-

At 1:30 pm BST, we will learn the key NFP report, depicting the state of the US labor market in May.

-

Analysts estimate that non-farm employment increased by 180,000 in May compared to 175,000 in April.

-

Additional indicators in this report, namely unemployment, labor force participation, and wage growth, are expected to show no deviations from April's readings.

-

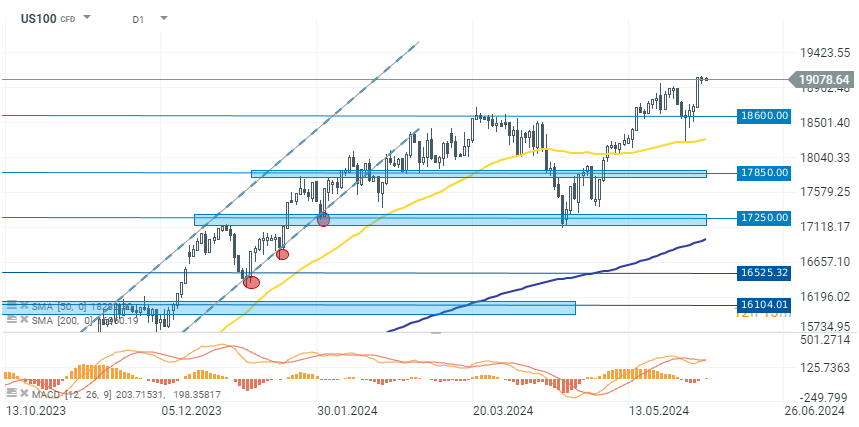

US100 is oscillating around its historical highs ahead of the NFP report.

-

The report's outcome may determine whether this barrier will be broken or if we will see a retreat in demand for risk-related instruments.

-

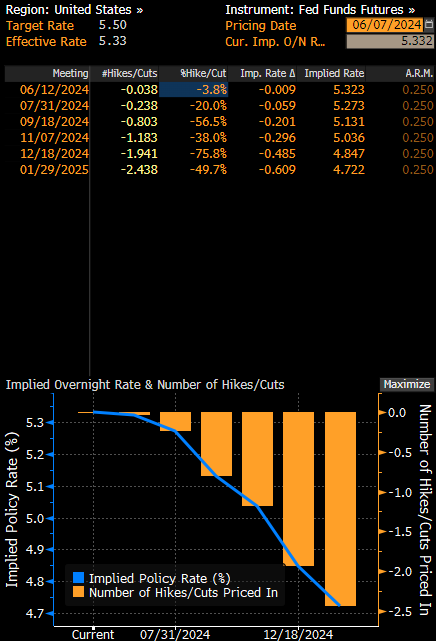

Currently, swaps estimate an 80% probability (cumulative value) that the Fed will make one rate cut of 25 basis points by September this year.

Ahead of us is the key reading of the week, the NFP data from the US labor market. It is widely believed that despite several indicators expected to accelerate slightly compared to April's reading, the overall tone of the report will indicate that economic momentum in the labor market is weakening. Worse data could theoretically allow for an extension of the rally in global risk-related markets, including stock indices, cryptocurrencies, or currencies excluding the dollar. Currently, swaps estimate an 80% probability (cumulative value) that the Fed will make one rate cut of 25 basis points by September this year. A worse reading could further increase this probability, opening the window for a bullish reaction on Wall Street. So, what to expect from today's data?

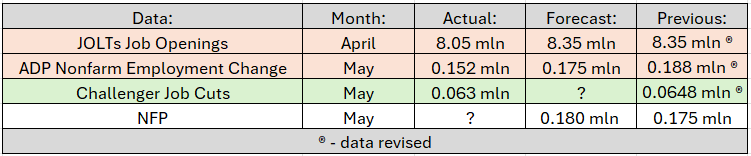

Early reports indicate a weaker NFP reading.

Forecasters expect the May US employment report to provide new evidence that the labor market is gradually cooling. This could also be suggested by data released earlier this week, especially the April JOLTS readings and the May ADP report. However, historically, these data have often not aligned linearly with NFP data, frequently indicating a completely opposite picture of the situation.

Early indications from JOLTS and ADP favor a lower NFP reading. Source: XTB

When analyzing macro outlook, it is also worth mentioning the ISM PMI data. In both cases (manufacturing and services), the May readings indicated a higher employment subindex, with mixed main ISM data and lower values in the price subindex, which in this context can be considered an inflation indicator. However, considering that both subindexes oscillated within the range of analysts' expectations (within +/- 1 standard deviation), their predictive ability for NFP data may be limited.

Implied FED interest rate path

Contracts futures based on FED funds indicate that there is an 80% probability (cumulative value) that the FED will make one rate cut of 25 basis points by September this year. The NFP reading is likely to change this value significantly, and it is the upward or downward revision that will be crucial for the market's reaction to the presented data.

Source: Bloomberg Financial LP

US100 (D1 Interval)

Before the release of the NFP data, the US100 is consolidating around historical highs above 19,000 points. Volatility in the index has been limited for two days, and investors' attention is focused on the release of labor market data at 14:30. The consensus indicates that the data will show further market stabilization around last month's readings. Data deviating from expectations may affect the Fed's rate cut path, and consequently cause greater market volatility. A reading slightly below expectations would give markets hope that the US economy is not in the worst condition, but on the other hand, it would increase the likelihood of faster rate cuts. In such a scenario, we can expect a breakout in the US100 index above the current consolidation channel. Also, a reading in line with expectations could trigger a similar reaction, looking at the recent publications of macroeconomic data.

On the other hand, a reading above expectations, contrary to the previous scenario, could reduce the chances of the first rate cut in September. Consequently, we can expect a downward reaction in the US100 index.

Source: xStation 5

Source: xStation 5

BREAKING: เศรษฐกิจยูโรโซนฟื้นตัว? PMI สดใส แต่ราคาน้ำมันและก๊าซสูงยังเป็นแรงกดดัน

🔼 DE40 รับแรงหนุนจากผลประกอบการของ SAP

Economic Calendar: ภาคอุตสาหกรรมเผชิญแรงกดดันจากราคาน้ำมัน

Morning Wrap: ตลาดจะฟื้นตัวหลังแรงเทขายเมื่อวันพฤหัสบดีหรือไม่❓