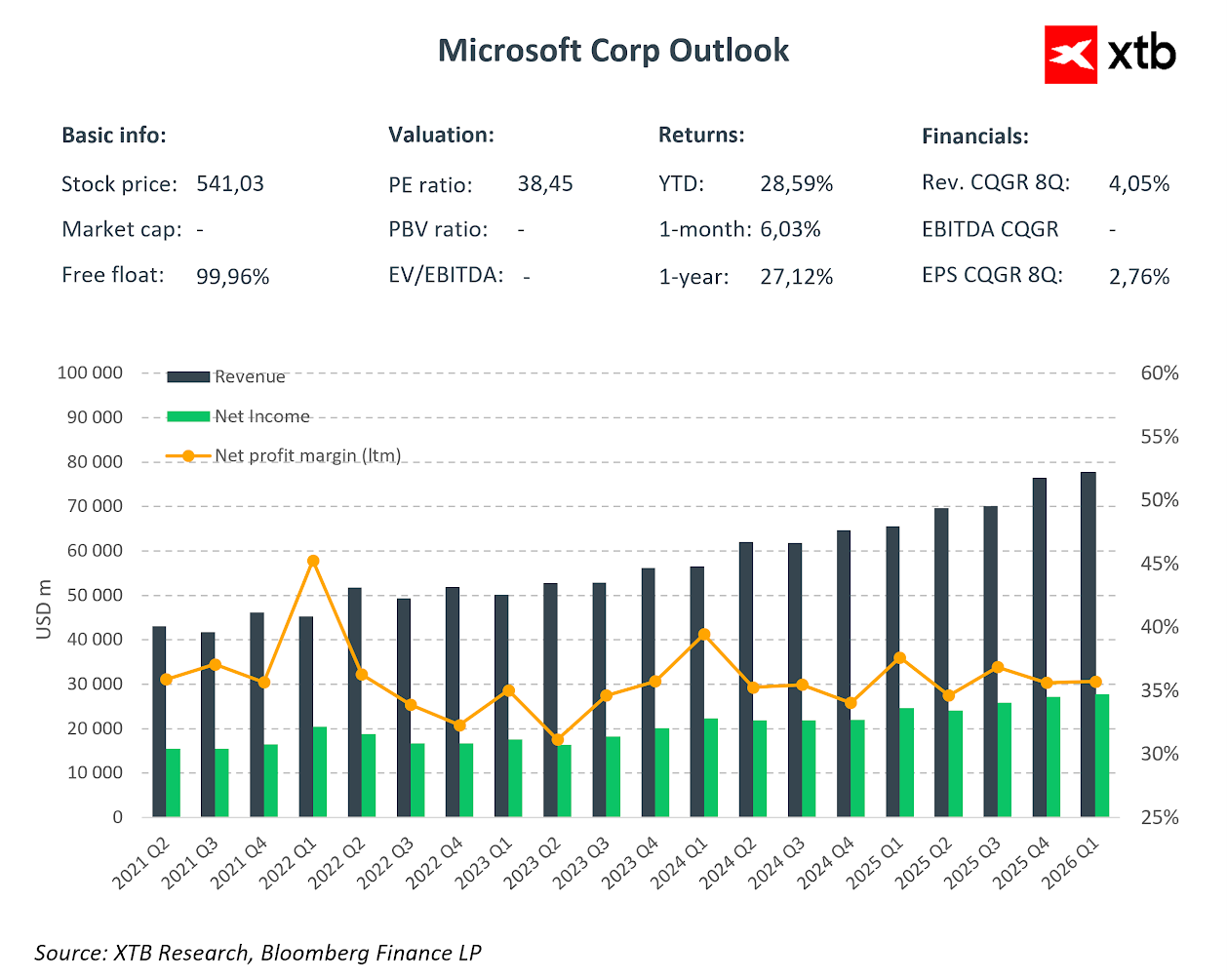

Microsoft รายงานผลประกอบการที่แข็งแกร่งสำหรับไตรมาสแรกของปีงบประมาณ 2026 (สิ้นสุด 30 กันยายน 2025) โดยทำผลงานเหนือความคาดหมายของนักวิเคราะห์ในทุกตัวชี้วัดหลัก โดยเฉพาะการเติบโตที่แข็งแกร่งของธุรกิจคลาวด์

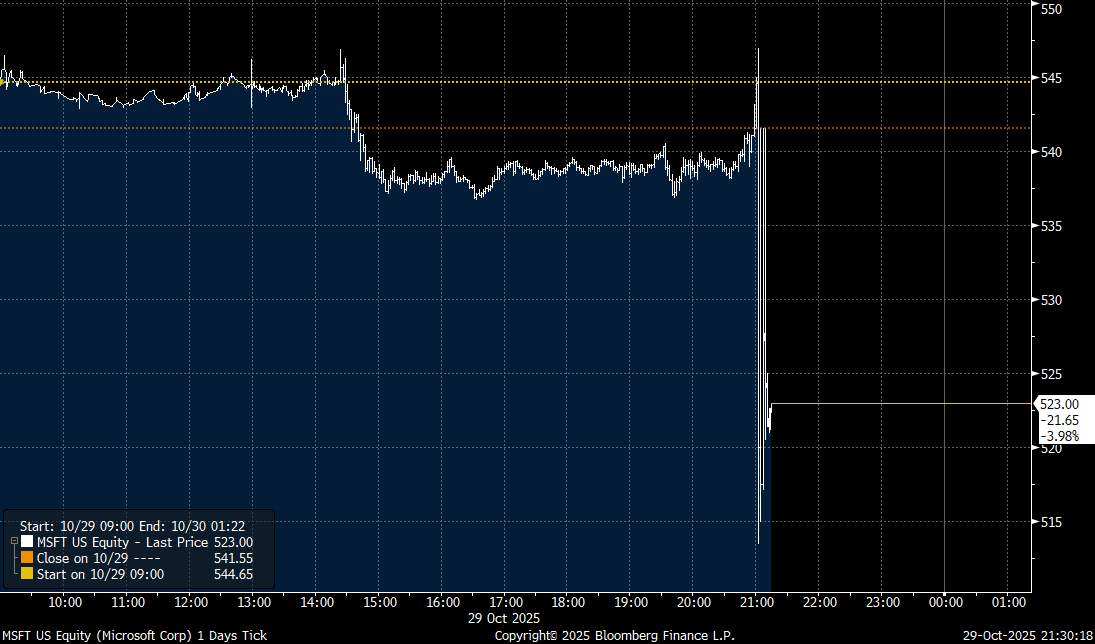

แม้ว่าผลการดำเนินงานจะดี แต่หุ้นของบริษัทปรับตัวลดลงสูงสุด 3% ในช่วงหลังตลาด เนื่องจากนักลงทุนยังคงกังวลเกี่ยวกับผลตอบแทนจากการลงทุน (ROI) ของโครงสร้างพื้นฐาน AI ขนาดใหญ่

หุ้น Microsoft ปรับตัวลดลงในช่วงหลังตลาด แหล่งข่าว: Bloomberg

ไฮไลท์ผลประกอบการรายไตรมาส

รายได้และความสามารถในการทำกำไร:

-

รายได้: 77.7 พันล้านดอลลาร์ (+18% เทียบกับปีก่อน, +17% ในสกุลเงินคงที่) เทียบกับประมาณการ 75.55 พันล้านดอลลาร์

-

กำไรจากการดำเนินงาน: 38.0 พันล้านดอลลาร์ (+24% YoY) เทียบกับประมาณการ 35.1 พันล้านดอลลาร์

-

EPS (GAAP): 3.72 ดอลลาร์ (+13% YoY)

-

EPS (non-GAAP): 4.13 ดอลลาร์ (+23% YoY) โดยไม่รวมผลกระทบจากการลงทุนใน OpenAI

-

กำไรสุทธิ (GAAP): 27.7 พันล้านดอลลาร์ (+12% YoY)

ถึงแม้ตัวเลขพื้นฐานแข็งแกร่ง นักลงทุนยังคงกังวลเรื่อง ROI ของการลงทุน AI ขนาดใหญ่ ซึ่งเป็นสาเหตุหลักที่หุ้นปรับลดหลังตลาด

Capital Expenditure (CapEx):

-

CapEx: $19.39 Billion — significantly below the $23.04 Billion consensus. This divergence may be seen as a disappointment by those seeking aggressive spending, but could also suggest that further expenditure may not substantially accelerate the revenue outlook.

Business Segment Results

Intelligent Cloud (Core Growth Driver):

-

Revenue: $30.9 Billion (+28% YoY) vs. $30.18 Billion consensus.

-

Azure and other cloud services: +39% YoY (ex-FX) vs. +37.1% consensus.

Productivity and Business Processes:

-

Revenue: $33.02 Billion (+17% YoY) vs. $32.29 Billion consensus.

-

Microsoft 365 Commercial cloud: +17% YoY (+15% in constant currency).

-

Microsoft 365 Consumer cloud: +26% YoY.

-

LinkedIn: +10% YoY.

-

Dynamics 365: +18% YoY.

More Personal Computing:

-

Revenue: $13.76 Billion (+4% YoY) vs. $12.88 Billion consensus.

-

Windows OEM: +6% YoY.

-

Search and Advertising (ex-TAC): +16% YoY.

Why Are Shares Declining?

Despite beating expectations on revenue and earnings, the market reacted negatively due to several factors:

-

ROI Concerns over AI Investment: Microsoft is spending tens of billions of dollars on AI infrastructure (approx. $80 Billion in FY2025), yet investors are demanding more convincing evidence of proportional returns from this outlay.

-

Guidance and Future CapEx: The market was looking for clear signals of accelerating AI monetization. The lower-than-expected CapEx ($19.39 Billion vs. $23 Billion consensus) may suggest Microsoft is adjusting the pace of investment, raising questions about demand momentum.

-

AI Infrastructure Competition: Reports of Oracle reportedly taking on some infrastructure orders from OpenAI (a key Microsoft partner) may signal a loss of momentum in the hyperscale segment.

-

Margin Pressure: CFO Amy Hood had previously warned that margins could be pressured amid the expansion of data centers. While the operating margin was 45% this quarter, continued heavy investment could erode it further.

-

Valuation Premium: Microsoft shares trade at a forward P/E of around 35, commanding a premium over the broader market. Investors expect this high valuation to be justified by spectacular AI revenue growth, which has yet to fully materialize.

Positive Indicators

-

Microsoft Cloud Revenue: $49.1 Billion (+26% YoY).

-

Remaining Performance Obligations: Increased by 51% to $392 Billion — a strong signal of future demand.

-

Free Cash Flow: The company generated $45.1 Billion from operating activities during the quarter.

-

Capital Return to Shareholders: $10.7 Billion returned via dividends and share repurchases.

Summary

Microsoft delivered solid results, surpassing consensus on revenue, operating profit, and EPS. Azure's 39% growth (above the 37% forecast) confirms the strength of the cloud platform. However, the market appears to be penalising the company for the lack of clear indication on how its past investments will translate into greater future profits. Furthermore, emerging competition in the cloud infrastructure segment raises question marks for one of the market leaders. Nevertheless, it must be acknowledged that the company's prospects for continued growth and development remain extremely strong.

The company's shares lost 3-4% in after-hours trading. Source: xStation5

ข่าวเด่นวันนี้ 30 ก.ค.

SK Hynix Earnings: ตลาดเทขายมากเกินไปหรือไม่?

ASML ร่วงแรง: ความฝันและข่าวลือยังไม่สามารถทำลายการผูกขาดได้

US100 ร่วงเกือบ 2% 🚨