- Company delivered acceptable earnings

- Worse guidance has sunk the stock's price

- Texas Instrument benefits from Chip's act but suffers on tariffs

- Trade tensions might benefit company in the long term

- Despite tense financial situation, company returns cash back to investors

- Company delivered acceptable earnings

- Worse guidance has sunk the stock's price

- Texas Instrument benefits from Chip's act but suffers on tariffs

- Trade tensions might benefit company in the long term

- Despite tense financial situation, company returns cash back to investors

Texas Instruments is an icon of analog semiconductors. It designs and manufactures power, signal, and microcontroller systems that are used in automotive, industrial, consumer electronics, and medical equipment. The company is also building its own manufacturing chain on 300-millimeter wafers in the United States, which aims to make it independent from external suppliers and strengthen control over costs.

At first glance, the third-quarter report published by the company today looks decent.

- Revenues reached $4.74 billion, exceeding consensus

- Sales increased by 7% quarter-on-quarter and by as much as 14% year-on-year.

- Earnings per share amounted to $1.48, which was one cent lower than market expectations.

Despite this, shares are falling by about 8% before the market opens. The reason is clear and was immediately apparent after the publication. The company provided a weaker forecast for the fourth quarter, which was significantly below the previous consensus, and the market interpreted this as a signal of slower recovery in the entire analog sector.

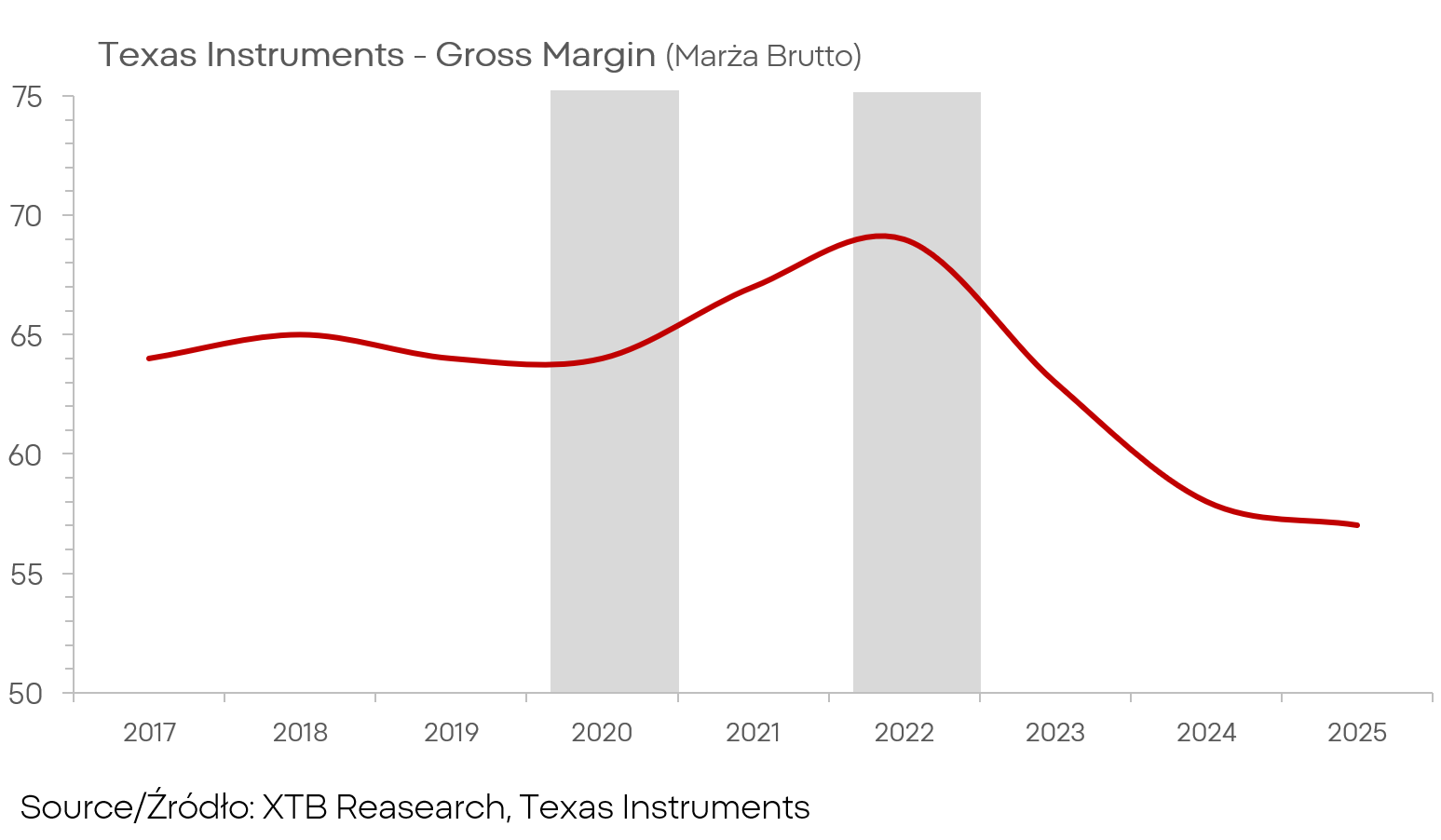

However, the list of problems does not end there. The company operates under increasing pressure from tariffs and uncertainty regarding new duties, and it also faces tougher competition from manufacturers in China. The expansion of capacity in older-generation semiconductors there is causing price pressure, and the cyclical rebound in demand in automotive and industry is slower than many expected. As a result, the market fears that orders in the coming months may not meet expectations. Additionally, total debt amounts to about fourteen billion dollars, and margins, although recently rebounding, remain lower than in 2022.

This is due to higher costs, weaker capacity utilization, and price pressure. Such a combination naturally worsens the perception of the company in the eyes of the market in an environment of heightened uncertainty.

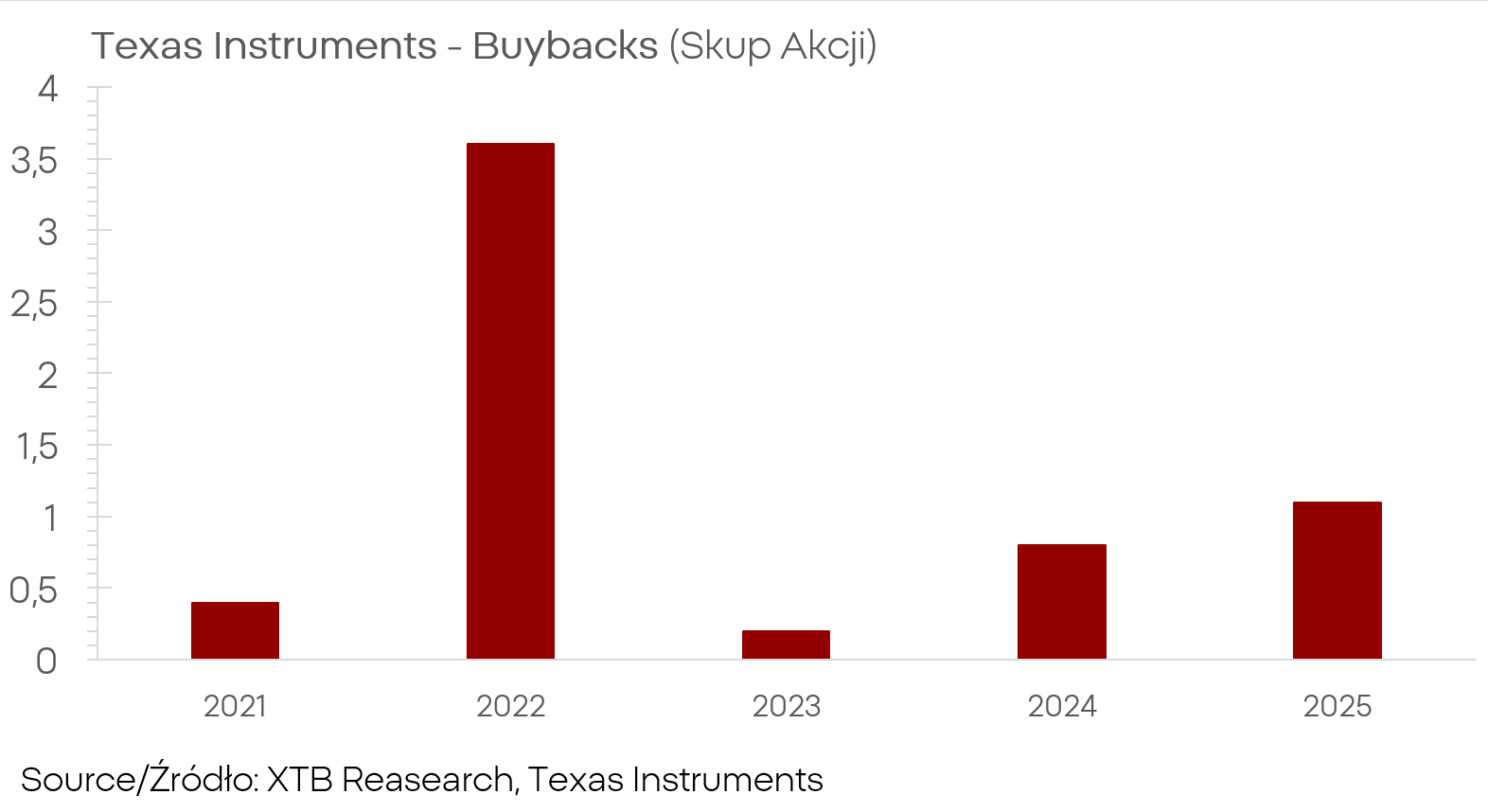

Two numbers stand out in the report. Free cash flow over twelve months increased by sixty-five percent, and spending on share buybacks went up by about two hundred fifty-three percent. However, it should be noted that in the case of share buybacks, this is mainly due to a low base and still far from the levels of 2022. In the case of free cash flow, the picture is better because lower CAPEX clearly contributes to improvement. Thanks to subsidies from the CHIPS Act program, the company was able to maintain the pace of investments at a significantly lower cash cost. Additionally, the company benefited from better inventory and receivables management, which lowered the inventory cycle ratio.

Not everything is lost, though.

The management continues the restructuring and optimization program and expands domestic production capacities, all while maintaining a generous dividend and share purchase policy. In the long term, current trade tensions may paradoxically become an advantage if American customers start preferring local suppliers, and investments from recent years begin to reflect in the results in the form of higher productivity and free cash flow.

This scenario is not guaranteed but remains a real option that investors should consider.

The situation of Texas Instruments is complex and does not inspire optimism for the next quarter, but the company is taking actions to address key weaknesses.

If transparency in tariff policy improves and competition stabilizes in mature markets, and ongoing investments start to increase efficiency, then over the next few years, the current weakness may prove to be a transitional period that builds the foundation for more solid growth.

For now, however, the market rightly discounts weaker indications for the fourth quarter and greater environmental uncertainty.

TXN.US (D1)

Source: xStation5

Daily Summary: Wall Street Regains Ground; Another Intervention in the Yen Market❓

Three Markets to Watch Next Week (July 31, 2026)

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Euro Area core inflation above estiamtes! EURUSD under key resistance!