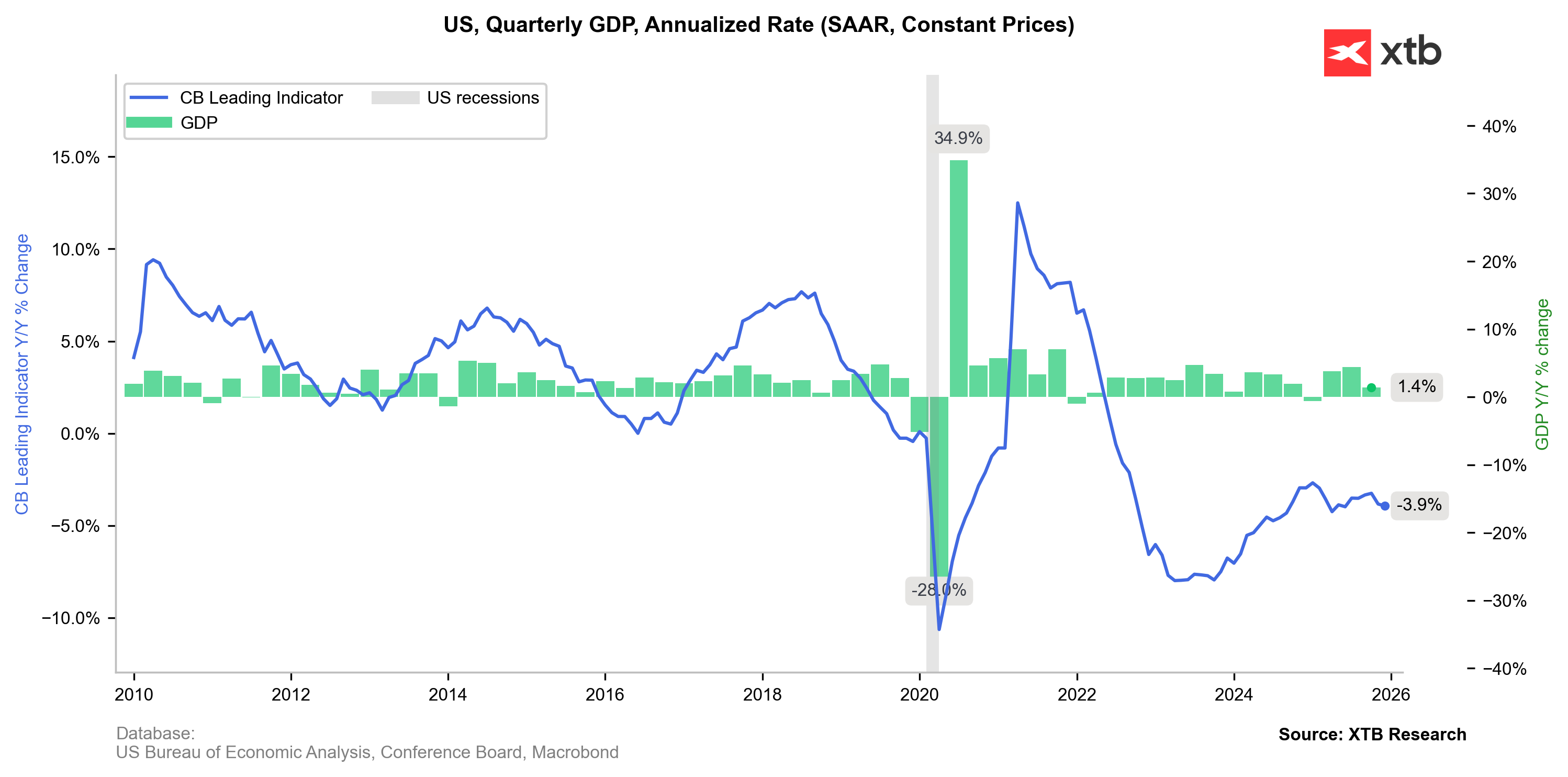

การเติบโตทางเศรษฐกิจของสหรัฐฯ ชะลอตัวลงอย่างมากในไตรมาส 4 ปี 2025 โดยร่วงจากระดับ 4.4% ที่ขับเคลื่อนด้วยการบริโภคและมุมมองเชิงบวกสูง เหลือเพียง 1.4% เท่านั้น

ในภาพแรก ตัวเลขที่ต่ำกว่าคาดการณ์ถึงครึ่งหนึ่ง ประกอบกับสัญญาณเงินเฟ้อที่กลับมาสูงเกินคาดเป็นครั้งแรกในรอบหลายเดือน อาจทำให้หลายคนกังวลว่าเศรษฐกิจกำลังเข้าสู่ภาวะ “stagflation”

อย่างไรก็ตาม เมื่อพิจารณารายละเอียดในรายงานของ Bureau of Economic Analysis จะเห็นภาพที่แตกต่างออกไป โดยข้อมูลสะท้อนถึงรากฐานที่ยังแข็งแกร่งพอสำหรับการฟื้นตัวของเงินเฟ้อ และในขณะเดียวกันก็เปรียบเสมือนใบรายงานผลที่ย่ำแย่อย่างมากสำหรับนโยบายของทำเนียบขาว

Source: XTB Research

Record Shutdown, Record Decline

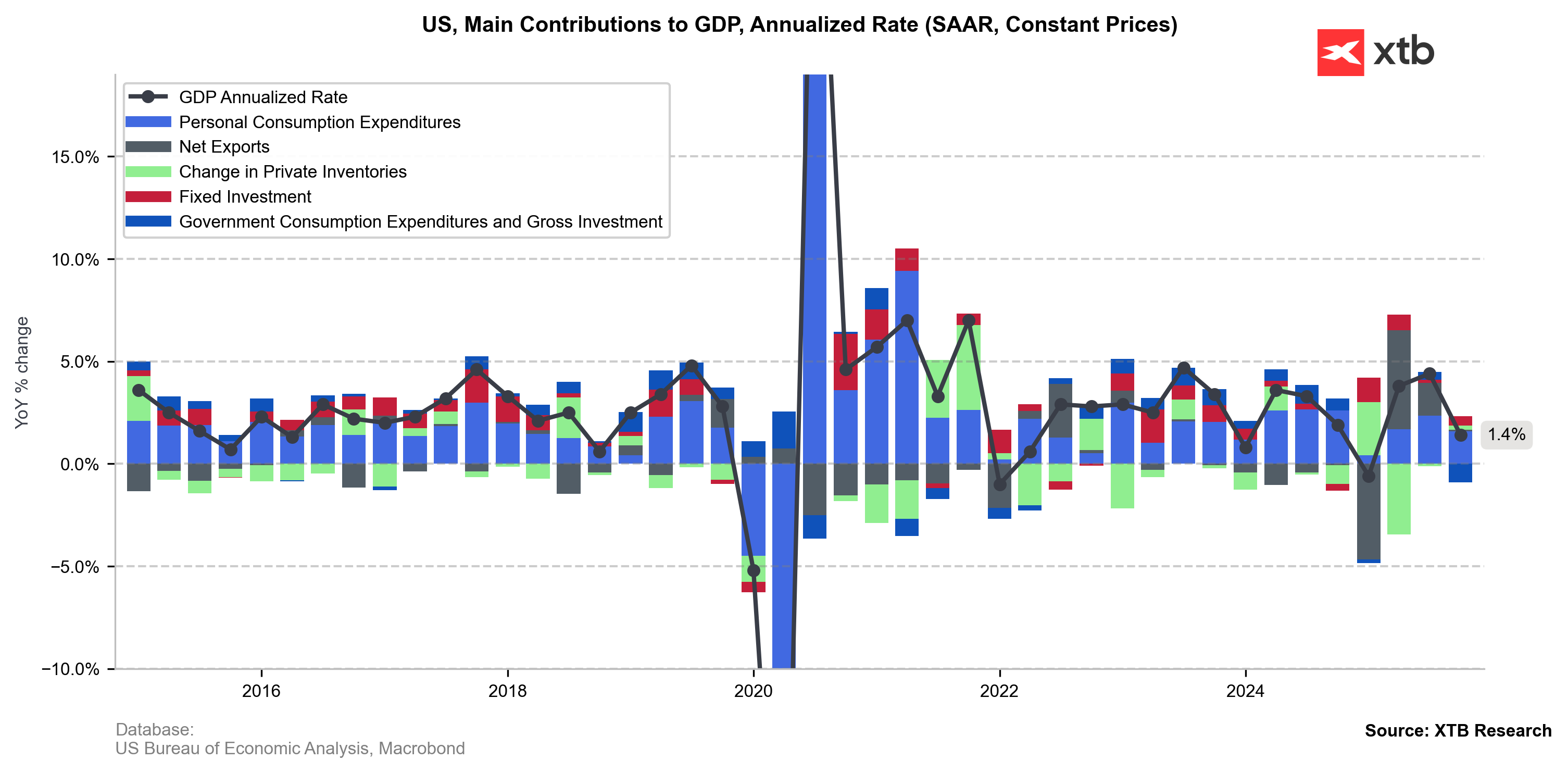

The sharp drop in GDP growth was primarily dictated by the longest government shutdown in history last fall, which suspended federal agency operations and all associated spending—including salaries, social programs, and security. Federal-level spending fell by 1.15%, the worst performance since the 1970s.

Additionally, net exports—the primary engine of GDP data in recent quarters—essentially stalled, calling into question the effectiveness of Donald Trump’s protectionist policies. In fact, exports fell by 0.1% in Q4, driven by a drop in goods; the trade balance was saved only by a slowdown in imports (from 0.6% to 0.2%) rather than an outright decline.

Nevertheless, the report reflects political tribulations rather than structural weakness. The consumer remains the primary driver of the US economy, with spending rising by nearly 1.6% despite inflation lingering above target and a tight labor market. Furthermore, investment growth accelerated, with the most significant capital flow directed toward data processing infrastructure. This suggests ongoing AI adoption, which both the current and nominated Fed chairs expect will increase long-term productivity and limit inflation.

The drop in the US GDP growth was driven by shutdown-driven swings in public sector, not the stagnation in the private economy. Source: XTB Research

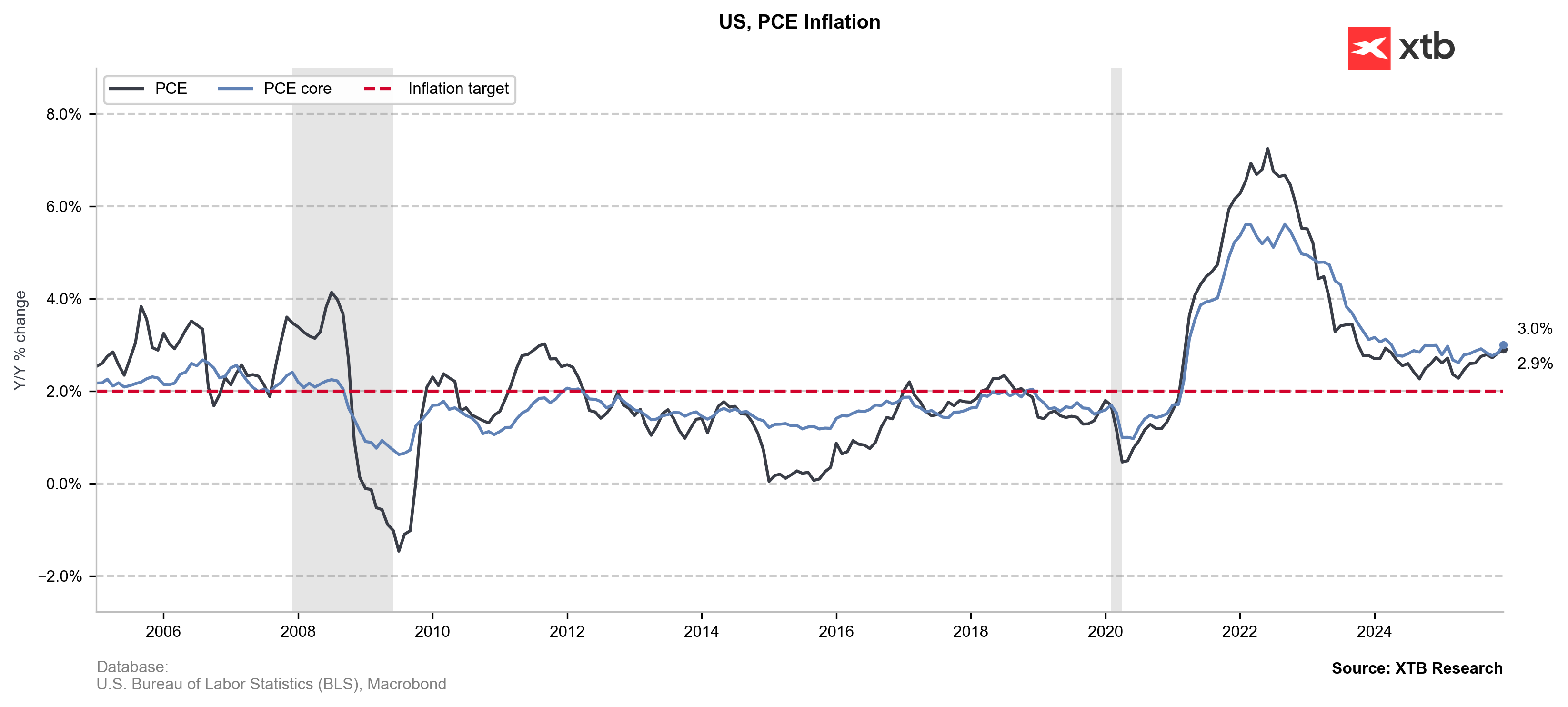

วอลล์สตรีทกลับมากังวลเงินเฟ้ออีกครั้ง

บรรยากาศเชิงลบของข้อมูลเศรษฐกิจในวันนี้ยิ่งทวีความชัดเจน หลังจากตัวเลขเงินเฟ้อที่ Federal Reserve ให้ความสำคัญเป็นพิเศษออกมาสูงกว่าคาด

ดัชนี Core PCE ซึ่งเป็นมาตรวัดเงินเฟ้อที่ครอบคลุมตะกร้าสินค้าและบริการกว้างกว่า CPI และยังรวมค่าใช้จ่ายที่มีการจ่ายแทนผู้บริโภค (เช่น เงินอุดหนุนประกันสุขภาพ) ปรับเพิ่มขึ้นจาก 2.8% สู่ 3% สูงกว่าที่ตลาดคาดการณ์ไว้

ตัวเลขดังกล่าวทำให้นักลงทุนใน Wall Street กลับมาให้ความสำคัญกับความเสี่ยงด้านเงินเฟ้ออีกครั้ง และเพิ่มแรงกดดันต่อแนวโน้มนโยบายการเงินในระยะต่อไป

The increase in PCE inflation has been gradual. Source: XTB Research

The rise in PCE inflation to 3% should not be surprising given the steady upward trend visible in the data. Wall Street, however, has largely ignored readings that were in line with or lower than expectations for some time, even as they signaled building price pressure. The market has slightly dialed back its pricing for US rate cuts, still betting on July as the next window. Nonetheless, we can expect a sharpening of hawkish rhetoric from the Fed, especially following FOMC Minutes indicating that cutting rates with PCE at 3% would suggest a lack of determination in the fight against inflation.

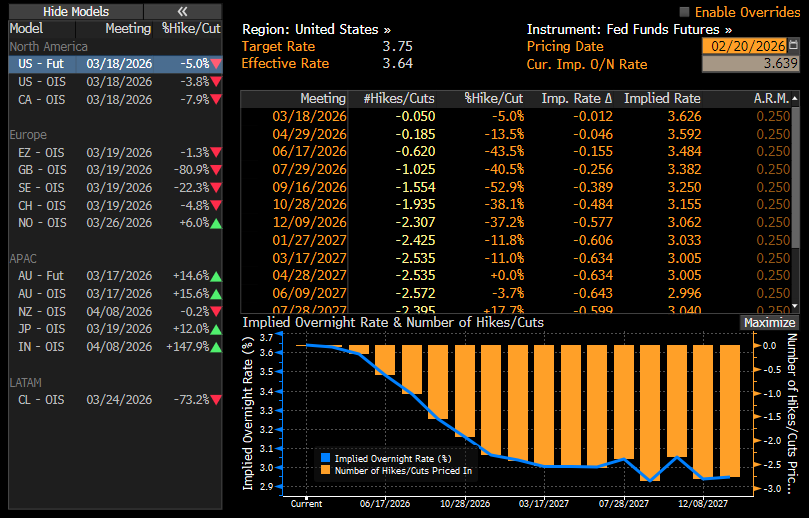

The implied rate cut probabilities remain vastly the same, with first cut expected in July. Source: Bloomberg Finance LP

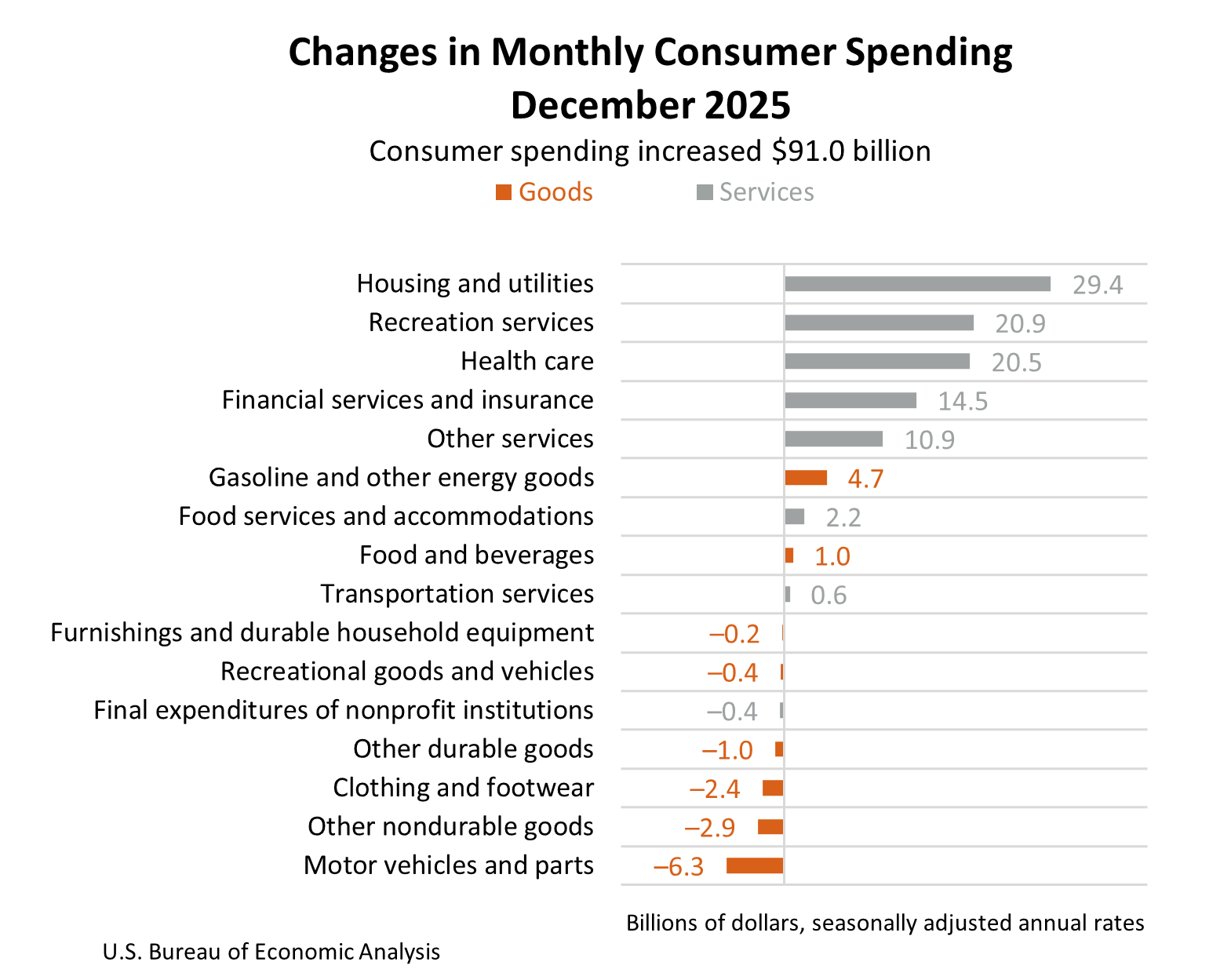

The Danger of "Sticky" Spending

The "sticky" nature of US inflation is also evident in the structure of the PCE report. The largest increases were recorded in "non-discretionary" sectors—healthcare, housing, utilities, and insurance—which are harder to control via higher interest rates. Conversely, the visible drop in spending on goods suggests that consumers are being "squeezed" by the rising cost of living, leading them to forgo discretionary purchases.

Source: BEA

บทสรุป: เศรษฐกิจกำลังเดินหน้าได้ “แม้ไม่มีทรัมป์” จริงหรือไม่?

เมื่อพิจารณาข้อมูลทั้งหมด ภาคเอกชนและผู้บริโภคของสหรัฐฯ ยังคงแสดงให้เห็นถึงความแข็งแกร่ง แม้ต้องเผชิญกับความวุ่นวายทางการเมืองและการโยนความรับผิดชอบกันไปมารอบประเด็นการปิดหน่วยงานรัฐบาล

ยิ่งไปกว่านั้น การชะงักงันของการส่งออกสุทธิยังเปิดเผยความจริงที่ถูกซ่อนไว้ภายใต้นโยบายกีดกันทางการค้าของทำเนียบขาว นั่นคือ ห่วงโซ่อุปทานและกำลังการผลิตระดับโลกไม่สามารถย้ายกลับมายังสหรัฐฯ ได้ในชั่วข้ามคืน

หลังจากความผันผวนที่เกิดจากการเร่งกักตุนสินค้าคงคลังก่อนมาตรการภาษีนำเข้า โครงสร้างการค้าควรค่อย ๆ กลับสู่ภาวะปกติ อย่างไรก็ตาม การที่มูลค่าการนำเข้ายังคงเติบโตอย่างสม่ำเสมอ สะท้อนว่า ชาวอเมริกันยังคงซื้อสินค้าเดิม ๆ เพียงแต่ต้องจ่ายในราคาที่สูงขึ้นเท่านั้น

Aleksander Jablonski

นักวิเคราะห์เชิงปริมาณ (Quant Analyst)

🛢️ น้ำมันดิบ Brent ทดสอบระดับ $95 ต่อบาร์เรล

Economic Calendar: จับตาผลประกอบการ Tesla และ Google

Morning Wrap: หุ้น AI และทองคำกลับมาได้รับความสนใจอีกครั้ง?

ข่าวเด่นวันนี้ 22 ก.ค.