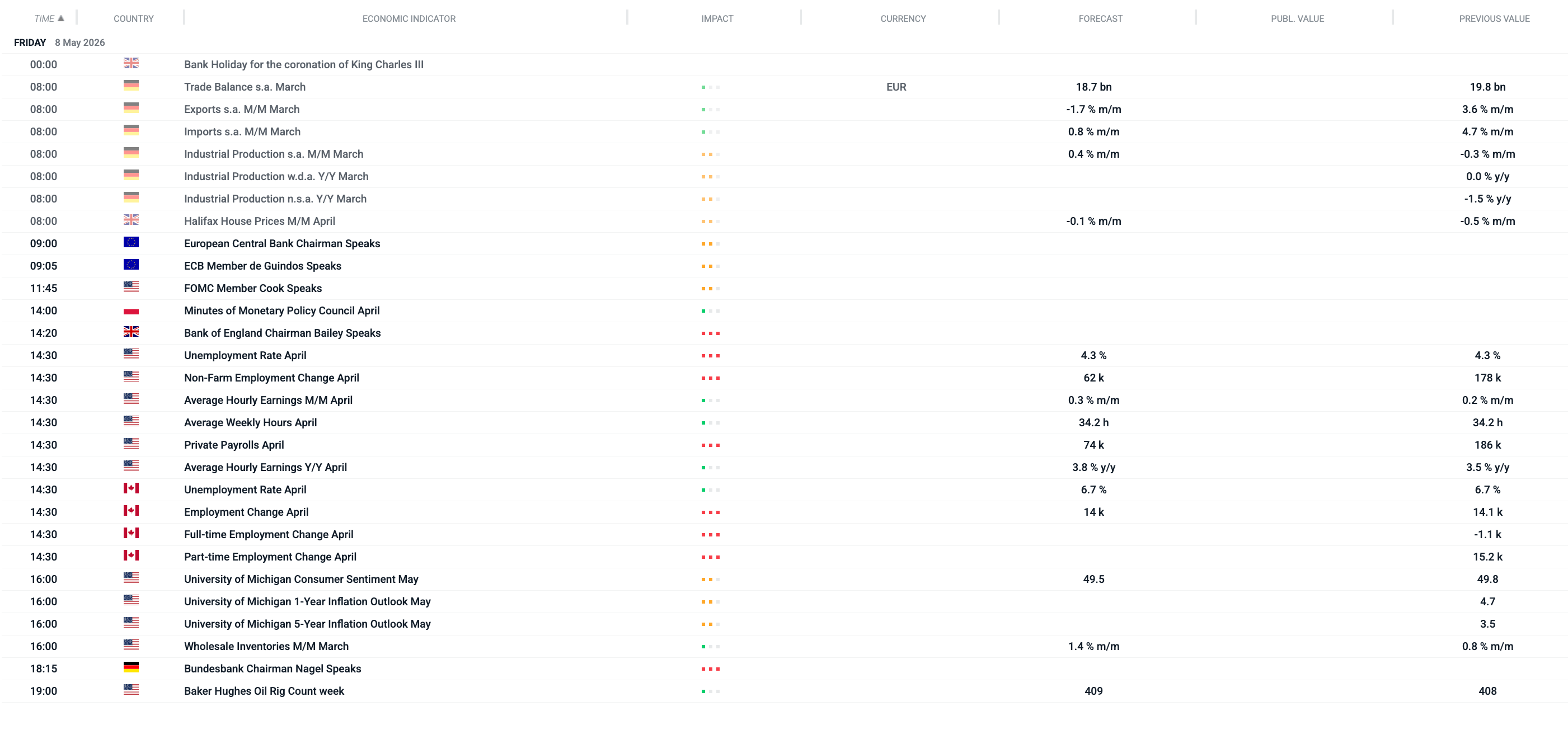

Today’s session will remain reigned by the sentiment around the Middle East conflict, though market volatility should also spike amid high-stake data releases, key for the monetary policy in the US.

Market focus will center on the Non-Farm Payrolls (NFP), which are expected to show cooling labor market with a modest 62k gain against a steady 4.3% unemployment rate. This anticipated slowdown in hiring is the primary driver for sentiment, as investors weigh whether the US economy is heading for a soft landing or a sharper contraction amidst restrictive policy, as well as the continuation of a lower labour market turnover.

Complementing this is the University of Michigan (UoM) report, forecast to show subdued consumer sentiment at 49.5 alongside persistent 4.7% inflation expectations. Navigating these critical releases is a rally of central bank speakers, including the BoE’s Bailey, ECB officials, and the FOMC’s Cook. Their coordinated commentary will be pivotal as they attempt to reconcile softening growth data with the need to keep long-term inflation expectations anchored.

All times CET. Filtered by: US, Canada, UK, Eurozone, Germany, France, Poland, Japan, Australia, New Zealand. Source: xStation5

Economic Calendar: What Could Move the Market This Week? (03.08.2026)

Morning Wrap: USA Halts Strikes – Oil Down, Stocks Up (03.08.2026)

Daily Summary: Wall Street Regains Ground; Another Intervention in the Yen Market❓

Three Markets to Watch Next Week (July 31, 2026)