Tomorrow after the market close, Nvidia will release its results for the fourth quarter of fiscal year 2026. This report goes far beyond standard financial results and will become a key reference point for the semiconductor market, institutional investors, and participants in the AI sector.

Nvidia is no longer just a chip manufacturer. The company has become a barometer for the entire technology sector, and its results reflect demand for AI in data centers, hyperscaler spending, and the adoption pace of new GPU generations such as Blackwell and H200. The report will show whether Nvidia’s product demand is based on stable, long-term contracts or whether the market has overestimated AI expectations.

Why this report is critical

Nvidia’s weight in the market and indices

Nvidia holds the largest weighting in the S&P 500 technology sector and is a key component of the Dow Jones Industrial Average. Its share price exerts a significant influence on indices and ETFs tracking the market. The market reaction to NVDA’s results this quarter could determine the direction of the entire semiconductor sector and sentiment in technology indices.

Hyperscaler spending test

Amazon, Google, Microsoft, and Meta continue to increase spending on data centers and AI infrastructure. Nvidia is the primary beneficiary of these investments, and the report will show whether GPU revenue growth is truly driven by sustainable demand or merely one-off orders in the AI hype environment. The pace of hyperscaler spending will serve as a barometer for how strongly these companies believe in AI’s long-term potential.

Blackwell and H200

New GPU generations, including Blackwell and H200, will be closely watched by investors. Their adoption by corporate clients, including in China, will indicate whether Nvidia maintains its technological edge and captures market share in the growing AI sector. The report will also test the “peak AI 2026” narrative. GPU revenue growth in recent years has been spectacular, but the question of whether AI will remain a lasting growth driver remains open..

Market expectations

-

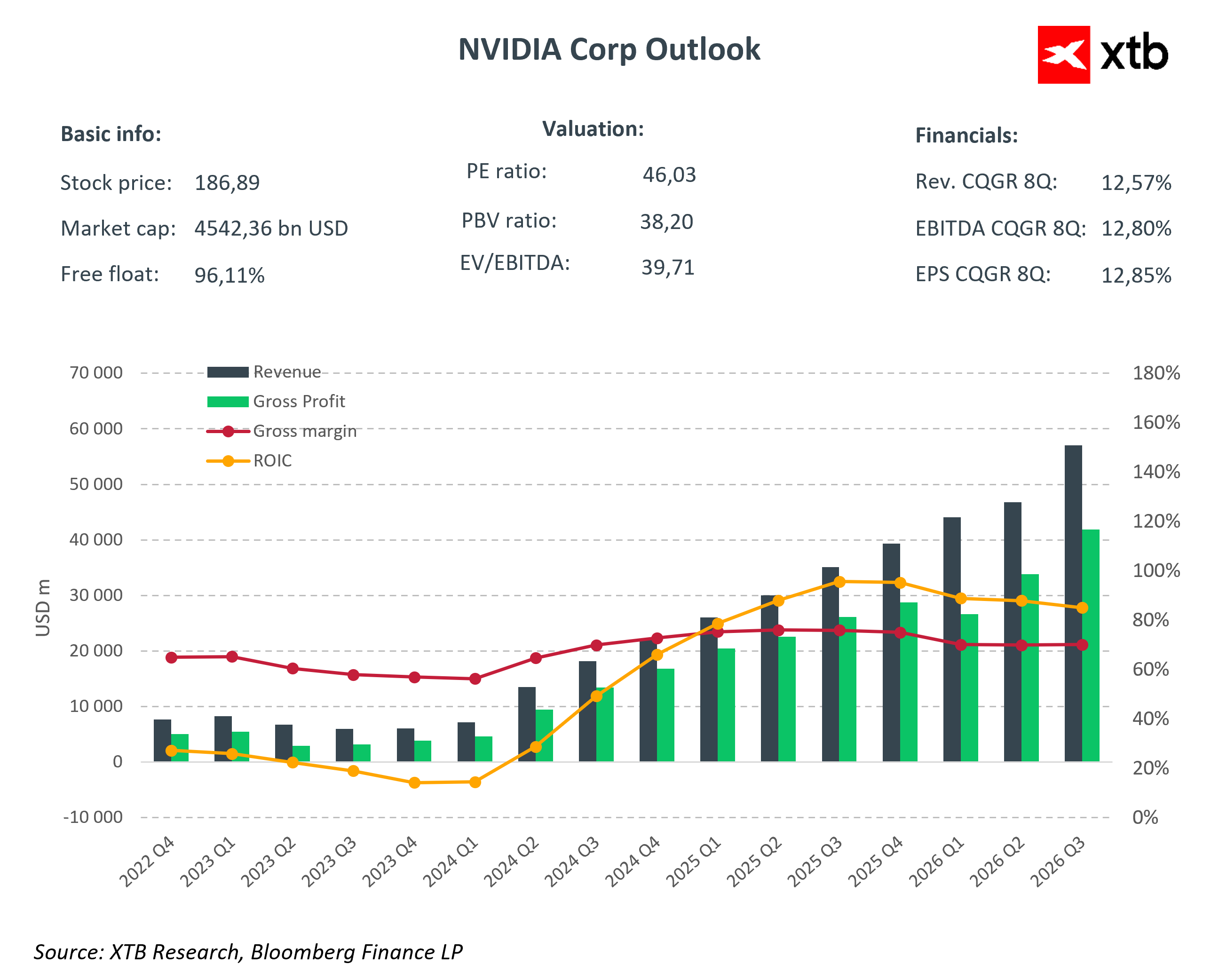

Q4 2026 revenue: 65 to 66 billion USD versus 39.33 billion USD last year. This represents 66–67% year-on-year growth driven by accelerated AI adoption and increased hyperscaler orders.

-

Adjusted EPS: 1.50–1.53 USD versus 0.89 USD last year. The market expects confirmation of strong profitability despite rising investment levels.

-

Q1 FY2027 guidance: around 72.4–72.5 billion USD, implying continued growth of ~64% year-on-year and providing insight into whether the “peak AI” narrative will hold in the coming year.

-

Historical context: Nvidia has beaten revenue forecasts for 13 consecutive quarters and EPS for 12 consecutive quarters, setting an exceptionally high bar.

What really matters

Data Center and AI

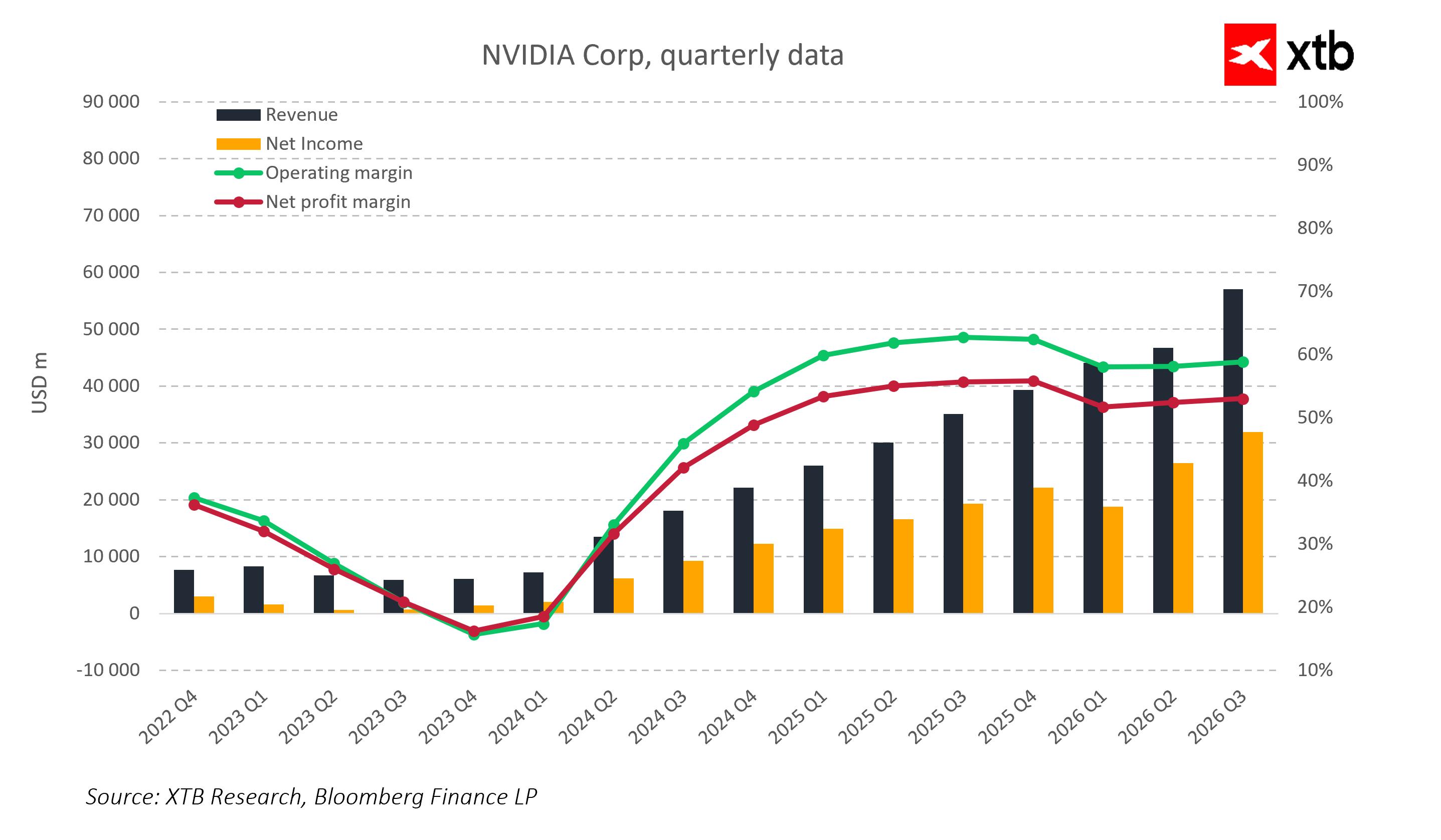

The Data Center segment is the heart of Nvidia’s strategy. Revenue growth in this segment is not solely driven by gaming GPU demand but primarily fuels the AI business. Investors will analyze the adoption pace of Blackwell and H200, the number of deployments in hyperscaler data centers, and the revenue split between training and inference. This will help assess whether GPUs generate a stable demand cycle that can continue over the coming years and whether the product pipeline, including projects like Vera Rubin, provides a competitive advantage for 2026–2028.

Blackwell and H200 in China

The H200 could generate 3–3.5 billion USD in quarterly revenue. This is significant as the Chinese market remains a key revenue source. The adoption pace of these chips and the impact of export restrictions will indicate to what extent geopolitical factors could limit revenue scaling and affect Nvidia’s global strategy.

Margins and component costs

In previous quarters, gross margins hovered around 73–74%, and management has indicated the goal of maintaining a mid-70s level. Consensus expects the company to sustain very high margins despite rising HBM memory costs and expanded production capacity, partly through long-term component price agreements. Investors will scrutinize commentary on product mix, discount levels for key clients, and the impact of new GPU generations on margins.

Hyperscaler CapEx and business scaling

Increasing spending by Amazon, Google, Microsoft, and Meta demonstrates confidence in AI’s long-term potential but also presents challenges for Nvidia’s profitability. Investors will watch whether the company can grow revenue while maintaining high gross and operating margins and how efficiently it manages costs amid rapidly growing demand.

Market reaction scenarios

The Nvidia report will be perceived not just as a single company’s result but as a barometer for the entire AI and semiconductor market. After 13 consecutive quarters in which NVDA consistently beat forecasts, expectations are extremely high. Even strong results could be considered neutral if guidance or management commentary falls short of market ambitions.

In a positive scenario, meaning a strong beat in revenue and EPS, guidance for 2027 exceeding expectations, and faster-than-anticipated adoption of Blackwell and H200 in China, a dynamic reaction across the semiconductor sector can be expected. NVDA’s rise would likely lead to gains among competitors and generate positive sentiment in technology ETFs and indices such as the S&P 500. The narrative of a sustained AI boom would be reinforced, potentially encouraging institutional investors to increase allocations to AI- and data center-related companies.

In a neutral scenario, market reaction would likely be muted. Results in line with expectations and stable guidance for 2027 probably will not generate strong price movements or materially change sentiment across the sector. Nvidia shares would remain stable, as would competitor stock prices and major indices, with the report confirming the existing growth trajectory without providing an additional impulse for aggressive buying or profit-taking.

In a negative scenario, revenue or EPS disappointment, weaker guidance, slower adoption of Blackwell and H200 in China, and margin pressure could trigger a broad semiconductor market correction. NVDA would likely decline, affecting competitors, ETFs, and technology indices including the S&P 500. Enthusiasm for AI could cool, and investors may adopt a more conservative view on sector growth prospects for the upcoming quarters.

Regardless of the scenario, the Nvidia report will drive short-term market volatility. Every nuance in management commentary regarding demand, hyperscaler CapEx, margins, or the situation in China will be carefully analyzed and could trigger significant price movements.

Key takeaways

-

Nvidia serves as a test of the durability of the AI boom and the scalability of GPUs in data centers.

-

The report will indicate whether hyperscaler spending translates into real revenue and whether demand for Blackwell and H200 is stable, including in China.

-

Margins and management commentary on inference versus training will reveal whether GPU demand will remain strong in the coming years.

-

Guidance for 2026 and 2027 will signal whether the “peak AI 2026” narrative is justified or if investors should adjust expectations.

-

NVDA’s results will impact the semiconductor sector, the S&P 500, and overall technology and AI sentiment.

-

The adoption pace of H200 in China and management comments on export restrictions could add further volatility.

-

The report will test Nvidia’s ability to scale AI investments effectively while maintaining high profitability and competitive advantage.

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Morning Wrap: AI Fuels the Rebound. Technology Makes a Strong Comeback

Apple is still impressive, but the market is no longer impressed

Amazon’s massive AI bet is starting to pay off