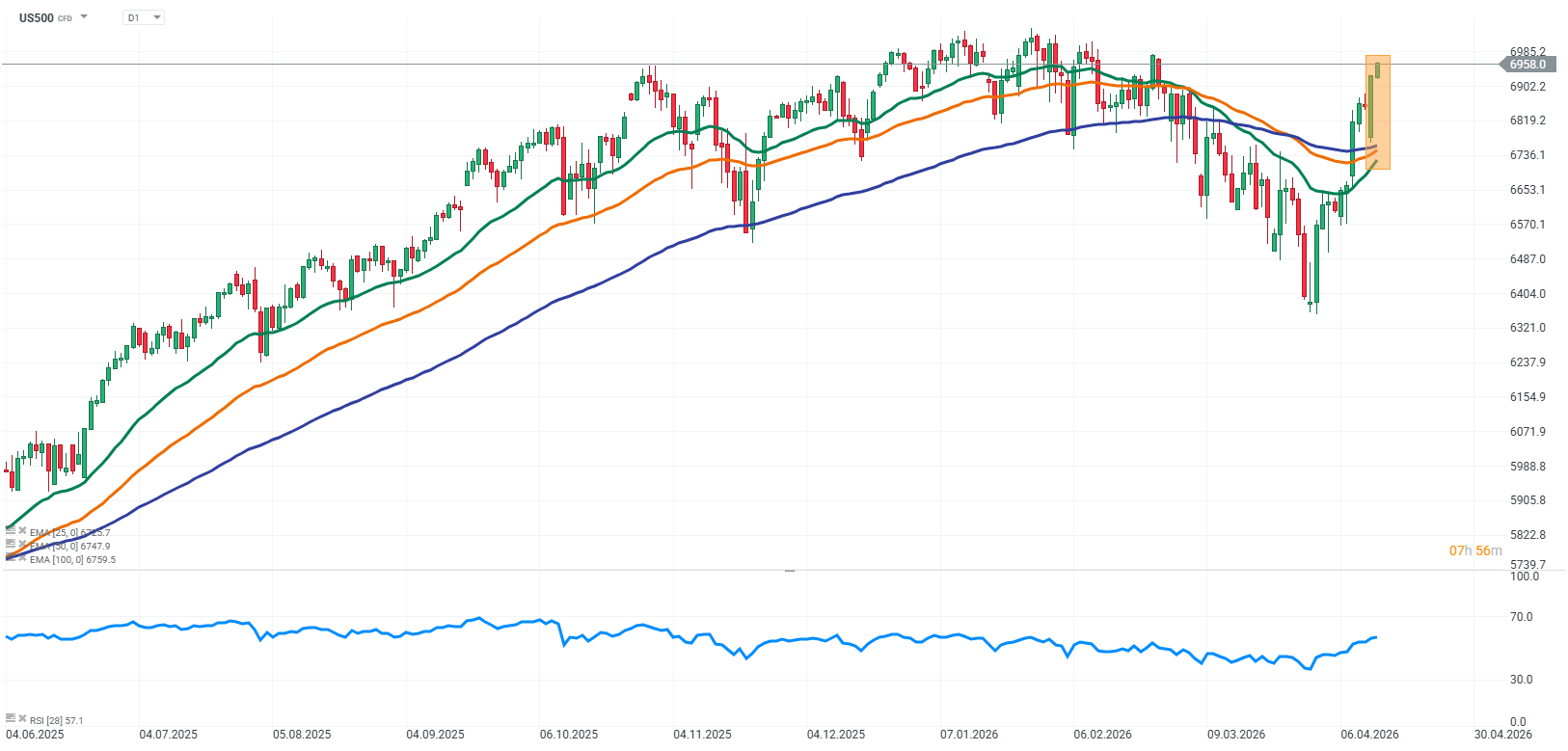

Wall Street is increasingly leaning into a narrative of risk de-escalation rather than escalation, which in the current environment is becoming a key source of short-term support for valuations. The market appears to be shifting from a defensive stance toward a more pro-growth positioning, pricing in a scenario of gradually easing geopolitical tensions or at least their stabilization at levels that do not generate further macroeconomic shocks. This is not yet a full conviction about a durable improvement in fundamentals, but rather a rapid re-rating of the risk premium, which is declining faster than real economic data are changing.

In this context, today’s PPI reading is particularly important, as it came in significantly below expectations. Producer-level price pressures are not accelerating to the extent the consensus had anticipated, despite ongoing tensions in global trade and energy markets. The market interprets this as a signal that cost pressures are not transmitting as strongly through the broader economy as previously feared in more pessimistic scenarios. This does not yet indicate full disinflation, but it shifts the balance of risks toward a more neutral and controlled inflation environment.

At the same time, the earnings season in the banking sector is delivering mixed signals. Overall, U.S. banks are reporting solid but not outstanding results, highlighting that the environment remains challenging and far from euphoric. There are clear “flies in the ointment” in these reports, whether in the form of more cautious guidance or weaker momentum in certain business segments, which tempers enthusiasm and reinforces the view that current market conditions remain uncertain. Nevertheless, the financial sector continues to show solid profitability, particularly driven by trading activity and relatively stable investment banking flows, which helps prevent a deterioration in sentiment.

Combining these factors — a softer-than-expected PPI reading, mixed yet resilient bank earnings, and rising expectations of geopolitical de-escalation — we get a classic setup supporting further upside moves. In such an environment, the market does not require a strong upward revision of growth expectations; instead, a reduction in tail risks and a compression of the risk premium are sufficient for indices to continue rising.

The key question for the coming sessions is whether this move represents the beginning of a durable regime shift in markets or rather a short-term “hope repricing” phase, where investors are too quickly pricing in geopolitical and inflation stabilization. History shows that such de-escalation-driven optimism phases can be very dynamic, but they can also reverse just as quickly if any of the key drivers — energy, geopolitics, or services inflation — begin to escalate again.

Source: xStation5

US S&P 500 (US500) futures are posting moderate gains today, with one of the key supporting factors being a weaker-than-expected U.S. PPI reading. The data indicate that producer-level price pressures are not accelerating as much as the consensus had forecast, reducing concerns about a renewed inflation wave driven by costs. The market interprets this as a sign that the inflationary impulse from the supply side remains under control, supporting risk assets.

Source: xStation5

Company News

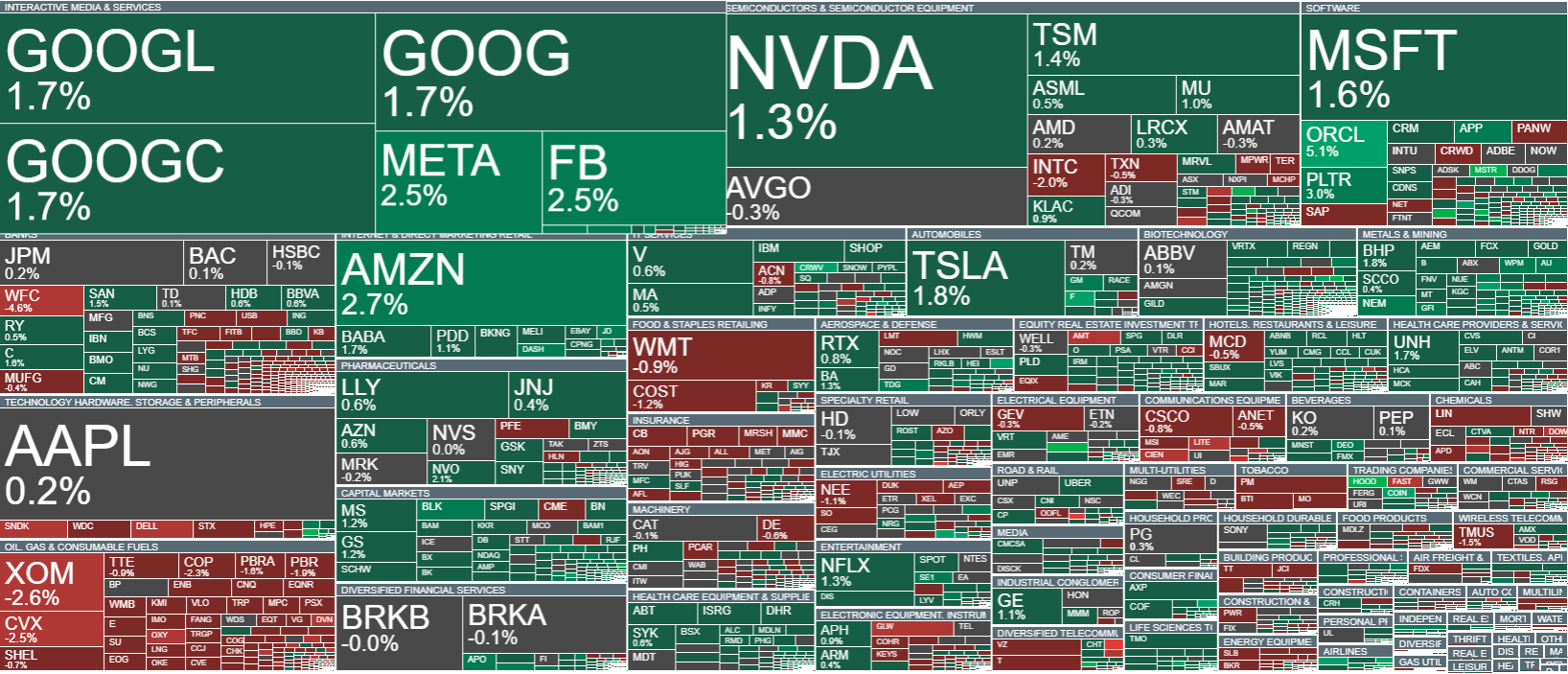

Wells Fargo (WFC.US) disappointed the market despite earnings growth, as the quality of results was weaker than expected and largely driven by one-off factors and less balanced business performance. Investors are also paying attention to more cautious credit reserve assumptions and mixed signals across business segments. As a result, the stock is trading lower.

Key financial figures:

-

Revenue: USD 21.45 billion, about USD 340 million below expectations

-

Net income: around USD 5.3 billion, up year-over-year

-

EPS: USD 1.60, beating estimates by USD 0.02

BlackRock (BLK.US) reported very strong Q1 2026 results, significantly beating expectations thanks to robust ETF inflows and higher asset management fees. Additional support came from higher performance fees and business scale expansion, pushing assets under management to record levels.

Key financial figures:

-

Revenue: USD 6.7 billion vs. expected ~USD 6.4 billion

-

Operating income: up 31% to USD 2.67 billion

-

Operating margin: increased to 44.5%

-

EPS: USD 12.53 vs. expected ~USD 11.5

JPMorgan Chase (JPM.US) delivered stronger-than-expected Q1 2026 results, supported by solid trading revenues and investment banking strength, along with overall business resilience. Earnings and revenue surprised positively, confirming the strong condition of the financial sector in a high-volatility environment.

However, the report was not entirely positive, as the bank lowered its full-year net interest income (NII) outlook, which tempers part of the optimism regarding future earnings momentum. This creates a typical “beat now, weaker outlook later” dynamic, limiting overall investor enthusiasm despite solid quarterly performance.

Key financial figures:

-

Revenue exceeded USD 50 billion vs. expected USD 49.2 billion

-

EPS: USD 5.94 vs. expected ~USD 5.45

-

Net interest margin (NIM): 2.5% vs. expected 2.57%

IonQ (IONQ.US) is rising after being included in DARPA’s Quantum Benchmarking Initiative, a program aimed at advancing and evaluating quantum computing technologies. This is not yet a large guaranteed contract, but rather participation in a government R&D program with potential for future awards.

Economic Calendar: PayPal, Visa and Coca-Cola to overshadow macro data (28.07.2026)

Morning Wrap: US halt to attacks balanced by semiconductor sector declines (28.07.2026)

Daily Summary: Chip War Weighs on Wall Street as Oil Plunges After US–Iran Ceasefire ⭐

Nasdaq-100 under pressure after chip sell-off