รัสเซียเป็นหนึ่งในสมาชิกสำคัญของกลุ่มผู้ผลิตน้ำมันรายใหญ่แบบ “exclusive” และอุตสาหกรรมไฮโดรคาร์บอนถือเป็นปัจจัยหลักที่กำหนดทิศทางนโยบายของสหพันธรัฐรัสเซียมาโดยตลอด สงครามในยูเครนได้แสดงให้เห็นอย่างชัดเจนว่า “แหล่งอำนาจที่แท้จริงของรัสเซีย” ไม่ได้อยู่ที่กองทัพ แต่คือทรัพยากรน้ำมันและก๊าซธรรมชาติจากไซบีเรีย โรงกลั่น และโครงข่ายท่อส่งพลังงาน

จุดอ่อนสำคัญของเศรษฐกิจรัสเซียนี้กำลังถูกโจมตีโดยกองทัพยูเครน โดยการโจมตีโครงสร้างพื้นฐานด้านพลังงานของรัสเซียกำลังยกระดับขึ้นอย่างมีนัยสำคัญ โดยเฉพาะในช่วงที่สถานการณ์ตะวันออกกลางและอ่าวเปอร์เซียส่งผลให้ราคาน้ำมันโลกผันผวนอย่างรุนแรง คำถามสำคัญคือ โดรนของยูเครนจะ “เร็วกว่า” รายได้ที่ไหลเข้าสู่คลังของเครมลินหรือไม่

การเข้าใจน้ำมัน = การเข้าใจรัสเซีย

เช่นเดียวกับโครงสร้างรัฐรัสเซียเอง อุตสาหกรรมน้ำมันและก๊าซของประเทศนี้ถูกผูกติดกับอดีตอย่างลึกซึ้ง อุตสาหกรรมน้ำมันของสหภาพโซเวียตมีจุดกำเนิดในบากู (ปัจจุบันอยู่ในอาเซอร์ไบจาน) การผลิตอย่างเข้มข้นในอดีตทำให้คุณภาพของแหล่งน้ำมันเสื่อมลง และระบบอุตสาหกรรมโซเวียตไม่สามารถแก้ปัญหานี้ได้อย่างมีประสิทธิภาพ

ต่อมา “ศูนย์กลางการผลิตน้ำมัน” ได้ย้ายไปยังไซบีเรียตะวันตก และยังคงเป็นหัวใจของการผลิตจนถึงปัจจุบัน ซึ่งมีความสำคัญอย่างมาก เพราะระยะยิงของโดรนยูเครนถูกออกแบบให้สามารถเข้าถึงพื้นที่ดังกล่าวได้

แหล่งน้ำมันในไซบีเรียตะวันตกมีขนาดใหญ่ แต่การสกัดเชิงพาณิชย์กลับทำได้ยาก น้ำมันของรัสเซียมีลักษณะ “หนัก” และมีสิ่งเจือปนสูง (sour crude) ซึ่งทำให้การสกัดและการกลั่นมีต้นทุนสูงและซับซ้อนมากขึ้น

การขาดเทคโนโลยีที่ทันสมัยและการบริหารจัดการที่ไม่มีประสิทธิภาพตั้งแต่ยุคโซเวียต ส่งผลให้แหล่งผลิตเสื่อมคุณภาพลงเรื่อย ๆ และทำให้เศรษฐกิจโซเวียต—และต่อมาคือรัสเซีย—ต้องพึ่งพาทรัพยากรที่ยากขึ้นในการทำกำไรอย่างยั่งยืน

จุดสูงสุดของการผลิตน้ำมันในรัสเซียเกิดขึ้นในช่วงทศวรรษ 1970 โดยอยู่ที่มากกว่า 13 ล้านบาร์เรลต่อวันเล็กน้อย หลังการล่มสลายของสหภาพโซเวียต การผลิตลดลงเหลือประมาณ 6 ล้านบาร์เรลต่อวัน และในปัจจุบันตัวเลขดังกล่าวยังไม่เกินระดับ 10–11 ล้านบาร์เรลต่อวัน

การเสื่อมสภาพของแหล่งผลิตจากการใช้งานอย่างหนักในยุคสหภาพโซเวียต ทำให้สหพันธรัฐรัสเซียต้องเข้าสู่ความร่วมมืออย่างลึกซึ้งกับบริษัทตะวันตก ซึ่งนำเทคโนโลยีขั้นสูงเข้ามาและถ่ายทอดความรู้ด้านการจัดการการผลิตให้กับรัสเซีย หากไม่มีบริษัทอย่าง SLB, Halliburton, BP, Exxon, Emerson หรือ Siemens ประเทศรัสเซียที่ยากจนและล้าหลังในเชิงเทคโนโลยีคงไม่สามารถฟื้นฟูการผลิตกลับมาสู่ระดับปัจจุบันได้

สิ่งนี้สร้าง “จุดอ่อน” ที่รัสเซียไม่ต้องการยอมรับ นั่นคือโครงสร้างพื้นฐานน้ำมันของรัสเซียไม่ได้ถูกสร้างโดยชาวรัสเซียเอง แต่พึ่งพาเทคโนโลยีจากยุโรปและสหรัฐฯ หากถูกตัดขาดจากบริการ ซอฟต์แวร์ และอะไหล่ ระบบจะค่อย ๆ เสื่อมสภาพลง ซึ่งสามารถเห็นตัวอย่างได้ในเวเนซุเอลาและอิหร่าน แม้กระบวนการนั้นจะใช้เวลาไม่ใช่แค่หลายปี แต่เป็นหลายทศวรรษ

ปัญหาทางเทคนิคของอุตสาหกรรมน้ำมันรัสเซียสามารถบรรเทาได้บางส่วนผ่านความร่วมมือกับจีนและอินเดีย แต่ในเชิงโครงสร้างแล้ว อุตสาหกรรมนี้ยังคงเป็น “อุตสาหกรรมตะวันตกที่มีธงรัสเซียติดอยู่” ซึ่งไม่สามารถเข้ากันได้กับโซลูชันของเอเชีย การแก้ปัญหาอย่างแท้จริงจำเป็นต้องเปลี่ยนระบบและโครงสร้างพื้นฐานเกือบทั้งหมด

นอกจากความเสื่อมทางเทคนิคแล้ว อุตสาหกรรมน้ำมันรัสเซียยังต้องเผชิญกับการโจมตีด้วยโดรนของยูเครนเป็นระยะ ซึ่งทำลายเครื่องจักรที่มีมูลค่าสูงและยากต่อการทดแทน

คำว่า “การเสื่อมสภาพ (degradation)” จึงเป็นกุญแจสำคัญในที่นี้ เป้าหมายของยูเครนไม่ใช่การโจมตีแบบทำลายศูนย์กลางทันที แต่เป็นสงครามแบบไม่สมดุล (asymmetric campaign) ที่สร้างความเสียหายทีละเล็กทีละน้อย แต่สะสมต่อเนื่อง

แล้วความเสียหายเหล่านี้มีเป้าหมายเชิงโครงสร้างอย่างไร?

มากกว่า 30% ของการส่งออกของรัสเซียมาจากน้ำมันดิบ และพลังงานฟอสซิลหรือผลิตภัณฑ์กึ่งสำเร็จรูปมีสัดส่วนมากกว่า 50% ของทั้งหมด อย่างไรก็ตาม น้ำมันดิบไม่ใช่สินค้าที่ทำกำไรสูงสุด เพราะผลิตภัณฑ์ที่ทำกำไรดีที่สุดจากน้ำมันรัสเซียคือดีเซล ซึ่งเกิดจากคุณสมบัติด้านความหนืดและกำมะถันของน้ำมันรัสเซีย

เมื่อมองจากตัวเลขการผลิตและการส่งออก จะเห็นได้ยากว่ามาตรการคว่ำบาตรหรือสงครามมีผลทำลายล้างต่ออุตสาหกรรมอย่างรุนแรง เพราะในความเป็นจริง นั่นไม่ใช่เป้าหมายตั้งแต่แรก

รัสเซียไม่ได้ถูกตั้งเป้าให้หยุดผลิตน้ำมัน แต่ถูกตั้งเป้าให้ “ทำกำไรได้น้อยลง” ซึ่งเป้าหมายนี้ประสบความสำเร็จบางส่วนแล้ว หลังจากตลาดวัตถุดิบเริ่มทรงตัวหลังวิกฤตปี 2022

จากข้อมูลรายได้งบประมาณและปริมาณการผลิต พบว่าการสกัดและการส่งออกน้ำมันดิบแทบไม่เปลี่ยนแปลง โดยปริมาณการผลิตลดลงเพียง 2–3% และการส่งออกเพิ่มขึ้นประมาณ 3%

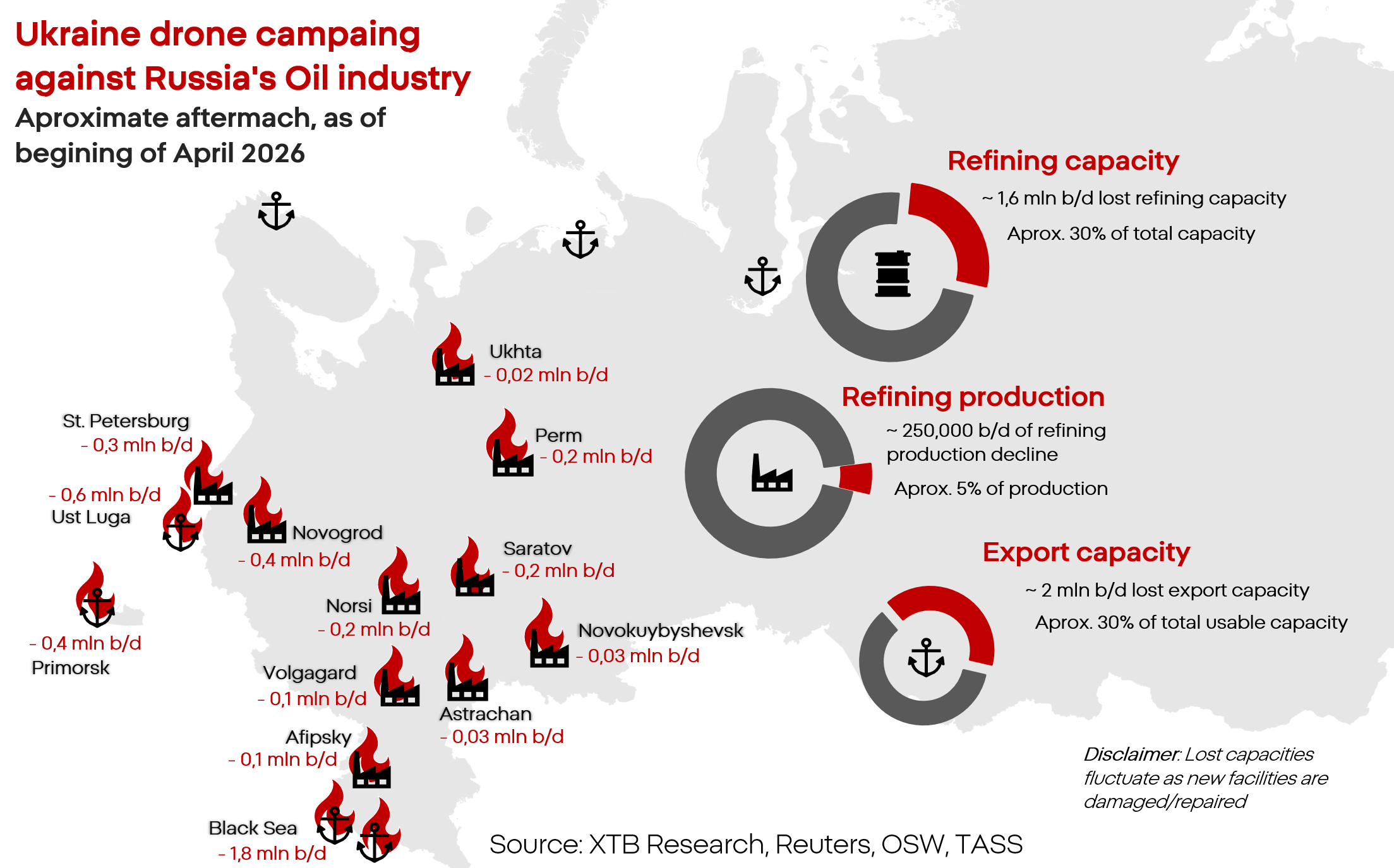

แคมเปญโจมตีด้วยโดรนของยูเครนจึงมุ่งเป้าไปยังส่วนที่ทำกำไรสูงและเปราะบางที่สุดของอุตสาหกรรม นั่นคือ “โรงกลั่นน้ำมัน” โดยทั่วไปยูเครนไม่ได้โจมตีแหล่งผลิตโดยตรง เพราะไม่คุ้มค่าในเชิงยุทธศาสตร์ แต่จะมุ่งโจมตีคอขวดของกระบวนการกลั่นและการส่งออกเชื้อเพลิง ซึ่งซ่อมแซมยากกว่า ใช้เวลานานกว่า และสร้างต้นทุนต่อเศรษฐกิจและงบประมาณรัสเซียได้มากกว่า

เนื่องจากกระบวนการกลั่นถูกปรับให้เหมาะกับน้ำมันเฉพาะชนิด รัสเซียจึงมีการผลิตดีเซลเกินความต้องการภายในประเทศอย่างมาก และต้องส่งออกเพื่อใช้กับระบบเศรษฐกิจที่สำคัญ รวมถึงยานพาหนะทางทหาร ขณะเดียวกัน การผลิตน้ำมันเบนซินซึ่งมีความสำคัญรองลงมาอยู่ในระดับ “พอดีแบบเฉียดฉิว” นี่คือจุดอ่อนที่แท้จริงที่ยูเครนกำลังโจมตี

ในขณะเดียวกัน ผลผลิตจากโรงกลั่นลดลงประมาณ 7% และการส่งออกลดลงถึง 12%

จุดสำคัญคือคำถามที่มักถูกหยิบยกขึ้นมา: หากมีรายงานว่าการโจมตีของยูเครนทำให้กำลังการกลั่นของรัสเซียเสียหายมากกว่า 30% แล้วเหตุใดผลผลิตจึงลดลงเพียง 7%?

รัสเซียมีกำลังการผลิตสำรอง (buffer) จำนวนมาก โดยกำลังการแปรรูปน้ำมันของโรงกลั่นในรัสเซียทั้งหมดประเมินได้สูงสุดราว 6 ล้านบาร์เรลต่อวัน อย่างไรก็ตาม ในปัจจุบันรัสเซียใช้กำลังการผลิตจริงเพียงประมาณ 4.5 ล้านบาร์เรลต่อวัน ดังนั้นแม้จะทำให้โครงสร้างพื้นฐานเสียหายไปถึง 1 ใน 3 รัสเซียก็ยังมีความสามารถเชิงสมมติในการปรับกระบวนการผลิตและส่งน้ำมันไปยังโรงงานอื่นได้ ขณะเดียวกันก็สามารถดำเนินการซ่อมแซมและควบคุมเพลิงในพื้นที่ที่ได้รับผลกระทบ

อย่างไรก็ตาม นี่ไม่ได้หมายความว่าผลกระทบจากการโจมตีจะไม่ปรากฏให้เห็น ในระดับนี้เริ่มเกิดการหยุดชะงักและการขาดแคลนแล้ว โดยคาดว่ากำลังการแปรรูปที่หายไปอยู่ในช่วงประมาณ 0.2–0.5 ล้านบาร์เรลต่อวัน

นอกจากนี้ โรงงานหลายแห่งได้รับความเสียหายในระดับที่ยากต่อการซ่อมแซม การปรับเส้นทางการผลิตใหม่ใช้ทั้งเวลาและต้นทุนสูง และในบางกรณีก็ไม่สามารถทำได้ทางกายภาพ อีกทั้งโรงกลั่นน้ำมันของรัสเซียส่วนใหญ่ถูกออกแบบมาเพื่อรองรับตลาดภายในประเทศเป็นหลัก เมื่อโรงกลั่นถูกทำลายหรือหยุดทำงาน จะส่งผลให้ตลาดเชื้อเพลิงในพื้นที่นั้นหยุดชะงักทันที

มุมมองด้านงบประมาณ

มูลค่าการส่งออกน้ำมันดิบของรัสเซียลดลงต่ำกว่าระดับก่อนสงครามประมาณ 10% ขณะที่การส่งออกผลิตภัณฑ์กลั่น (refined products) ลดลงมากกว่า 40%

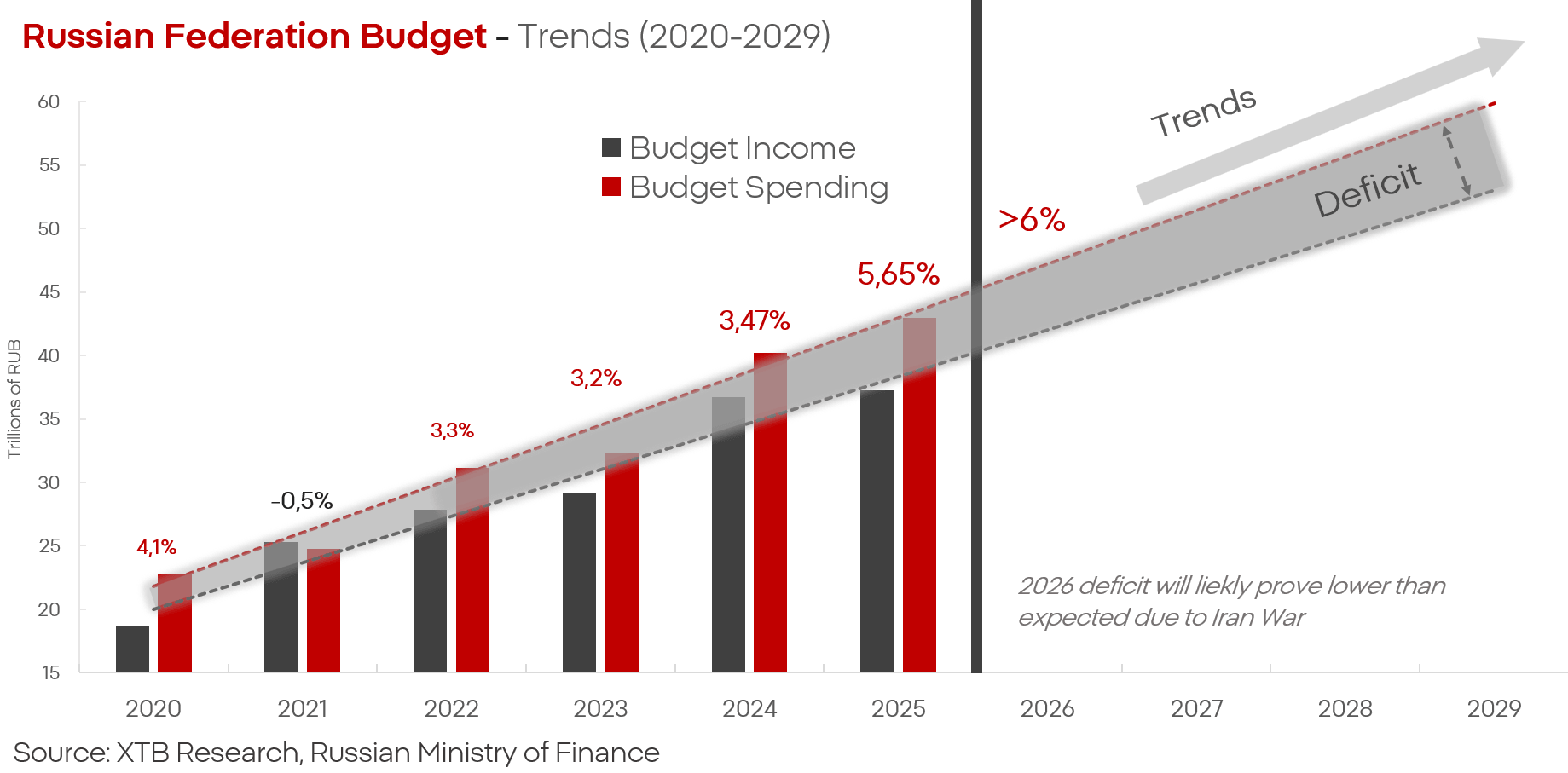

งบประมาณรัฐบาลกลางรัสเซียในปี 2025 อยู่ที่ 41.5 ล้านล้านรูเบิล (ประมาณ 415 พันล้านดอลลาร์สหรัฐ) โดยงบด้านกองทัพอยู่ที่ 13.2 ล้านล้านรูเบิล และงบด้านความมั่นคงภายในอีกประมาณ 4.5 ล้านล้านรูเบิล ซึ่งหมายความว่า “การป้องกันประเทศ” และ “ความมั่นคง” ซึ่งในทางปฏิบัติคือค่าใช้จ่ายด้านสงครามและการควบคุมภายใน รวมกันแล้วมีสัดส่วนมากกว่า 40% ของงบประมาณทั้งหมด

รายได้งบประมาณจากน้ำมันและก๊าซคิดเป็นประมาณ 20–30% ของรายได้งบประมาณทั้งหมดของรัสเซีย ดังนั้นโครงสร้างนี้จึงมีความเปราะบางอย่างมาก หากสมมติว่ามูลค่าการส่งออกที่ลดลงส่งผลโดยตรงต่อรายได้รัฐ ก็อาจหมายถึงการหดตัวของงบประมาณในระดับ “หลักสิบเปอร์เซ็นต์” ของงบประมาณรวมทั้งประเทศ

หากยูเครนยังคงดำเนินหรือยกระดับการโจมตีภาคน้ำมันของรัสเซียต่อไป อาจนำไปสู่สถานการณ์ที่เป็นไปได้มากขึ้นว่า รัสเซียจะต้องเลือกระหว่างการตอบสนองความต้องการภายในประเทศ (รวมถึงกองทัพ) และการตอบสนองลูกค้าส่งออก ซึ่งจะส่งผลโดยตรงต่อรายได้งบประมาณของรัฐ

จากน้ำมัน 1 ตัน รัสเซียสามารถผลิตดีเซลได้ประมาณ 300–400 กิโลกรัม และน้ำมันเบนซินประมาณ 150 กิโลกรัม

ในขณะเดียวกัน เศรษฐกิจรัสเซียต้องใช้น้ำมันเชื้อเพลิงประมาณ 130–140 ล้านตันต่อปีเพื่อให้ระบบดำเนินไปได้ในสภาวะค่อนข้างปกติ

เมื่อพิจารณาศักยภาพของโรงกลั่นในประเทศ หมายความว่ายูเครนอาจต้องทำให้กำลังการกลั่นของรัสเซียเสียหายราว 50–60% เพื่อสร้างสถานการณ์ที่บังคับให้รัสเซียต้องเผชิญ “ทางเลือก” ดังนี้:

- หยุดหรือชะลอปฏิบัติการทางทหารเนื่องจากขาดแคลนเชื้อเพลิง

- หรือปรับลดรายจ่ายงบประมาณอย่างมีนัยสำคัญจากข้อจำกัดด้านการส่งออกพลังงาน

ความขัดแย้งในอิหร่านเปลี่ยนสถานการณ์หรือไม่?

มีผลบางส่วน แต่ไม่ใช่ทั้งหมด

การปรับตัวขึ้นของราคาน้ำมันในตลาดโลก และการพึ่งพาพลังงานจากเอเชียที่สูง ทำให้เกิดผลสะท้อนต่อรายได้ของรัสเซีย ราคาน้ำมัน Urals ปรับขึ้นจากประมาณ 60 ดอลลาร์ต่อบาร์เรลไปมากกว่า 90 ดอลลาร์ หรือเพิ่มขึ้นกว่า 50%

อย่างไรก็ตาม การเพิ่มขึ้นนี้เป็นผลจาก “ราคา” ไม่ใช่ “ปริมาณการส่งออก”

ข้อจำกัดเชิงโครงสร้างของรัสเซีย

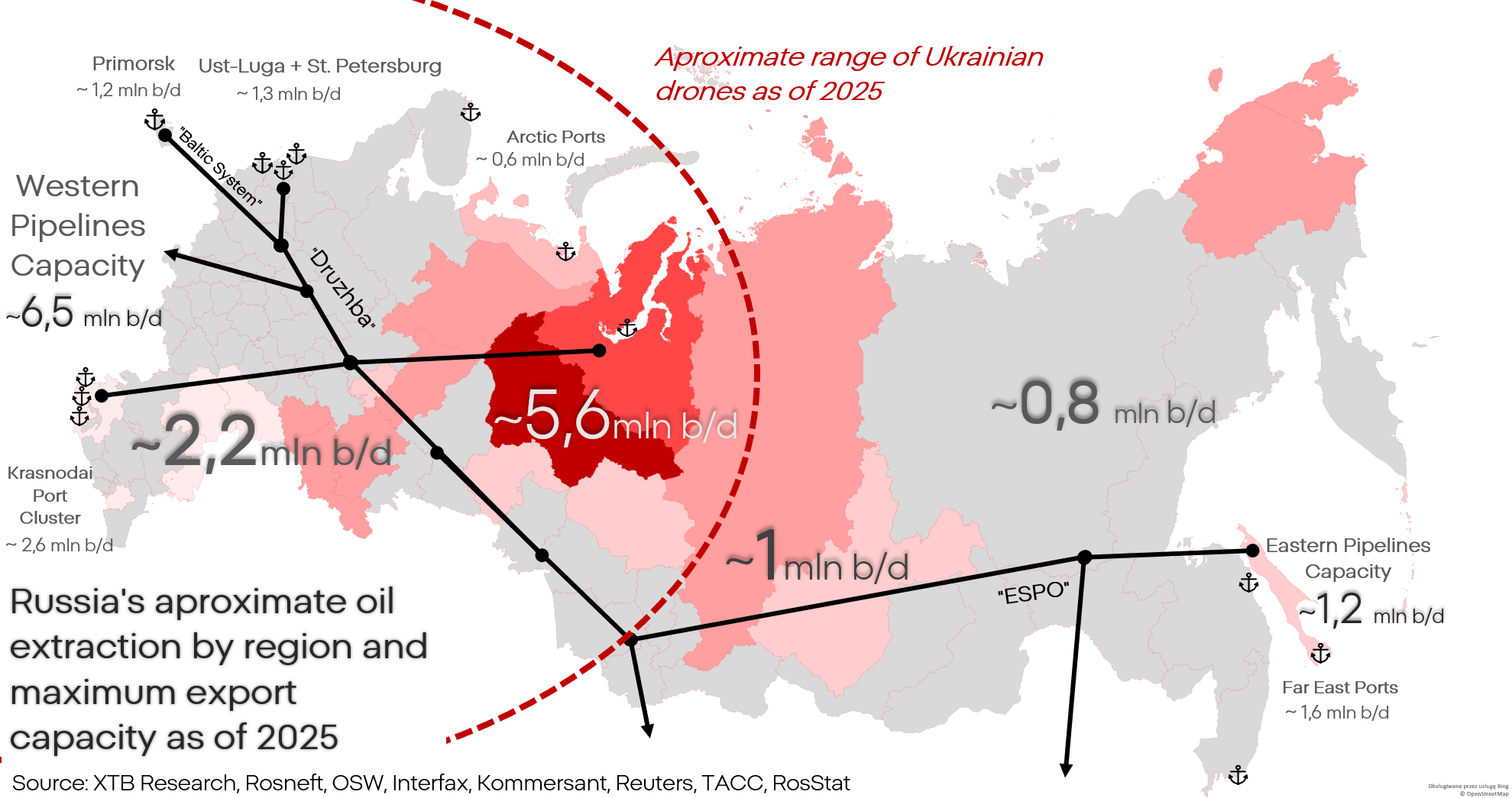

โครงสร้างพื้นฐานด้านการขนส่งพลังงานของรัสเซียมีข้อจำกัดค่อนข้างมาก บริษัท Transneft ซึ่งเป็นผู้ดูแลท่อส่งน้ำมันของรัสเซีย ควบคุมเครือข่ายท่อส่งประมาณ 67,000 กิโลเมตร แต่ส่วนใหญ่ถูกออกแบบเพื่อส่งออกไปยุโรปและกลุ่มประเทศอดีตยุโรปตะวันออก

ขณะที่ความต้องการน้ำมันหลักในปัจจุบันอยู่ที่เอเชีย แต่ท่อส่งและท่าเรือในภูมิภาคนี้กำลังใช้งานใกล้เต็มกำลังแล้ว

ในบริบทของความขัดแย้งในตะวันออกกลางและราคาสินค้าโภคภัณฑ์ที่สูงขึ้นทั่วโลก เป้าหมายของยูเครนคือการจำกัดความสามารถในการส่งออกและขนส่งน้ำมันของรัสเซียเพิ่มเติม การโจมตีท่าเรือและโรงกลั่นขนาดใหญ่ใน Ust-Luga และ Tuapse ถูกมองว่าเป็นส่วนหนึ่งของยุทธศาสตร์นี้ เนื่องจากเป็นจุดสำคัญทั้งในด้านการผลิตและการส่งออก

ผลกระทบต่องบประมาณรัสเซีย

ราคาน้ำมันที่สูงขึ้นช่วยบรรเทางบประมาณของรัสเซียได้เพียงบางส่วน แม้รายได้จากการส่งออกในเดือนมีนาคมจะเพิ่มขึ้นประมาณ 40% แต่ยังคงลดลงเกือบครึ่งเมื่อเทียบกับช่วงเดียวกันของปีก่อน

ในเดือนเมษายน รายได้เพิ่มขึ้นเป็นประมาณ 19 พันล้านดอลลาร์ หรือเพิ่มขึ้นราว 100% แต่เมื่อพิจารณาในเชิงประวัติศาสตร์ นี่น่าจะเป็นเพียงการฟื้นตัวชั่วคราว

ที่สำคัญ รายได้ของรัสเซียยังถูกจำกัดโดย “เพดานทางกายภาพ” หรือความสามารถด้านโลจิสติกส์และโครงสร้างพื้นฐานการส่งออก มากกว่าจะขึ้นอยู่กับราคาน้ำมันเพียงอย่างเดียว

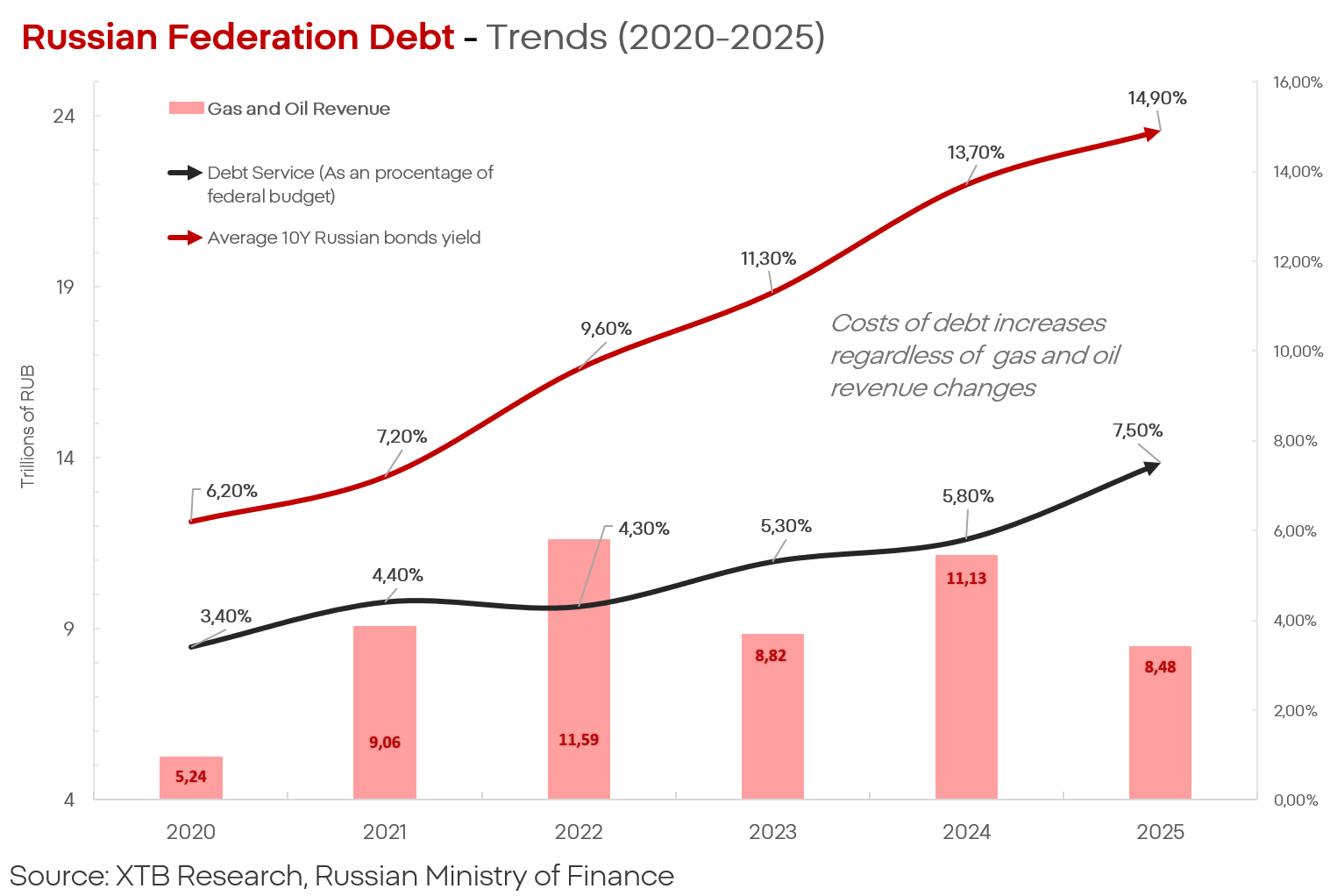

รายได้เหล่านี้ โดยธรรมชาติแล้วไม่ใช่รายได้ถาวร ผลกระทบต่อทั้งงบประมาณของรัสเซียและหนี้สาธารณะที่กำลังกลายเป็นภาระที่เพิ่มขึ้นเรื่อย ๆ ก็ไม่ใช่สิ่งที่ยั่งยืนเช่นกัน แม้รัสเซียจะมีผลกำไรเกินดุลจำนวนมากในปี 2022 และสามารถดำเนินกลไกหลบเลี่ยงมาตรการคว่ำบาตรได้จริงในปี 2024 แต่ต้นทุนการชำระหนี้กำลังเพิ่มขึ้นในอัตราที่รวดเร็วไม่ต่างจากความสูญเสียในแนวรบยูเครน

ในขณะเดียวกัน แหล่งข่าวจาก Reuters ระบุว่ารัสเซียเริ่มมีการจำกัดทั้งการผลิตและการส่งออกน้ำมันอย่างชัดเจน โดยในเดือนเมษายน การผลิตน้ำมันคาดว่าจะลดลงมาอยู่ที่ 8.5 ล้านบาร์เรลต่อวัน และการส่งออกอยู่ที่ 4.1 ล้านบาร์เรลต่อวัน หากตัวเลขนี้ถูกต้อง หมายความว่าการผลิตน้ำมันของรัสเซียได้ลดลงสู่ระดับต่ำสุดในรอบประมาณ 10 ปี แม้ในช่วงที่ราคาน้ำมันอยู่ในระดับสูงเป็นประวัติการณ์และความต้องการยังแข็งแกร่ง

แม้แต่กระทรวงเศรษฐกิจของรัสเซียเองก็ยังประเมินแนวโน้มในเชิงลบ โดยคาดว่าการส่งออกน้ำมันจะลดลงมาอยู่ที่ราว 200 ล้านตันต่อปี และยอมรับว่าไม่มีแนวโน้มที่รัสเซียจะสามารถฟื้นฟูตำแหน่งทางการตลาดได้ภายในทศวรรษนี้

ทั้งหมดนี้หมายความว่า สงครามในอิหร่านอาจเป็นแรงหนุนสำคัญต่อรัสเซียในระยะสั้น แต่หากแนวโน้มปัจจุบันยังดำเนินต่อไป ก็อาจยังไม่เพียงพอที่จะหยุดทิศทางเชิงลบที่กำลังก่อตัวขึ้นอย่างต่อเนื่องต่อเศรษฐกิจ อุตสาหกรรม และงบประมาณของประเทศ

Kamil Szczepański

นักวิเคราะห์ตลาดการเงิน XTB

BREAKING: เศรษฐกิจยูโรโซนฟื้นตัว? PMI สดใส แต่ราคาน้ำมันและก๊าซสูงยังเป็นแรงกดดัน

Oil rises over 3% 🛢️

สรุปก่อนประกาศผลประกอบการ: ภาคอุตสาหกรรมกลาโหม

🛢️ น้ำมันดิบ Brent ทดสอบระดับ $95 ต่อบาร์เรล