Oracle (ORCL.US), a cloud services giant, is a company that has built its position over decades primarily on databases and enterprise software, and today is increasingly focusing on the development of cloud computing and artificial intelligence. On one hand, Oracle still derives a significant portion of its revenue from traditional database systems and business applications, while on the other hand, the role of Oracle Cloud Infrastructure and SaaS services is growing. The company has become one of the beneficiaries of the AI boom, partly due to high-profile contracts with OpenAI and other partners. Today's financial results, published after the market closes, will not only be a quarterly report but also a test of how the market evaluates Oracle's strategy in the world of cloud and AI.

Source: Xstation

In the short term, the company is in a very strong upward trend – the stock price has gained over 90% from local lows in April, and several investment banks are raising their price forecasts, reaching even 300–325 USD. This is due to expectations of further revenue growth from the cloud, an increasing order backlog, and increased demand for infrastructure for AI models.

At the same time, more cautious voices are emerging – for example, RBC Capital believes that the valuation is already too high, pointing to a possible slowdown in OCI growth. In the long term, key questions concern not only further AI contracts, but also whether the company will be able to maintain margins with increasing capital expenditures on data centres and equipment.

In recent weeks, there has also been talk of large layoffs at Oracle – over 3,000 people, mainly in marketing and customer service departments, which is part of a broader wave of restructuring in the tech industry. On the other hand, the market is buzzing with reports of potential multi-billion dollar contracts with OpenAI, which would be effective from 2028 and significantly increase long-term cloud revenue. These conflicting signals mean that today's results will be analysed particularly closely.

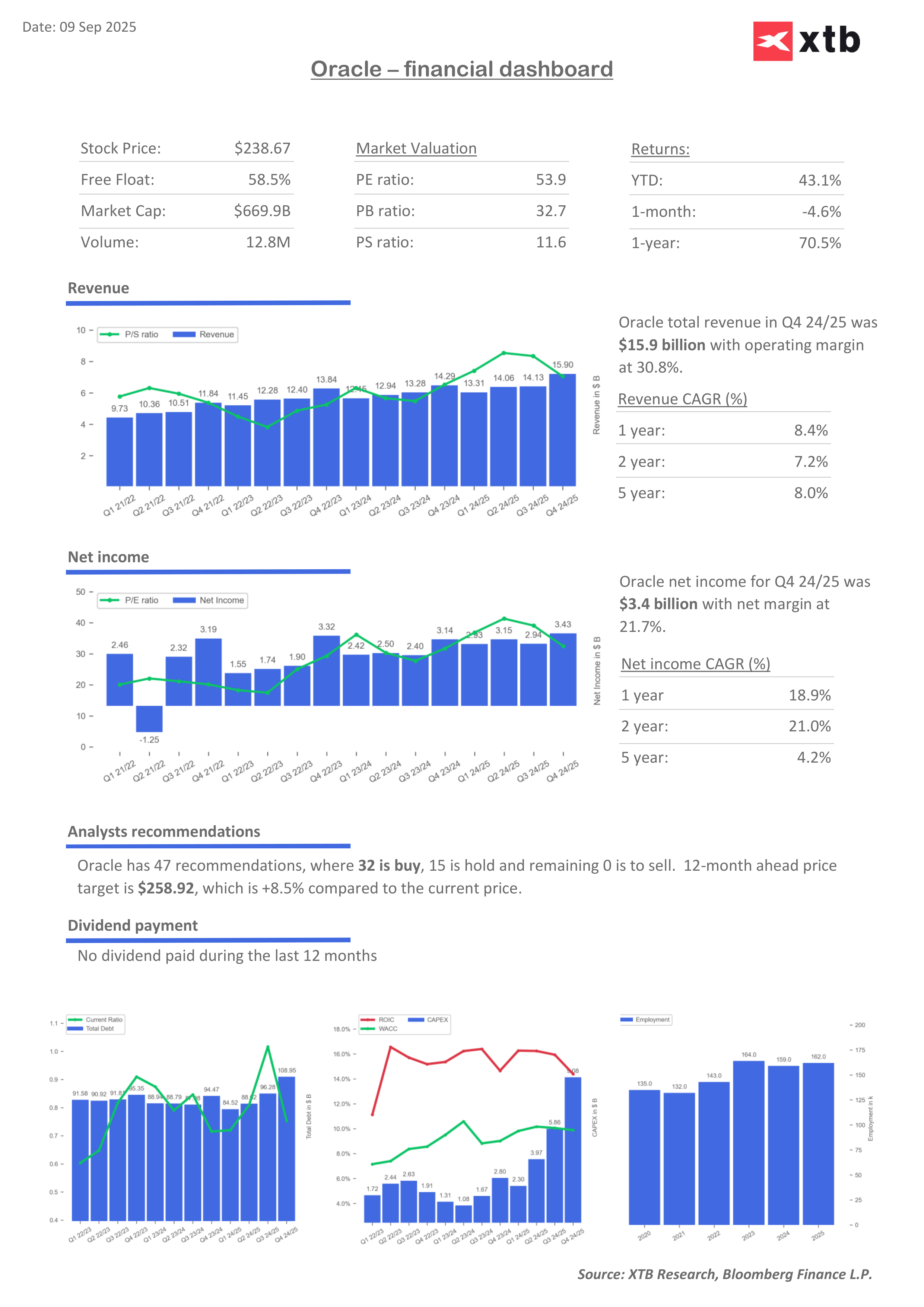

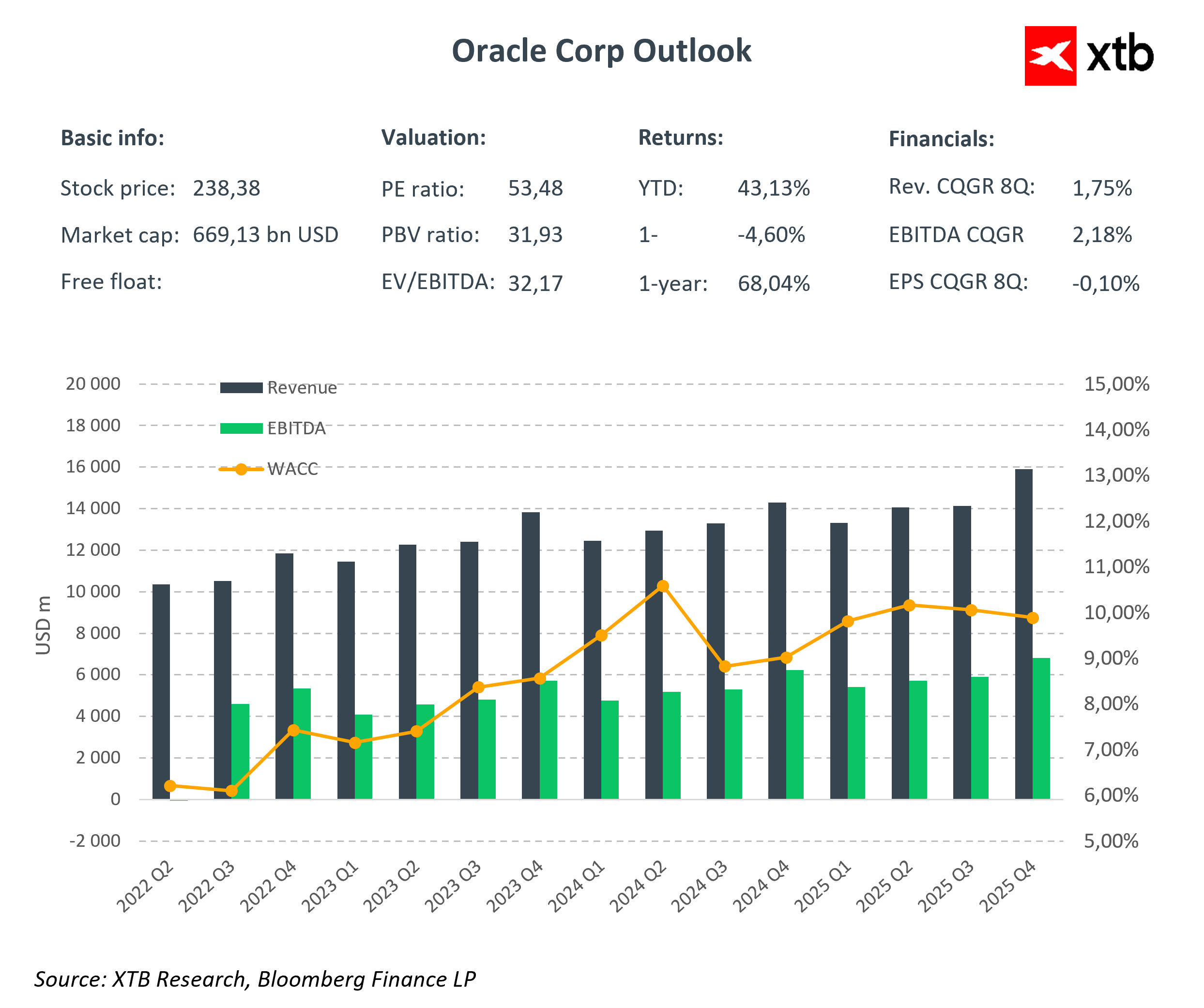

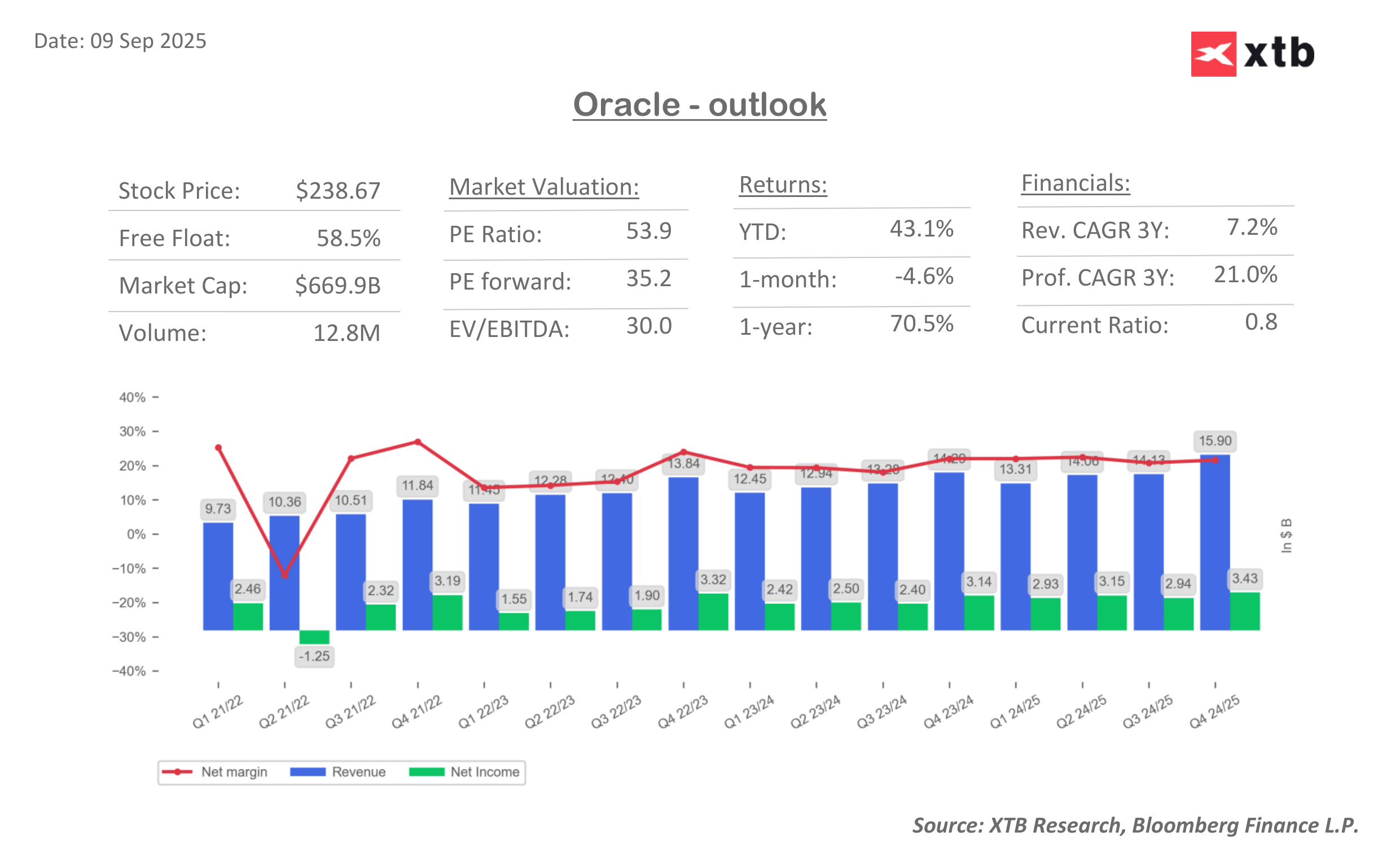

As can be seen in the revenue and valuation metrics charts, the company's growth is stable, and very high metrics are gradually normalizing.

The market's base scenario currently is that the company will exceed forecasts both in terms of EPS and revenue, show strong growth in OCI, and provide clear signals regarding the execution of the agreement with OpenAI and other partnerships. In such a case, the shares could continue their dynamic rally.

However, if the company disappoints, for example, with lower-than-expected cloud revenue, more cautious comments regarding margins and CAPEX, and a lack of specifics about large AI contracts, such a report could become a pretext for profit-taking and a correction in the stock price after such large increases in recent months.

It is worth noting that the expected results for the first quarter of the new fiscal year Q1 FY26 – which is effectively the second calendar quarter – will be weaker than those reported for the previous period, Q4 FY25. At that time, Oracle showed revenue of 15.9 billion USD and EPS of 1.70 USD, higher than current consensus estimates of around 15.0 billion USD and 1.48 EPS. However, such weakness does not necessarily mean problems right away – Q4 traditionally tends to be a stronger sales period for the company. Nevertheless, the market will be watching whether the decline is merely a seasonal effect or a signal that the growth rate of cloud and AI services is beginning to stabilize. If it turns out that the lower numbers are a temporary effect, investors may ignore the difference compared to Q4.

However, if the company does not present strong prospects for the coming quarters, there will be concern that the stock valuation – already very high – does not have sufficient foundation in real revenues. In extreme cases, this could lead to a larger correction in the sector.

Morning Wrap: AI companies and gold back in favour? (22.07.2026)

Did SaaS lost too much? Morgan Stanley says yes.

Tech sector catches its breath 🚀

US OPEN: Semiconductors drive a rebound