoxx 50, rising by as much as +2.07% and making a significant contribution to the index’s movement.

Source: XTB

The industrial sector (+0.75%) and the financial sector (+0.56%) are also performing well. On the other side of the fence is the energy sector, which, with a result of -1.48%, is by far the weakest sector of the day — pressure on TotalEnergies (-1.51%) and Eni (-1.41%) is dragging the sector down. Losses are also being recorded in Health Care (-0.22%) and Utilities (-0.15%).

Source: XTB

Company information

-

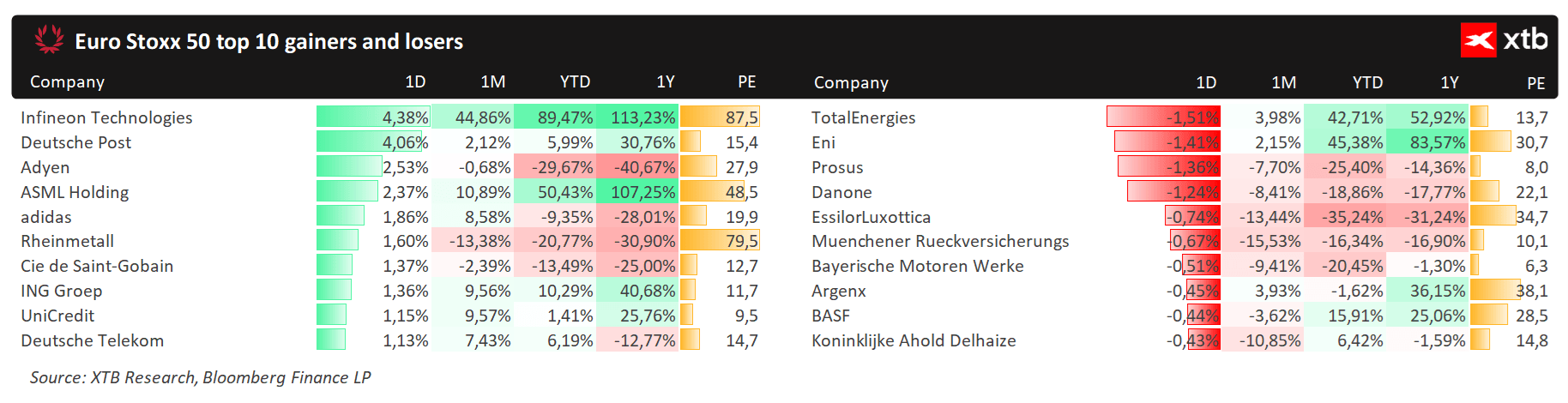

Richemont — the owner of the Cartier brand — has published its annual results, which received a mixed reception from the market: shares initially jumped by over 5% before eventually falling by 1.9%. The group’s sales rose to €22.42 billion (+4.8% y/y), and at constant exchange rates, growth reached +11% against a consensus forecast of +9.78% — clearly beating expectations. The star performers were the Jewellery Maisons, whose sales at constant exchange rates rose by 14% against a forecast of 13%, with the segment’s operating margin standing at 30.5%. The results were overshadowed by unfavourable exchange rates — operating profit stood at EUR 4.49 billion compared to the EUR 4.60 billion expected by the market, and the group’s operating margin shrank to 20.0% from 20.9% a year ago. Richemont proposed a dividend of CHF 3.30 per share (consensus: CHF 2.93), which Vontobel analysts described as confirmation of the quality and the management’s confidence in future earnings — despite currency headwinds, they believe the company remains a “quality compounder” in a volatile sector.

-

Deutsche Post (DHL) has jumped by over 4% following an upgrade by Deutsche Bank, which believes that the cycle of downward earnings revisions has come to an end and that concerns about disruption from AI and increased competition are overstated.

-

Puig — a Spanish cosmetics company — has seen its share price fall by a record 15% following the collapse of merger talks with Estée Lauder. Earlier reports had suggested that Estée Lauder had commissioned JPMorgan to structure a €5 billion financing package for a potential takeover.

-

Julius Baer has fallen by more than 10% following a disappointing earnings report — weak net asset inflows fell short of analysts’ expectations, even though the shares had risen by 9% year-on-year as of Thursday.

-

Softcat is up by up to 12% after the company raised its annual operating profit forecast — analysts point to an acceleration in orders and expect the consensus forecast to be revised upwards.

Daily Summary - Oil gains due to uncertainty, market awaits inflation data

⬆️Oil back above $88

US Open: Nasdaq Seeks Direction 🗽 Hims & Hers Shares React to Earnings

⚫Commodity wrap - Oil, Gold, Natgas, Emiss (11.08.2026)