French fashion holding SMCP (SMCP.FR) has updated its forecast for the third quarter as well as the whole of 2023. It was after this that the dynamic sell-off of its shares began. Declines have already reached nearly 28% and the broader fashion company sector is trading under the dash today, with LVMH (MC.FR), Hermes (RMS.FR) and Kering (KER.FR) losing slightly. SMCP lowered forecasts, pointing to a general deterioration in demand conditions in all markets where the company has a presence with a particular focus on China where demand is disappointing.

What did the company report?

- The company's portfolio includes four Parisian luxury brands Claudie Pierlot, Sandro, Maje and Fursac. Previously, the company raised forecasts citing hopes of a rebound in China but the country's economic expansion in 2023 is running clearly below expectations;

- In Q2 2023, China's product sales grew 53%, but the market is unlikely to be able to count on maintaining this momentum in Q3. According to the company's commentary, a definite slowdown has also been observed since the beginning of August in major European markets including France, Italy and Switzerland

- As a result, the company expects modest sales growth in the second half of this year and is no longer counting on a positive effect related to China, which supports the base effect of last year's 'pandemic' year

- Q3 according to the company is expected to be flat or mildly negative on a m/m basis but SMCP maintains a higher forecast for the festive Q4. In Q2, sales in China propelled the company's product sales by more than 8.7% to €305 million, today its total capitalization is below €300 million

- For the full year 2023, the company expects single-digit, modest sales growth and expects EBIT margins to increase between 7 and 9%, compared to 9.2% previously. The company intends to cut costs and slow down the hiring process.

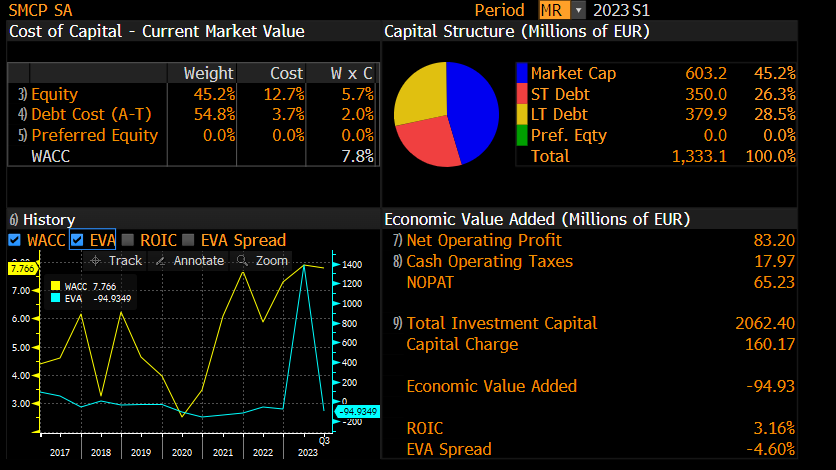

The company has a WACC (weighted average cost of invested capital) higher than ROIC (return on invested capital) resulting in a negative EVA spread - ti somewhat justifies the lower valuation on the P/E side. The above figures are for the end of Q2 2023 - since then the company's capitalization has already fallen by 50%. Source: Bloomberg Finance LP

The company's valuation appears to be relatively low, which may represent an opportunity for 'value investors'. However, it is worth mentioning that a low valuation does not guarantee a possible increase in share prices. Sentiment around luxury companies has clearly begun to deteriorate - the specter of recession in Europe or China is not a positive indicator for stock market bulls, and in an extreme scenario it may turn out that valuations of fashion companies may be adjusted to the prevailing weaker macroeconomic situation.

SMCP shares are currently trading near 2019 - 2020 lows. Source: xStation5

วอลล์สตรีทจะไปต่อได้แค่ไหน? 🗽 สรุปภาพรวมฤดูกาลประกาศผลประกอบการสหรัฐฯ

ผลประกอบการ Berkshire สะท้อนอะไรเกี่ยวกับทิศทางของตลาด?

Intel ต้องการเงิน 1.5 หมื่นล้านดอลลาร์ ปัญหาทางการเงิน หรือราคาที่ต้องจ่ายเพื่อการขยายธุรกิจครั้งใหญ่?

Economic Calendar: ตลาดกลับมาคึกคัก หลังสุดสัปดาห์ที่ความขัดแย้งทางภูมิรัฐศาสตร์ยังไร้ทางออก 🚢