After Monday’s session closes, the controversial technology company Palantir will publish its results. Specializing in AI technology, data aggregation, and surveillance, the company is known not only for its extreme growth rate but also for sharp market reactions to earnings releases. What will happen this time, and what should investors pay attention to?

Looking at basic metrics such as revenue and EPS, Palantir has beaten the market consensus in every earnings call since mid-2023.

At today’s call, the market expects revenue above USD 1.5 billion and EPS of 0.28. This implies a quarter-on-quarter profitability increase of more than a dozen percent and an increase of over 200% year on year.

However, these profitability measures are only the tip of the iceberg when analyzing companies as complex as Palantir.

With valuation multiples as high as Palantir’s, any disappointment can trigger a wave of selling. At the same time, even a slight beat on key items can result in euphoria. This is a straightforward consequence of the company’s enormous operating leverage and growth rate.

To defend the bullish thesis, the company must address several risks during the call and in the results themselves:

Pressure from commercial LLMs, companies such as OpenAI and Anthropic are increasingly pushing into a segment that has so far been the domain of firms like Palantir. The company needs to show that this is not a threat to its growth. It can do so by:

- Demonstrating growth in RPO & cRPO

- Reinforcing market confidence in the guidance, or even raising it,

- Reporting the net revenue retention rate (a key metric for SaaS companies), which will help assess whether Palantir’s business model is threatened in any way.

Other areas investors should watch include Palantir-specific operational efficiency metrics, such as:

- Implementation time and efficiency, and the length of the transition from pilot stages of the service to a production version—this will indicate how effectively the company handles the significant challenges of deploying and integrating complex solutions and legacy databases across many organizations.

- Balance in customer growth, an excessive increase in the share of the government sector in the company’s growth may raise concerns about the health of the commercial segment and about the company’s priorities. Strong growth in sales outside the US would also be welcomed.

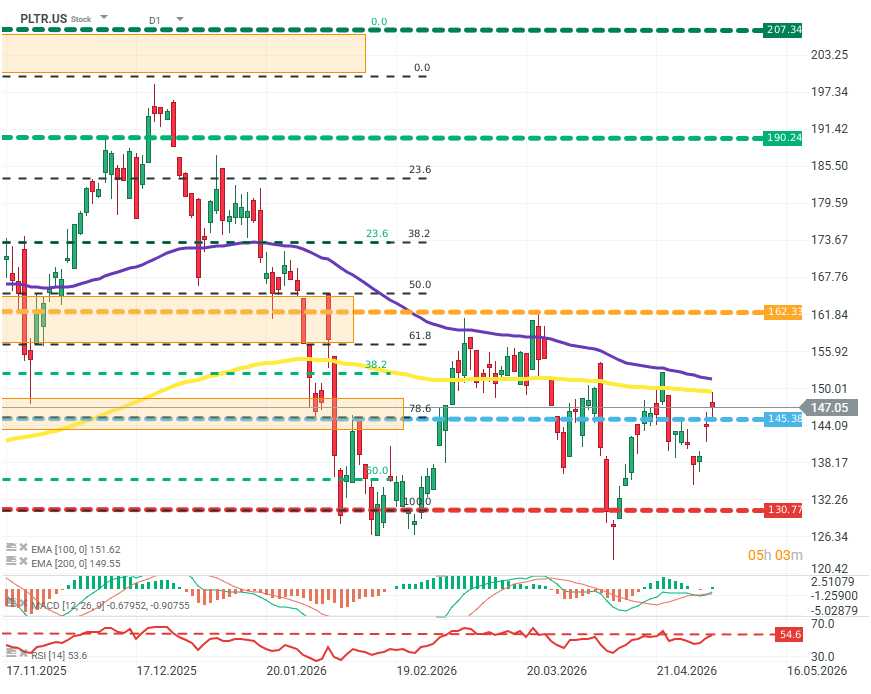

PLTR.US (D1)

Despite the predominantly negative sentiment during Monday’s session, driven by escalating tensions in the Strait of Hormuz, sentiment toward the stock remains positive ahead of earnings. Since the start of the year, the price has been moving in a consolidation channel between roughly USD 160 and 130. The trend of the EMA100 and EMA200 moving averages remains bullish; however, they are close to crossing, which would be a strong bearish signal. Source: xStation5.

Texas Instruments earnings: Growth without cash

All or nothing: ServiceNow earnings preview

Did SaaS lost too much? Morgan Stanley says yes.

US OPEN: The market extends losses as investor concerns grow