The Bank of Japan has decided to raise interest rates. The benchmark rate was raised by 15 basis points from 0.1% to 0.25%, a surprising decision for the markets. Futures had priced in the fact that bankers would not yet decide on such a large hike at this meeting. Bank of Japan raised rates to highest since 2008; Japanese yen strengthened after decision

- In the first reaction, the yen strengthened and the USDJPY settled around 151, but a moment later the currency pair rebounded to above 154, and is currently trading around 152, below levels before the decision.

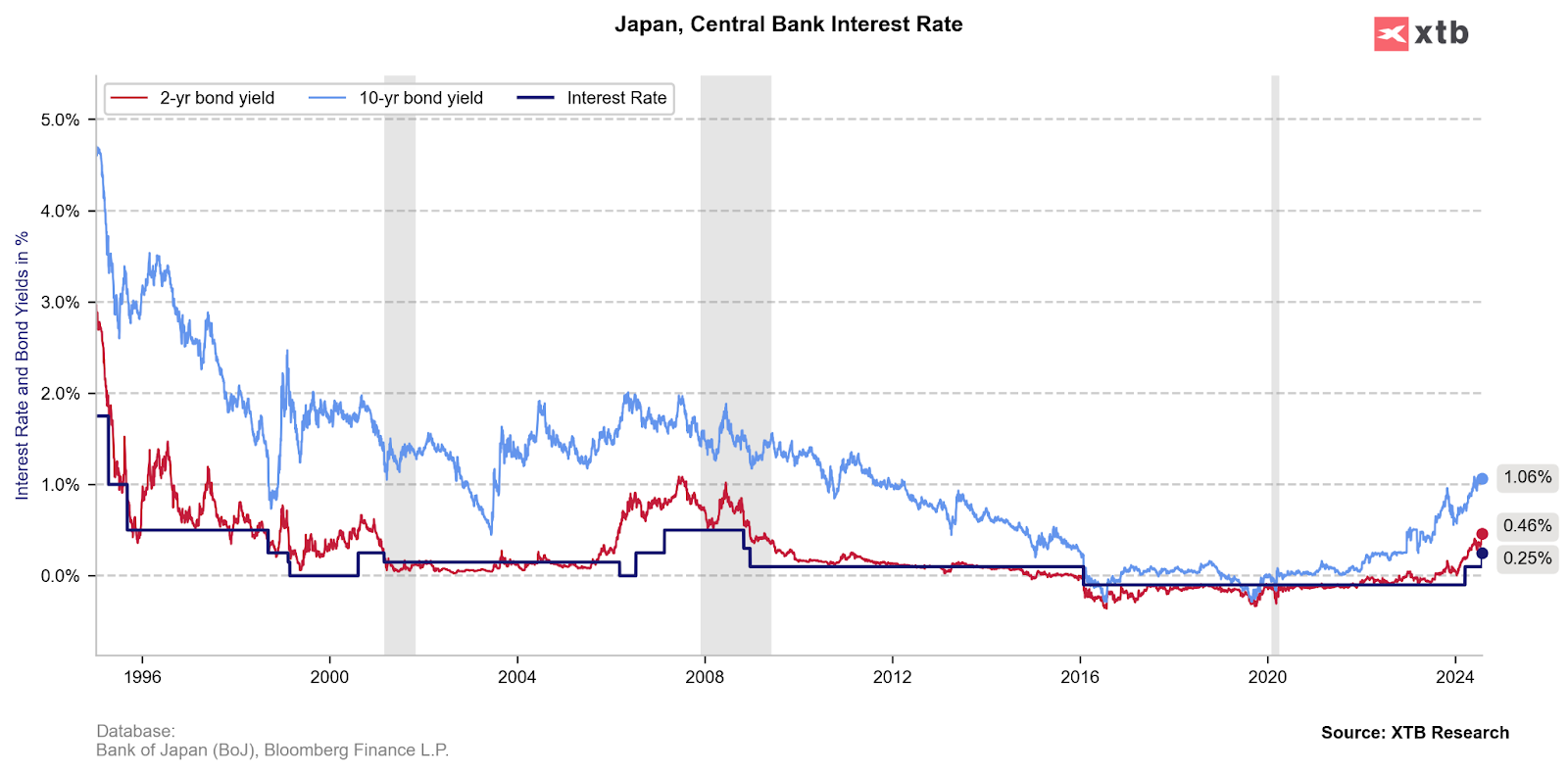

- Such a reaction leads us to conclude that the decision was hawkish and may lead to a decline in speculative positions targeting the Japanese yen. Yields on 10-year Japanese bonds rose to 1.06% (up 5 basis points and 5.88% from pre-decision levels).

Source: XTB Research, Bloomerg Finance L.P.

- In addition to the rate hike, the BoJ announced a reduction in bond purchases. The quantitative tightening implies a reduction in the bond-buying process to 3 trillion yen per month (equivalent to about $19.6 billion) from 6 trillion previously.

- However, markets expected a more hawkish move Japan is again heading in the opposite direction of the global economy.

- In most major economies, bankers have either already decided on the first reductions (as in Switzerland or Canada) or are strongly considering such a decision (like the US Fed, among others).

Ueda comments

The Bank of Japan's decision may help curb the yen's strong weakening trend in the global currency market, and is underpinned by rising inflation expectations in the economy. Kazuo Ueda, BoJ Governor, indicated that a weak yen raises risks for the Japanese economy, suggesting that the yen's strengthening is an important factor the bank is considering in its decisions. In his view, the current interest rate on the Japanese economy remains very low and is in fact 'deeply negative'.

- At the same time, the date of the next rate hike is currently uncertain and will depend on data.

- BoJ's JGB reserves to fall by about 7 to 8% in two years

- Currently, the domestic economy is recovering; it is returning to growth at a very moderate pace; service prices are rising noticeably

- Consumption is growing at a steady pace; household sentiment supports this scenario

- BoJ data on wage hikes suggest they are also increasing at smaller firms (hawkish; there was a perception that they might mostly affect Japan's largest firms, benefiting from exports)

- BoJ expects wage pressures to continue, and that the increases are not just a temporary trend in the economy

- According to Ueda, today's rate hike will not slow economic growth

- Ueda announced that if the economy and prices move in line with the central bank's projections, the bankers will decide on further increases.

- In his view, the 0.5% interest rate level is not a cut-off point to block further increases if data support the decision.

Ueda wants to avoid sudden increases in the short term. Rather, it is inclined to anticipate a potential deterioration in economic conditions so that interest rate decisions are gradually adjusted to the changing economic situation. In the bank's view, a weakening yen underpins rising prices and supports inflation by pushing it beyond the 2% inflation target.

USJPY (D1 interval)

The currency pair has slipped to levels not seen since early May, where we see key price reactions including two local peaks from the fall of 2022 and 2023, and the bottom of the early May 2024 sell-off. A break below could result in a test of the 145 - 148 area, where we see the 38.2 Fibonacci retracement of the 2023 upward wave and the important price reactions of June and December 2023 and this spring.

Source: xStation

Chart of the Day: เงินเฟ้อกดดัน AUDUSD! 'เหยี่ยว' RBA กำลังเปลี่ยนท่าที?

Morning Wrap: ตลาดเอเชียเผชิญแรงขายจากผลประกอบการ SK Hynix และความตึงเครียดอิหร่าน ดอลลาร์หยุดชะลอความเคลื่อนไหวก่อนผลประชุม Fed

ข่าวเด่นวันนี้ 29 ก.ค.

Chart of the Day: ราคาน้ำมันร่วง...ใครได้รับผลกระทบมากที่สุด?