- Headline CPI: +0.3% m/m, +2.7% y/y (unchanged vs. November)

- Core CPI (ex food & energy): +0.3% m/m, +2.7% y/y (up from 2.6% in November)

- The December report may therefore give the impression of a return of price pressures due to distortions in the November data.

- Headline CPI: +0.3% m/m, +2.7% y/y (unchanged vs. November)

- Core CPI (ex food & energy): +0.3% m/m, +2.7% y/y (up from 2.6% in November)

- The December report may therefore give the impression of a return of price pressures due to distortions in the November data.

Today at 01:30 PM GMT we will receive the December US CPI print. This is the most important report of the week and, alongside NFP, one of the key releases from the Federal Reserve’s monetary policy perspective.

Inflation in the US likely edged slightly higher at the end of 2025. Consensus expects December CPI to come in at +0.3% m/m for both headline and core inflation. On a year-on-year basis, headline CPI is seen at 2.7%, while core CPI is expected to rebound to 2.7% from 2.6% in November. This modest uptick is mainly attributed to normalization after an unusually weak November reading, rather than the start of a new wave of inflationary pressure.

November CPI was distorted by the US government shutdown, which delayed price data collection and forced the Bureau of Labor Statistics (BLS) to rely on imputations—particularly in shelter components. According to Bloomberg Economics, this may have understated inflation by around 20 bps. As a result, the December report may appear to signal a return of price pressures as these one-off effects unwind. Some banks also point to the possibility of lingering distortions, suggesting that the first truly “clean” data may not arrive until February.

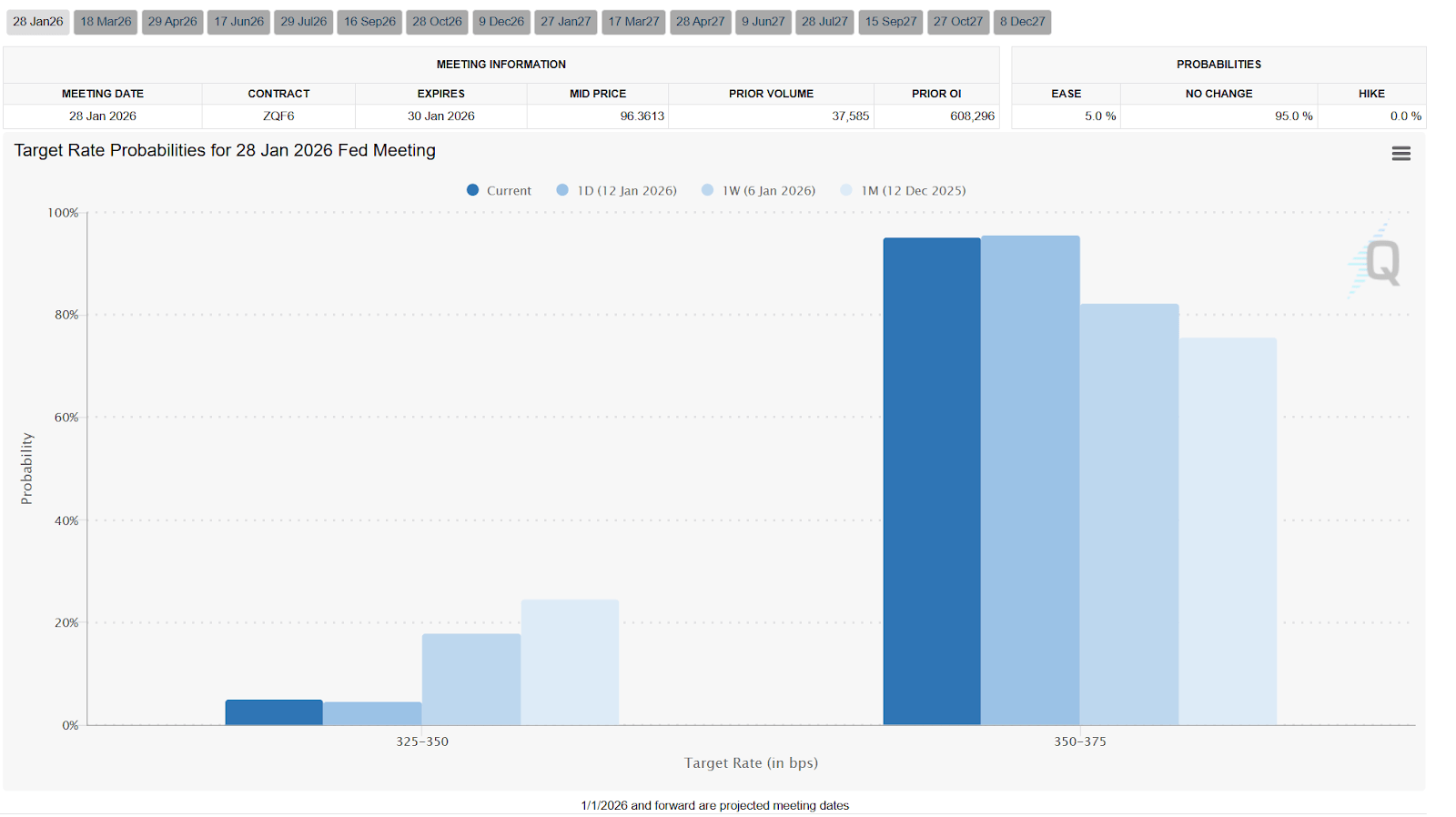

Markets price roughly a 95% probability that the Fed will keep interest rates unchanged at the upcoming meeting. Policymakers will monitor the impact of tariffs on prices, but most forecasts assume that inflation will gradually cool in 2026. Disinflation in housing and softer wage pressures are expected to outweigh tariff effects.

Interestingly, market pricing for the January decision has become increasingly hawkish day by day. This shift may help explain the recent rebound in the US dollar. Source: CME FedWatch Tool.

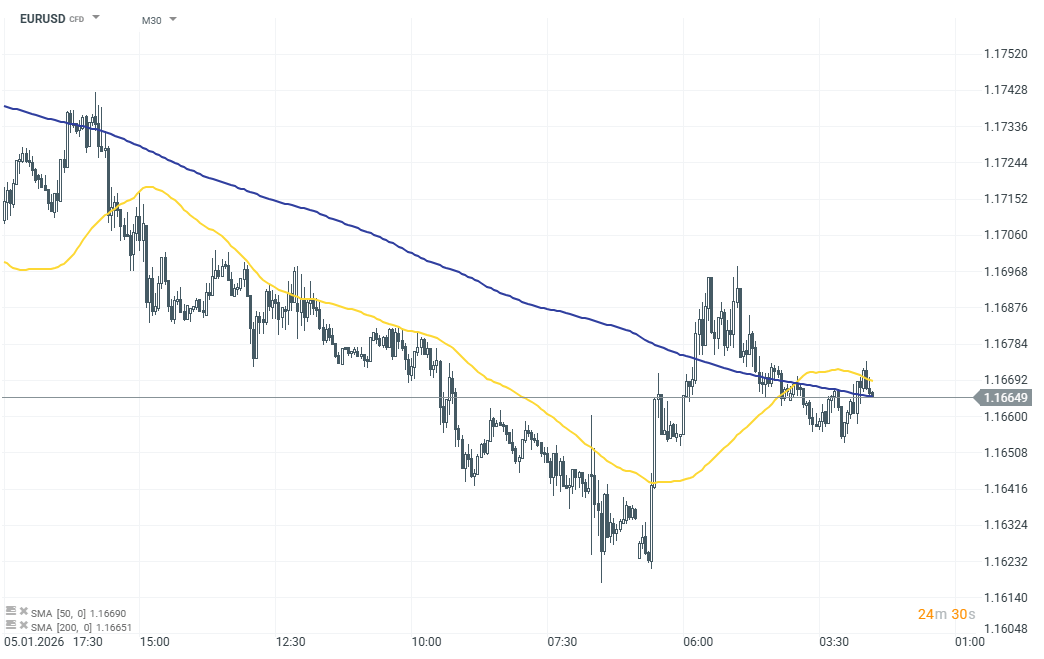

EURUSD (D1 timeframe)

The dollar remains relatively calm ahead of the release. EURUSD is trading slightly lower, down 0.02%. The pair is also influenced by heightened geopolitical uncertainty and ongoing developments around the US central bank, which may temper the market reaction to the CPI report.

Daily summary: Sense of relief to global markets🎢 OIL prices dip 8%🚨

BREAKING: US ISM Manufacturing - Strong Beat Across the Board

Eurozone PMIs: German Factory Revival Masks Underlying Stagnation 🇪🇺

Chart of the Day: Yen Falls From 40-Year Highs – What’s Next? (03.08.2026)