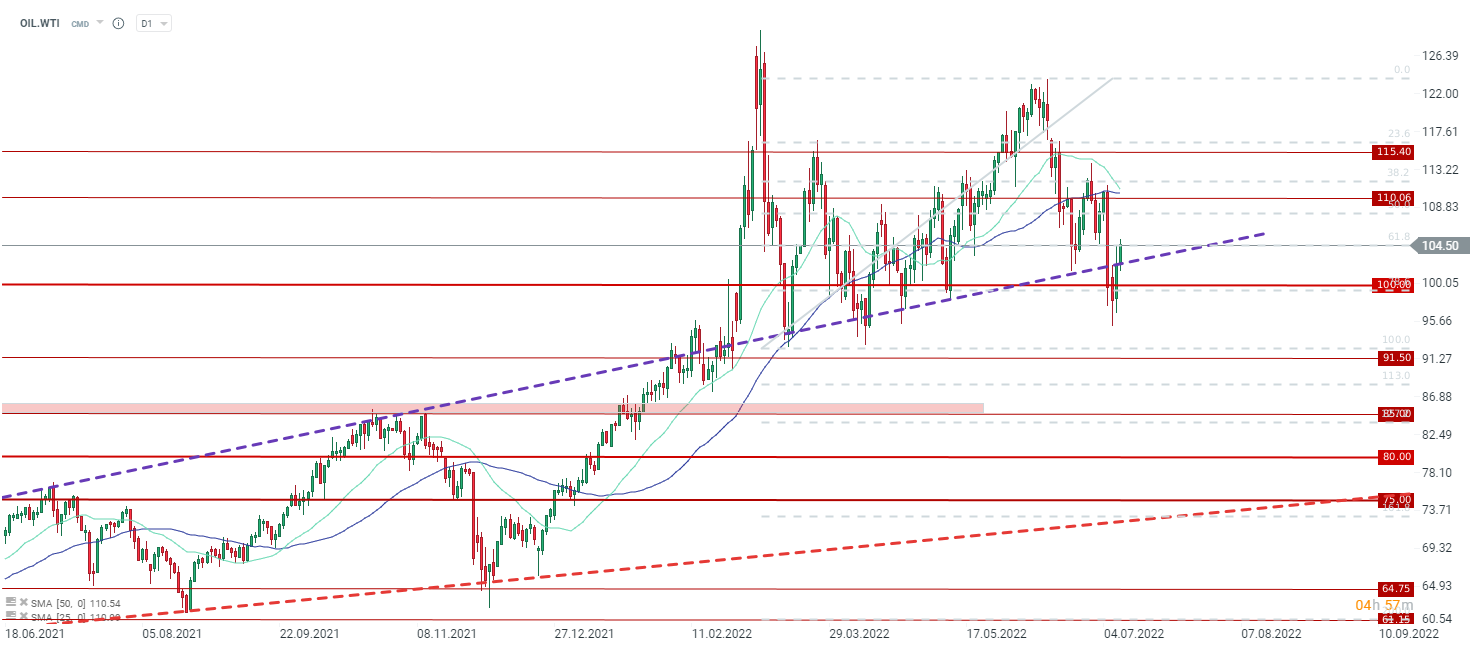

The massive declines in the oil market earlier in the week were the result of major recession fears around the world. Recessionary fears have emerged primarily in Europe in the face of a strike in Norway, which is leading to a cut of up to 50% of gas exports to European countries. Lack of access to gas from a major supply, a 60% drop in exports from Gazprom and the shutdown of exports next week due to maintenance repairs are pushing the price of the vital energy commodity very high again, but also increasing the chances of a recession if large supplies are not resumed. From all this, we had a massive sell-off in the euro and the pound and the strengthening of the US dollar, which led to an even bigger sell-off in the commodity market.

On the other hand, there are no serious signs of demand destruction yet. Yes, in the United States, the holiday plans of millions of Americans have been altered due to high fuel prices, and demand for marine fuel in the first half of the year was lower than a year earlier. However, in addition to this, overall global demand is growing all the time along with a very large supply constraint, primarily in terms of the fuel market. The physical market continues to see very strong demand, which is characterized by a large difference between the spot price and the next contract. The crack spread, or the difference between the price of the petroleum product and the price of crude, is still very large (despite a slight pullback), showing that the biggest problem is seen on the end product side. U.S. refineries are currently producing as much as they can, but after the summer, maintenance time will come, which could put upward pressure anew.

Citi points out that in the event of a recession, oil prices will fall into the area of $65 per barrel. This level seems remote, but we should not rule out such a situation either. As the covid situation showed, demand can very quickly collapse as much as 30% in the space of a few weeks, which led to more than 2 years of recovery from the pre-pandemic situation. On the other hand, the current fundamental situation does not justify levels below $100 per barrel, but rather the continuation of high levels.

At the end of the week, oil recouped more than half of the declines of the entire week, thanks to the last two sessions. On the other hand, the downward sequence in oil is maintained all the time.

Source: xStation5

Chart of the Day: ราคาน้ำมันร่วง...ใครได้รับผลกระทบมากที่สุด?

ปฏิทินเศรษฐกิจ: ผลประกอบการของ PayPal, Visa และ Coca-Cola จับตาเหนือข้อมูลเศรษฐกิจ

สรุปตลาดเช้าวันนี้: ตลาดสหรัฐฯ ทรงตัว หลังยุติการโจมตี แต่หุ้นเซมิคอนดักเตอร์กดดันตลาด (28.07.2026)

สรุปตลาดประจำวัน: สงครามชิปกดดัน Wall Street ขณะที่น้ำมันร่วงแรง หลังสหรัฐฯ–อิหร่านบรรลุข้อตกลงหยุดยิง ⭐