🏛️ At 7:00 PM (BST), we’ll learn the details of the Fed’s latest decision

The Federal Reserve’s latest decision to keep interest rates unchanged (at 4.25%–4.50% since December) aligned with investor expectations. However, the Fed’s internal narrative has been evolving quickly in light of incoming macroeconomic data.

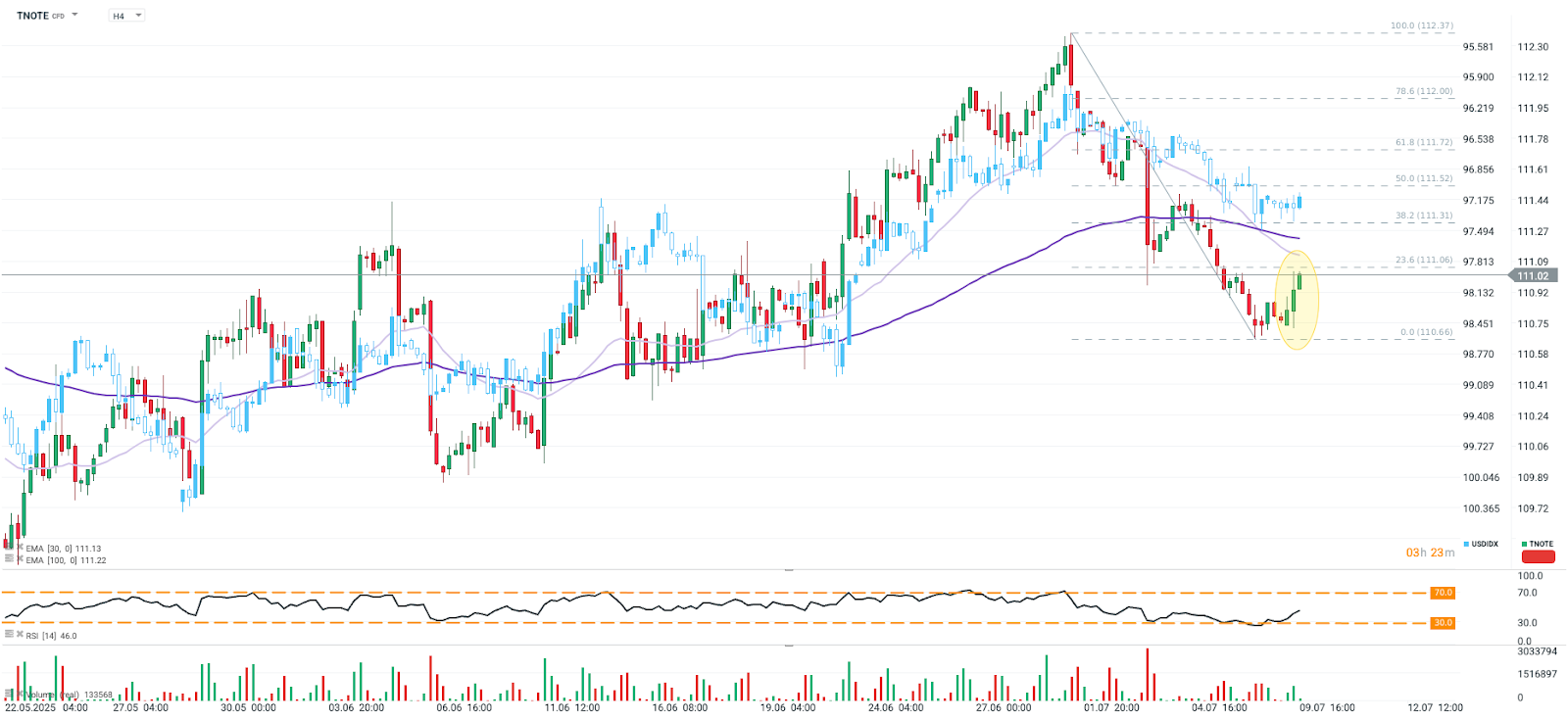

The June FOMC meeting took place before the release of a very strong NFP report, which cooled expectations for potential rate cuts. The labor market turned out stronger than forecast (more new jobs than the consensus expected), justifying the Fed’s cautious and patient stance. As a result, the decline in U.S. 10-year yields was halted.

เริ่มเทรดทันทีวันนี้ หรือ ลองใช้บัญชีทดลองแบบไร้ความเสี่ยง

เปิดบัญชี ลองบัญชีเดโม่ ดาวน์โหลดแอปมือถือ ดาวน์โหลดแอปมือถือ

What to expect from the FOMC minutes:

-

Internal Fed divide: Christopher Waller and Michelle Bowman (Trump appointees) support a July rate cut; meanwhile, 7 members foresee no cuts at all in 2025, while 17 expect one or two.

-

Market expectations vs. Fed reality: Markets still price in two cuts by the end of 2025, even though some FOMC members see no room for easing. This would mark the fourth consecutive year where markets assume a more dovish trajectory than what actually materializes.

-

Rate cut timing: While a July cut remains highly unlikely, the Fed may be laying the groundwork for a possible September move—contingent on clearer tariff impacts and stable macro data.

-

Inflation vs. tariffs: The debate likely addressed whether tariff-driven price increases will be temporary or more lasting. The Fed’s latest projections show higher PCE inflation extending into 2027. This may limit room for swift rate cuts—especially if inflation proves stickier than expected and market expectations need to adjust.

-

Labor market: The absence of clearly negative data should reinforce the Fed’s "wait-and-see" stance—particularly if job growth remains solid and unemployment stays stable. Continued labor market strength could delay rate cuts, despite tariff-driven inflation pressures.

-

Fiscal policy and debt impact: Market participants are also watching rising borrowing costs and U.S. debt auctions. Weak demand for Treasuries (as seen in Tuesday’s 3-year auction) may raise concerns over the sustainability of U.S. debt levels, potentially influencing monetary policy.

Source: xStation5