US index futures are trading higher today ahead of the 14:30 NFP release, with the US100 jumping more than 0.8% and approaching the 29,000 level, while the US500 gains 0.6%. The rally continues to be supported by a record-breaking US earnings season, with broad-based growth in profits and revenues across the S&P 500, net profit margins rising to their highest level in 15 years at 13.5%, and AI-driven optimism continuing to support market sentiment.

Estimated EPS growth for the S&P 500 points to a sharp acceleration in year-over-year earnings growth compared with an already strong 2025. Earnings growth in the technology sector is expected to reach 46% YoY versus nearly 28% last year, while the energy and materials sectors are also projected to post substantial gains. According to Charles Schwab and LSEG data, companies across nearly all sectors — except healthcare, financials, and industrials — are expected to significantly outperform last year’s EPS growth pace.

US100 chart (D1 interval)

Source: xStation5

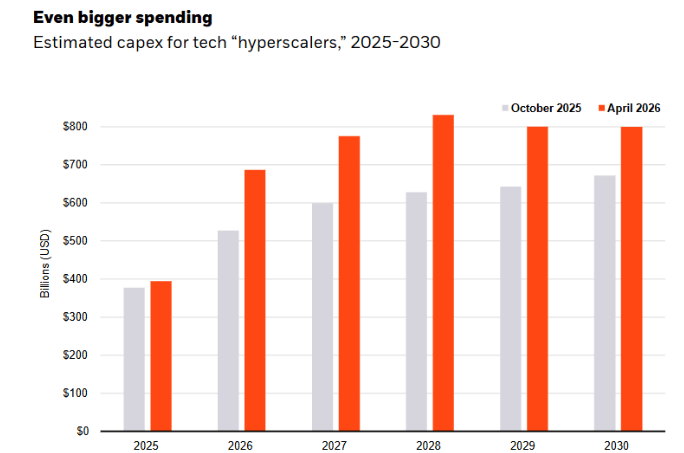

CAPEX spending by tech giants continues to rise

According to BlackRock Investment Research, projected AI hyperscaler CAPEX has increased by 25% compared with October last year. This is positive news for semiconductor companies and AI infrastructure firms, as it implies further market expansion and supportive trends for both revenue and earnings growth. On the other hand, any meaningful economic slowdown could have a sharp negative impact on valuations and sentiment.

Source: BlackRock

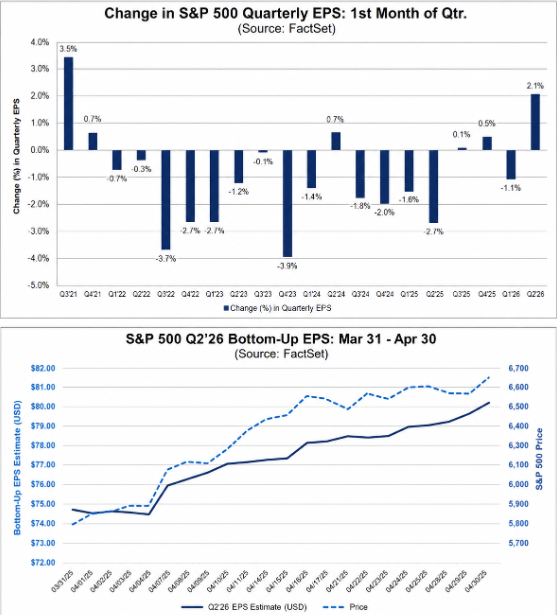

Forecasts are rising while Big Tech continues to dominate

Analysts raised Q2 2026 EPS forecasts for S&P 500 companies by 2.1% in April, despite the fact that expectations are typically revised lower at the start of a quarter. Over the past 20 years, the average first-month quarterly EPS revision has been -1.9%. The current increase marks the largest upward revision since Q2 2021, when forecasts rose 3.5% following the post-pandemic recovery.

The energy sector recorded the strongest upgrade in earnings expectations, with forecasts rising by 45.1%. At the same time, five out of eleven sectors saw deteriorating expectations, with industrials remaining the weakest area as forecasts declined by nearly 3%. Analysts also raised full-year S&P 500 earnings forecasts by 3.4% during April.

Source: FactSet

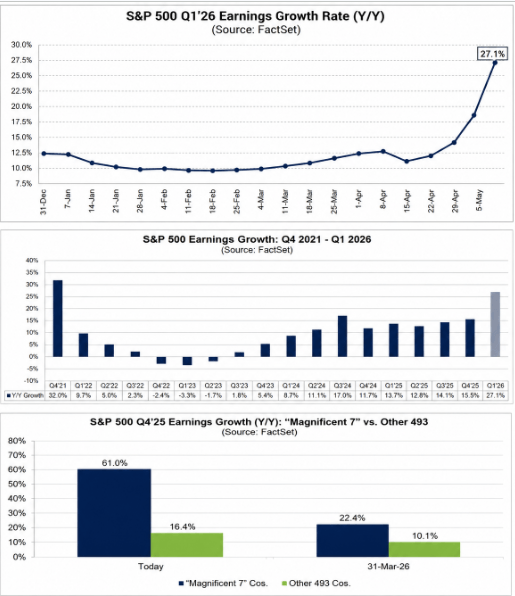

Following Big Tech earnings, the blended earnings growth rate for the S&P 500 in Q1 2026 surged to 27.1% from 15% just a week earlier, marking the strongest result since late 2021. The strongest earnings growth has been reported by Communication Services (+53.2%), Technology (+50.0%), and Consumer Discretionary (+39.0%), driven primarily by megacap companies.

Alphabet, Amazon, and Meta alone accounted for 71% of the entire increase in S&P 500 earnings growth during the latest week of earnings season. Alphabet surprised the market with EPS growth more than 90% above expectations, while Meta and Amazon beat consensus estimates by 56% and 70%, respectively.

Projected earnings growth for the Magnificent 7 has now climbed to 61%, compared with expectations of 22.4% at the end of March, highlighting the scale of megacap dominance in the current cycle. However, it is worth noting that the results from Alphabet, Amazon, and Meta were also supported by one-off accounting gains.

Source: FactSet

Daily Summary: Wall Street Regains Ground; Another Intervention in the Yen Market❓

Three Markets to Watch Next Week (July 31, 2026)

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Euro Area core inflation above estiamtes! EURUSD under key resistance!