The global wheat market is entering a critical phase, with CBOT wheat futures (WHEAT) attempting to maintain an upward trend. Production may decline this year, but there are also signs that weather conditions could partially reverse earlier negative expectations. Prices are currently reacting to a mix of factors, ranging from weather developments to shifts in global trade flows.

- Weather impact on prices: Rainfall in the Black Sea region and improving conditions in the US are temporarily easing upward price pressure, although earlier drought conditions are still affecting crop quality.

- Weaker US export data: Export performance remains disappointing, which is limiting price upside despite supply concerns in other regions.

- Russia and India as key players: Russia is reporting weaker harvests due to cold weather, while India is considering wheat imports, which could reshape global trade flows.

- Challenges in Argentina: Reduced planting area and high production costs are constraining supply potential from South America.

- Mixed situation in the US: Improved weather conditions contrast with earlier yield losses and signs of weaker export demand.

- Range-bound market structure: Prices are moving within a broad range, and the lack of a clear breakout reflects uncertainty about the next directional move.

WHEAT (D1 interval)

Source: xStation5

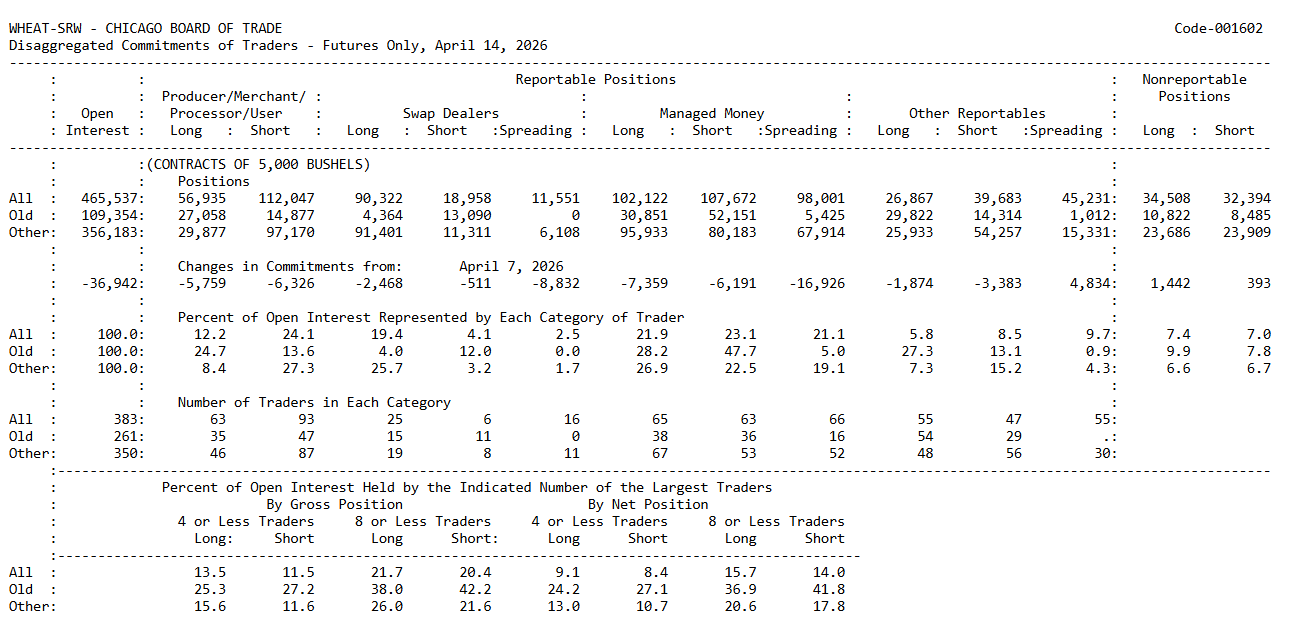

What does the Commitment of Traders report suggest?

To better understand the “what next” question for the wheat market, it is useful to look at positioning among large traders and hedgers. The key takeaway is that both commercial participants (producers and physical market players) and managed money (large speculative funds) are currently net short—but for very different reasons.

Commercials maintain a significant net short position, which is typical for agricultural markets, as they hedge future physical sales. Managed money is also net short, but only marginally. This is important, as it suggests that funds do not currently hold strong conviction in a sustained bullish move, despite ongoing weather-related risks.

Commercial positioning: still clearly defensive

Commercial traders hold 56,935 long contracts and 112,047 short contracts, resulting in a net short position of approximately 55,112 contracts. This reflects a strong bias toward hedging future supply and indicates that producers are not positioning for a sharp and sustained price rally. If expectations for a strong upside move were high, this short hedge would typically be lighter.

Managed money: slightly net short, without strong conviction

Managed money holds 102,122 long contracts and 107,672 short contracts, resulting in a modest net short position of around 5,550 contracts. While more neutral than commercials, funds are still not positioned on the long side. This suggests that the market is not in a typical setup where commercials are short and funds are aggressively long. Instead, both groups lean short, with different motivations.

Compared to the previous week, commercials reduced both long and short positions, slightly narrowing their net short exposure, but without any meaningful shift in hedging behavior. Managed money reduced long positions more aggressively than shorts, leading to a slightly deeper net short position. From a trading perspective, this indicates that funds are not building new long exposure and are instead scaling back participation.

Market interpretation

In a strong bullish environment, it is common to see commercials hedging while speculative capital takes the long side. That dynamic is currently absent. Funds are not stepping in to buy the market despite potential supply-side risks. This suggests that the wheat market has not yet developed a narrative strong enough to attract broader speculative interest.

As long as managed money remains slightly net short, any price increases may be driven more by short covering or temporary factors rather than a sustained bullish trend. At the same time, the current positioning leaves the market vulnerable in both directions. On one hand, it does not confirm a strong bull market. On the other, it leaves room for a sharp short-covering rally if a significant weather or export shock emerges.

Open interest declined by 36,942 contracts to 465,537, which is a meaningful move. This suggests that some market participants are closing positions rather than building new directional exposure. When open interest falls and funds are not shifting into long positions, it typically signals a lack of broad conviction in a sustained upward move.

Final takeaway

The Commitment of Traders report does not yet provide a clear bullish signal. The key issue for bullish participants is that speculative capital is not willing to take the opposite side of commercial hedging. Commercials continue to hedge aggressively, while managed money does not see sufficient reason to build strong long exposure.

This indicates that the wheat market remains in a phase where fundamental risks exist, but have not yet translated into strong conviction among speculative investors. A clear shift of managed money toward a net long position would be a more meaningful signal that the market is beginning to price in a genuine supply-side imbalance, rather than short-term weather-driven noise.

Source: Commitment of Traders, CFTC 14 April

🛢️Brent Crude Oil Tests $95 per Barrel

Morning Wrap: AI companies and gold back in favour? (22.07.2026)

Daily Summary: Semiconductors Rise in the Shadow of Geopolitical Turmoil

Tech sector catches its breath 🚀